(Bloomberg Opinion) -- The pandemic is far from over, but Singapore’s biggest bank is already off to the races.

DBS Group Holdings Ltd.’s recent S$1.1 billion ($828 million) purchase of a 13% stake in a rural Chinese bank gives a flavor of the aggressive deal-making investors can expect, as Citigroup Inc.’s exit from retail operations in Asia outside Singapore and Hong Kong puts assets on the block.

The Citi sale couldn’t have come at a better moment. DBS Chief Executive Piyush Gupta must be thinking hard about what he could snag from his former employer: India? Indonesia? Both? He doesn’t have the luxury of time. On its home turf, DBS is relatively safe for now. But new-age virtual banks, one from ride-hailing app Grab Holdings Inc. and another from mobile-games maker Sea Ltd., are coming to Singapore. Grab’s record $40 billion merger with a blank-check company gives it balance-sheet muscle, which it is bound to flex against DBS.

Luckily for the traditional lender, a revival in profit means it can buttress its Asian heft before challenger banks enter. A drop in new bad loans and a write-back of past allowances saw net income doubling from the previous three months to a better-than-expected S$2 billion in the first quarter, the bank said Friday. The thick cushion DBS built to absorb blows from Covid-19 disruption ought to come in handy this year as Singapore opens up, starting with a planned travel bubble with Hong Kong in May. Besides, with Singapore private home prices growing the fastest since 2018, mortgage loan demand is high.

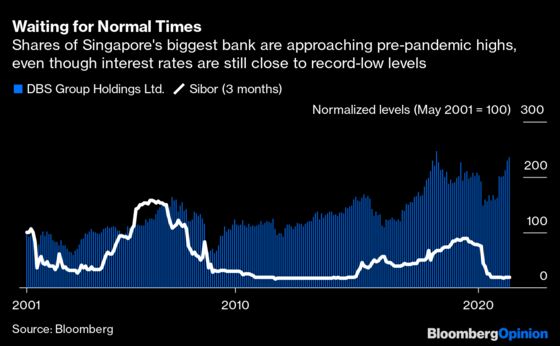

The loan pricing, though, is far from great. Pretty much the only thing weighing on earnings is the excess liquidity sloshing about in the island-state. It’s keeping a lid on interest rates DBS can charge customers. Net interest margin in the first quarter was 1.49%, unchanged from the previous three months. During the same period last year, the margin was 1.86%.

Investors aren’t waiting for interest rates to normalize. For them, it’s enough that credit volumes are coming back. Gupta said he’s upgrading the outlook for full-year loan growth to “mid-to-high single digits.” Shares of DBS and its two smaller Singapore peers, Oversea-Chinese Banking Corp. and United Overseas Bank Ltd., have jumped 40%-plus since last October.

DBS should also expect a boost from the nervousness over Hong Kong’s openness and rule of law as Beijing tightens its grip. The greater the exodus of money and talent from the special administrative region, the bigger the opportunity for traditional rival Singapore to bulk up as a financial center.

As a bank from politically neutral Singapore, DBS might even fancy its chances in Beijing’s ambitious Greater Bay Area. That capital-guzzling plan to connect Hong Kong with cities in southern China is a more natural bailiwick for HSBC Holdings Plc. But the London-headquartered lender is badly entangled in economic confrontations between the People’s Republic and the West. By paying top dollar to become the largest shareholder of Shenzhen Rural Commercial Bank Corp., Gupta is signaling his intention to play.

And why not? As I have argued before, Singapore’s largest bank is too dependent on its home market. Nationalist politics in Indonesia thwarted its $6.5 billion purchase of PT Bank Danamon, which eventually fell in the lap of Mitsubishi UFJ Financial Group. That was eight years ago. Since then, DBS has acquired Australia & New Zealand Banking Group Ltd.’s retail and wealth businesses in Singapore, Hong Kong, China, Taiwan and Indonesia. More recently, it took over the assets and liabilities of Lakshmi Vilas Bank Ltd., a troubled Indian lender the central bank wanted to put out of its misery.

None of this comes cheap. Half or more of the 3% to 4% increase this year in DBS’s expenses from pre-pandemic 2019 levels will be on account of Lakshmi Vilas. But these “bolt-on” acquisitions, as Gupta terms them, will complement investment in digital banking. The technology push will go beyond consumer banking. Together with JPMorgan Chase & Co., and Singapore state investment firm Temasek Holdings Pte, DBS is taking part ownership of a new blockchain-based platform for instantaneous settlement of cross-border payments between financial institutions. Offering services in tokenized money to corporate clients could see DBS open a fresh battlefront against Citigroup, HSBC and Standard Chartered Plc, the global-local, or “glocal,” trio that dominates transactions banking in Asia.

Citi’s slimming down gives DBS the opportunity; Grab’s impending arrival provides the motive; and a post-pandemic upswing in profitability supplies the wherewithal. Expect Gupta to crank up the M&A machine.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2021 Bloomberg L.P.