(Bloomberg Opinion) -- There are lots of reasons to fret about debt. And more reasons not to.

There is certainly a lot of debt out there. Federal, state and local governments have accumulated a record $27.9 trillion of debt financing. U.S. companies are selling the most debt in a decade.

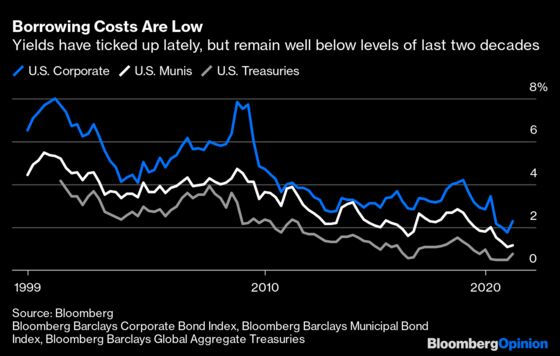

Borrowing costs are the lowest in at least 70 years. The riskiest entities are being rewarded with 52% more credit upgrades than rating downgrades, as demand for exchange-traded funds with high-yield junk bonds climbs to new highs. In today’s credit markets, anyone raising money can do so on the easiest terms of a lifetime.

The bond market is wrapping up a grim first quarter. The Bloomberg Barclays Global Aggregate Index has lost 4.46%, the most since the end of 2016. Yields are rising. Can disaster be far behind?

To judge by dire predictions of the worst inflation in a generation and an obituary earlier this month for a 40-year-old bull market in Treasury securities, the answer must surely be yes. Never mind that the bonanza for borrowers and bond buyers shows few signs of retreating even with interest rates tripling during the past 12 months. Average total debt, weighted by market capitalization among large and small companies that make up the Russell 3000 Index, probably is a record $47 billion, or $4 billion more than a year ago and $16 billion greater than it was at the end of 2015, according to the latest corporate filings compiled by Bloomberg.

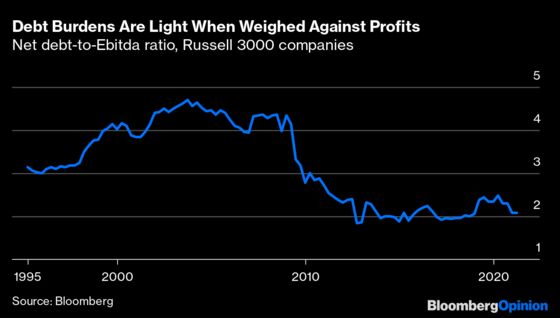

But wait. Corporate America is having little difficulty paying its debts because profits have been booming. The net debt to ebitda ratio, or total debt minus cash and then divided by earnings before interest, taxes, depreciation and amortization, is historically low, reflecting a healthy corporate debt burden relative to profits. The lower the ratio, the easier it is for a firm to increase earnings. The debt ratio for the Russell 3000 has been hovering below 2.5 since 2011, well below the average of more than 1,500 companies in the MSCI developed countries index and the most robust financial health since data was compiled in 1995, when interest rates were 24 times higher than they are today.

To be sure, some companies are canceling or delaying planned borrowings until recent price fluctuations subside. The debt ratios for smaller companies in the Russell 2000 peaked during the Covid-19 pandemic and remain at the highest level since 2015. Yet the deteriorating spread between small and large companies still is no worse than the five-year average, according to data compiled by Bloomberg. When the Federal Reserve lowered some short-term lending rates to little more than zero last year to shore up the economy during the pandemic, borrowing costs declined to a record throughout the credit markets, according to the Bloomberg Barclays Indexes.

The Fed's extraordinary intervention enabled investment-grade and non-investment-grade companies to issue $1.9 trillion and $442 billion of debt, respectively, in 2020. They already raised a fifth and a third of these amounts so far this year, according to data compiled by Bloomberg. Investor appetite for the riskier bonds is attributed partly to improved S&P ratings for 178 high-yield corporate debt securities compared to 117 downgrades. Moody’s also issued about 2.3 upgrades for each downgrade, its highest ratio in the past decade.

All of which helped Fort Worth, Texas-based American Airlines Group Inc. sell a total $6.5 billion of bonds in March at yields a fifth below the rates prevailing six months earlier, according to data compiled by Bloomberg. Carnival Corp., the Miami-based owner and operator of cruise ships to global vacation destinations, sold $3.5 billion of bonds in February at an initial yield of 5.9% that subsequently declined to 5.2% as investors snapped up the offering. Similar securities sold by the company last year yielded 6.8%.

In the market for debt issued by state and local governments and other tax-exempt borrowers, Princeton University sold about $432 million of bonds through the New Jersey Educational Facilities Authority in March at lower yields than the top-rated benchmark. The successful sale continued a trend of record issuance by municipalities which raised more than $100 billion during the first quarter after selling $454 billion in 2020, according to data compiled by Bloomberg.

For all the pessimism among commentators, exchange-traded funds holding municipal debt are seeing record inflows from investors, totaling $14.3 billion in 2020, or 3.6 times the amount five years ago. Demand is similar for high-yield ETFs which continue to see inflows close to 2019’s record $19.6 billion, or 6.8 times the amount at the end of 2015. The outcome is no different for investment-grade ETFs, which experienced a record $161 billion of inflows in 2020, or 3.3 times the flows from five years ago, according to Bloomberg Intelligence.

Not bad for a bear market.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Matthew A. Winkler is Co-founder of Bloomberg News (1990) and Editor-in-Chief Emeritus; Bloomberg Opinion Columnist since 2015; Co-founder of Bloomberg Business Journalism Diversity Program in 2017. During his 25 years as Editor-in-Chief, Bloomberg News was a three-time finalist and winner of the Pulitzer Prize for Explanatory Reporting and received numerous George Polk, Gerald Loeb, Overseas Press Club and Society of Professional Journalists and Editors (Sabew) awards.

©2021 Bloomberg L.P.