(Bloomberg Opinion) -- The hedge fund industry boasts some of the best money managers on the planet, but good luck investing with them. There are precious few, and it’s never clear who they are in the beginning. By the time their skills are apparent, they’ve already amassed a fortune and no longer need investors’ money.

Investors were reminded of that quandary last week with the news that David Tepper, founder of hedge fund Appaloosa Management, plans to return money to outside investors and focus on managing his own fortune, which includes the Carolina Panthers football team he bought last year. Tepper founded Appaloosa with just $57 million in 1993 but soon closed the fund to new investors as his fame grew and money poured in. Those who weren’t invested with Tepper from the start, or close to it, never had the opportunity.

Tepper is the latest in a long line of elite managers who have left the game in recent years, or plan to, including Richard Perry, Eric Mindich, John Griffin, Neil Chriss, John Paulson, Alan Fournier and Leon Cooperman. It’s hard to blame them. They don’t need the money. The trades are increasingly crowded. And with the rise of low-cost options, the fees that hedge fund managers demand seem more exorbitant than ever to investors.

But elite managers are the lifeblood of the hedge fund industry. They hold out the promise that the next great manager is waiting to be discovered, and no one embodied that promise better than Tepper.

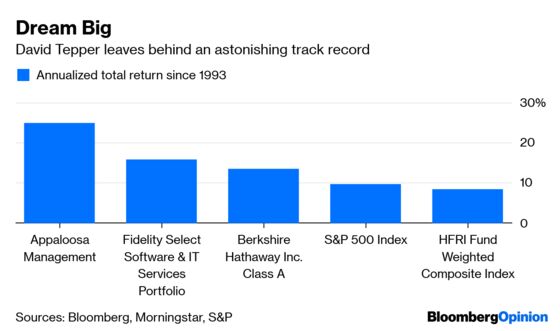

The track record Tepper leaves behind is otherworldly. Appaloosa has returned 25% a year since inception in 1993, according to Bloomberg News. To put that in perspective, a $10,000 investment in the fund in 1993 would now be worth roughly $3.6 million. By comparison, the same hypothetical investment in the HFRI Fund Weighted Composite Index, a broad collection of hedge funds, would be worth just $85,000. The S&P 500 Index and Berkshire Hathaway Inc. would have yielded $114,000 and $277,000, respectively. And an investment in the best performing mutual fund since 1993, according to Morningstar, the Fidelity Select Software & IT Services Portfolio, would be worth $476,000, still a mere fraction of Tepper’s bounty.

With numbers that good, it’s hard to chalk up Tepper’s results to luck. Appaloosa doesn’t publicly disclose its results, but based on numbers compiled by research firm GuruFocus, Tepper outpaced the S&P 500 by roughly 17 percentage points a year from 1993 to 2014, including dividends. It’s highly unlikely an outperformance of that magnitude is the result of chance. (For finance aficionados, that’s a t-statistic of 2.6.)

Like many elite managers, Tepper showed some unusual traits. One is the foresight to put performance ahead of fees. Appaloosa has returned money to investors in eight of the last nine years, according to Institutional Investor, continuing a “long-standing policy of returning capital to its investors in order to maintain a size that would maximize returns.” It hasn’t hurt Tepper. He ranks 120 on the Bloomberg Billionaires Index, with an estimated net worth of $11.2 billion.

Tepper also had a knack for knowing when to take big risks. Appaloosa was seven times more volatile than the HFRI index from 1993 to 2014, as measured by annualized standard deviation, three times more volatile than the S&P 500, and twice as volatile as Berkshire Hathaway’s stock. But more of that volatility can be attributed to Appaloosa’s ups than its downs, owing to Tepper’s penchant for making deeply contrarian bets.

His maneuvers around the previous two downturns are illustrative. In the aftermath of the dot-com bust, GuruFocus estimates that Tepper was down 25% in 2002, roughly in line with the S&P 500. But when the recovery took hold the following year, Tepper was up 149%, or 120 percentage points more than the market.

He navigated the 2008 financial crisis just as skillfully. He was down roughly 27% in 2008, or 10 percentage points better than the S&P 500. When the market recovered in 2009, he was up 133%, or 106 percentage points more than the market.

Still, Tepper and other elite managers can’t play the game forever, and their retirement makes room for a new generation of stars. The question is whether hedge fund investors still have the will to find them. The industry must hope that when Tepper exits, the dream of discovering the next great manager doesn’t go with him.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nir Kaissar is a Bloomberg Opinion columnist covering the markets. He is the founder of Unison Advisors, an asset management firm. He has worked as a lawyer at Sullivan & Cromwell and a consultant at Ernst & Young.

©2019 Bloomberg L.P.