(Bloomberg Opinion) -- Christian Sewing has tried to cast an optimistic light on Deutsche Bank AG’s future as he undertakes the lender’s deepest restructuring in decades. The chief executive officer told staff he’d been looking forward to updating the market on his progress five months into the overhaul.

The disclosures from that update, at the bank’s investor day on Tuesday, are more sobering: The skeptics are right to worry about Deutsche’s ability to increase its revenue while shrinking. Profit is also at risk.

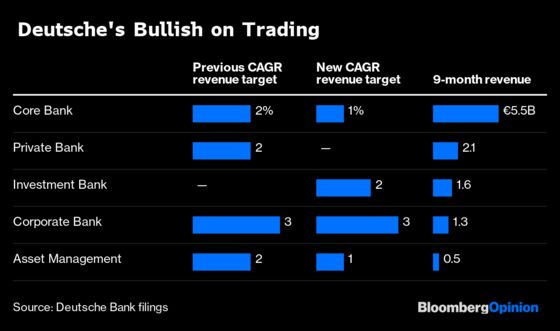

Sewing’s assumptions on interest rates when he unveiled his revamp in July were too bullish. The bank is now counting on a spike in revenue at its scaled-backed securities unit to hit its overall targets, another acknowledgement that things aren’t going to plan. His changes were meant to rein in the company’s dependence on volatile trading businesses.

Back in July, Sewing was heralding a return to the 150-year-old bank’s corporate finance and trade finance roots. Yet after a strong start to fixed-income trading in the fourth quarter, the recently scorned investment bank is making Sewing proudest, he told employees on Tuesday.

Deutsche now expects revenue growth at its core businesses of just 1% a year through 2022, half its previous forecast. Sales at the investment bank should increase 2% annually, compared to a previous estimate of no growth. Sewing has also dialed back his objectives for consumer banking and asset management.

The trading unit’s recovery is remarkable after a torrid third quarter, during which Deutsche lagged behind its Wall Street competitors in bonds and currencies. While Sewing said his reorganization was helping the bank’s trading of emerging markets debt and interest rates, relying on the investment bank again to improve revenue is a gamble. This doesn’t feel like a different direction.

It’s probably too soon to assess the impact of Deutsche’s exit from equity trading, though some clients have been returning. The fourth quarter is expected to be strong too for other Wall Street and European investment banks, according to analysts at KBW, so it’s hard hard to say how much of Deutsche’s improvement is unique.

In fairness, there was some genuinely good news on Tuesday. Cost-cutting targets were reaffirmed, and the bank is getting rid of unwanted assets more quickly than expected.

Regulators have certainly taken note of Deutsche’s efforts to reduce its riskiness. The European Central Bank has lowered the bank’s capital requirement for 2020. That’s a welcome sign that the lender may be able to fund its reorganization without having to tap investors. With the shares trading near record lows, valuing the bank at about 30% of its tangible book, Sewing desperately wants to avoid a rights issue.

For now the CEO is sticking to a 2022 target for an 8% return on tangible equity, although he acknowledged that market headwinds will make that tougher to achieve. His revenue ambitions have become more realistic, but counting on a continued rebound at the investment bank is exactly what he’s meant to be avoiding.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Elisa Martinuzzi is a Bloomberg Opinion columnist covering finance. She is a former managing editor for European finance at Bloomberg News.

©2019 Bloomberg L.P.