IPO Best in Show Doesn't Go to WeWork, Uber or Lyft

(Bloomberg Opinion) -- Many of us have been fixated on WeWork’s struggle to go public and the disastrous post-IPO stock performance of high-profile startups Uber Technologies Inc. and Lyft Inc. But as has often been true in the last few years, the tale is different for the unglamorous tech companies that are running circles around their cool peers.

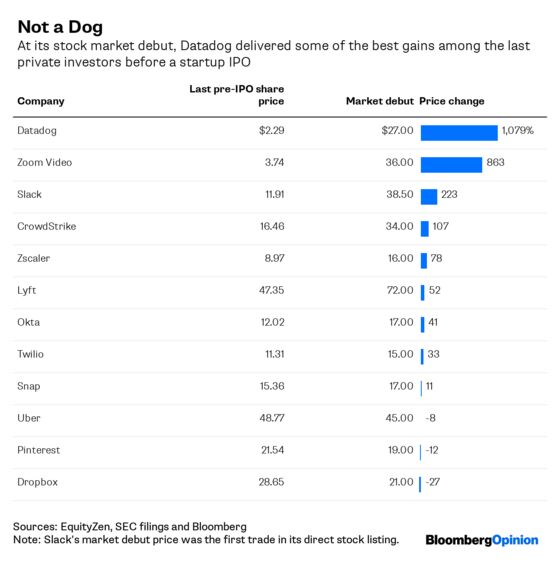

The latest example is Datadog Inc., which helps companies monitor the health of their apps and computing infrastructure; it sold its first batch of public stock late Wednesday. If you fell asleep reading the description, let me wake you up by saying that the company’s most recent pre-IPO investors have a nearly 1,100% gain on their shares in less than four years, according to figures from EquityZen, a marketplace for private stock sales. The earliest Datadog stock buyers from 2011 have a nearly 50,000% gain.

In a non-systematic look at more than a dozen other tech companies that have gone public in the past couple of years, the stock gain for Datadog’s pre-IPO investors is at or near the top of the leader board.

Repeatedly, the less-buzzy startups like Datadog that sell cloud-subscription software to businesses have been the ones that deliver the goods for early backers. There have been exceptions, but companies like Zoom Video Communications Inc. and Slack Technologies Inc. — the coolest of the Zzzz crowd — have tended to produce strong returns for pre-IPO investors, and their public shares have typically done well, too.

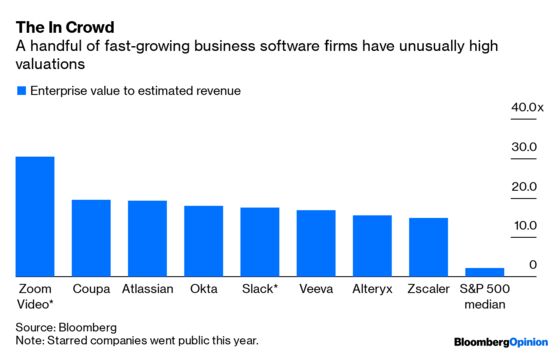

Investors, both public and private, love these software-as-a-service companies. Generally their technology is better than anything that came before — if there was an old-guard technology with similar functions — and once businesses use the software and stitch it together with email, calendars, information databases and other corporate systems, it can be tough to ditch. If they’re managed properly, these business software companies can grow fast and predictably.

Among the tech companies that have gone public on U.S. stock exchanges since the beginning of 2018, nine of the top 10 by stock gains from their IPO price are software companies that sell to businesses, according to data compiled by Bloomberg. (No. 1 is Zscaler Inc., whose share price has more than tripled since its March 2018 IPO, despite a recent drop.)

What are the lessons here? Well, not surprisingly, it may be that the consumer-oriented tech companies with lots of attention as startups may be great companies but not necessarily great investments if the hype leads to overvaluation. That’s particularly true — as in the cases of Uber, Lyft and WeWork — when public company investors are far more dubious than private investors about companies with unproven business models and unsteady financial metrics. The other lesson may be that you’re in luck if you founded a company in a sector like business software that, at least for now, is the apple of investors’ eyes.

These young cloud software companies are also priced for growth to the point where they are vulnerable to any hiccup in customer acquisition numbers or revenue gains. That has happened recently, when companies like Zscaler, Alteryx Inc., PagerDuty Inc., CrowdStrike Holdings Inc. and New Relic Inc. reported wobbly financial results, changes in management or were just infected by worries from other companies in their sector.

Still, Datadog shows the benefit of being the right kind of business at the right time. Bloomberg News reported Wednesday that Cisco Systems Inc. approached Datadog recently with a takeover offer significantly higher than the $7 billion valuation it had been shooting for in an IPO. (As of Thursday’s early stock market trades, Datadog is valued at about $11 billion, excluding the value of shares held by employees and others.)

Datadog was apparently confident enough in its prospects to turn that down and opt to go public. The uncool companies truly are that cool.

Those investors include Iconiq Capital, the investment fund that has managed money forMark Zuckerberg of Facebook and other affluent people and institutions in Silicon Valley and beyond. Other stock buyers included Index Ventures, OpenView Ventures, Amplify Partners and Contour Ventures, Datadog announced in early 2016.

I will say that it's unusual for tech startups these days to go public without selling stock or doing other cash collections in the four years before an IPO. Some startups can't go four weeks without needing fresh cash.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shira Ovide is a Bloomberg Opinion columnist covering technology. She previously was a reporter for the Wall Street Journal.

©2019 Bloomberg L.P.