Deutsche Bank Is Allowed Back Into the High-Risk Club

(Bloomberg Opinion) -- Deutsche Bank AG is back — at least if its ability to sell the riskiest type of debt is a yardstick.

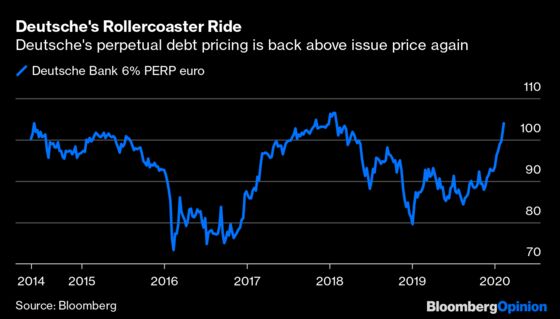

After a six-year hiatus marked by a flirtation with collapse, billions of euros of losses, multiple management changes and its biggest restructuring in decades, Deutsche is going into the deep end of fixed-income risk: a benchmark perpetual bond (known as an AT1, or CoCo bond). Investors’ insatiable hunt for yield and the lender’s own green shoots of recovery have allowed the former basket case of European banking to tap a market that was all but off-limits for years. The German behemoth appears to be exiting intensive care, though a full recovery is not a given.

So-called additional tier 1 regulatory capital bonds (CoCos) are an especially risky type of debt because the investor bears the losses if the bank fails. As such, it’s notable that Deutsche is self-assured enough to sell them — and people are happy to buy. The new issue announced on Tuesday saw initial talk of a 6.75% coupon reduced dramatically to 6% in the final pricing; the order book was 11 times higher than the $1.25 billion issue size.

The big message here for investors is that Deutsche does not need to raise equity to fund itself anymore.

Despite early doubts about the latest restructuring unveiled by Chief Executive Officer Christian Sewing in the summer, Deutsche has improved steadily over the past few months — albeit from a very low base. After hovering near record-low levels for much of 2019, its share price has risen 50% in the past two months. Capital Group, a $2 trillion fund manager, has shown its faith by taking a 3.1% stake.

The bank’s de-risking has helped. After shrinking and shedding assets, Deutsche Bank has improved its capital buffers beyond expectations.

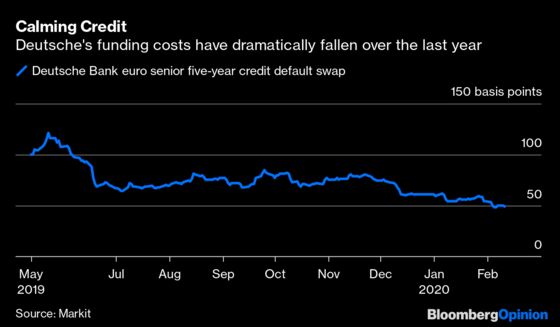

Its credit spreads have narrowed substantially, with five-year senior credit default swap spreads dropping from 80 basis points in November to less than 50 basis points now. That is now in line with blue-chip banking rivals such as Goldman Sachs Group Inc., which should help Deutsche lower its funding costs.

As it happens, Deutsche will probably issue much less net new debt this year as it repays funding taken from the European Central Bank. It helps that it doesn't really need the money being raised from the AT1 issue, as that will bolster its capital cushion further. It is well ahead of its regulatory requirements with a 30 billion-euro ($33 billion) buffer, according to Bloomberg Intelligence's Jeroen Julius.

None of this is to say that Deutsche’s transformation is complete. The 150-year-old lender is cutting one-fifth of its workforce, exiting the trading of stocks and shrinking the balance sheet. After initially pinning the bank's future revenue growth on a tilt toward its corporate banking roots, Sewing has acknowledged that he’s counting on trading revenue to hit targets.

Trading is not a business that can be counted on, as Deutsche reminded investors in its AT1 offer document. Not only are markets tough, the German giant’s franchise isn’t what it was. Still, the bond markets are prepared to take a punt on a form of debt where they carry the cost if things blow up. That’s a vote of confidence of sorts.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

Elisa Martinuzzi is a Bloomberg Opinion columnist covering finance. She is a former managing editor for European finance at Bloomberg News.

©2020 Bloomberg L.P.