(Bloomberg Opinion) -- Cars are very important to oil producers, obviously. Not just because they drink up the stuff. They also offer a ghost-of-Christmas-future dose of foresight.

Daimler AG, the epitome of luxuriously engineered combustion, just slashed its dividend by 72%. As my colleague Chris Bryant wrote here, Tuesday’s announcement capped a string of profit warnings and other setbacks. That the stock actually rose briefly on this news tells you just how desperate investors were for a strategic reset, Band-Aid rip notwithstanding.

It is the cut to Daimler’s payouts that should have oil executives sweating.

Coronavirus has made amateur virologists out of many an investor, with the emphasis heavily on “amateur.” Tuesday morning saw oil prices, and stocks, surge as the market made one of its habitual segues from rank fear to blithe optimism. The truth is that, whatever the current rate of new infections, the sector already has a chronic condition: cost-of-capital-itis.

Like Daimler, oil majors are juggling the demands of investing during a downturn, planning for a sea change in their business, and keeping investors sweet with payouts. Royal Dutch Shell Plc and BP Plc now yield roughly 7%. Even mighty Exxon Mobil Corp. now yields close to 6%, the highest since the merger that spawned the combined company.

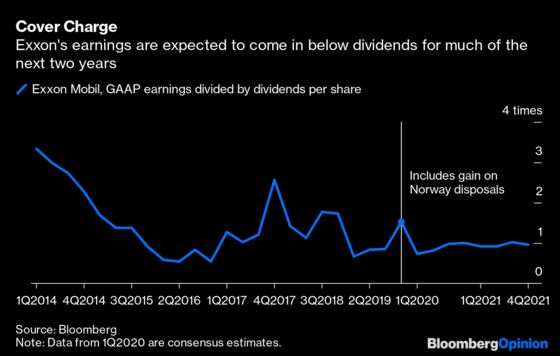

Exxon’s valuation looks especially vulnerable. Its recent exploration success, a virtual guarantee of high multiples in years past, is now viewed as a call on cash shareholders would rather have. Its integrated model has offered little respite in this weak oil market, with fourth-quarter results from the chemicals business especially poor — even before coronavirus piled on in this quarter. As it stands, the company has been selling assets and taking on debt to meet payouts, and consensus forecasts imply earnings will struggle to cover dividends through this year and next.

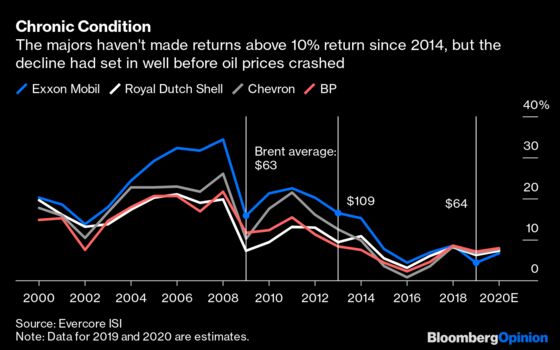

The underlying cause is a collapse in return on capital, due to a wave of heavy spending on the back of the last commodity supercycle (when China offered an unalloyed boost). Returns have not only dropped but also compressed in range between the majors.

Analysts at Evercore ISI estimate Exxon’s return on capital employed dropped to just 4.4% in 2019, on par with 2016 — when average Brent crude prices were 30% lower. Looking at Exxon alongside Chevron Corp., BP and Shell, it is telling that average returns for the group in 2013 — the last full year of triple-digit oil prices — were roughly those of 2009, just after the financial crisis. This problem predates not just coronavirus but also the oil crash.

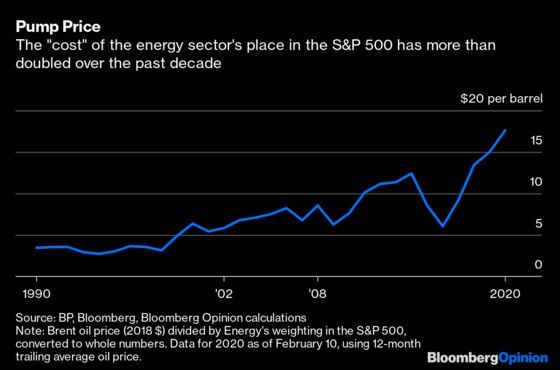

This really becomes apparent when comparing energy’s share of the S&P 500 with oil prices. The chart below divides the annual real Brent oil price by energy’s weighting to provide a ratio that can be thought of like this: How many real dollars per barrel does it take to buy the sector one percentage point in the S&P 500?

Hence, investors are demanding more. Compounding this is the issue Daimler also faces: transition.

One of Daimler’s failures has been its relatively slow development of electric vehicles. From one angle, that seems like a reasonable approach for an incumbent: Let others make mistakes and lose money developing a new market, and then deploy one’s established brand and resources to clean up when the concept has been road-tested. In practice, financial markets are nonplussed.

It has become a cliche to say Tesla Inc.’s supercharged market cap is now a multiple of stalwarts such as Daimler’s, despite the California upstart’s miniscule market share. Don’t get me wrong; I cannot justify Tesla’s valuation on its fundamentals or any reasonable projection (see this). But that is kind of the point. Many of Daimler’s problems — high costs, production delays and even legal tangles — are all familiar at Tesla too. Yet the latter has gotten a pass. It may not be right, but as the old saw goes, irrationality’s bank balance can be way bigger than yours.

A few years back, when Tesla was worth a mere $30 billion, I wrote oil majors should fear the company. Not because it would necessarily conquer the world. Rather, because investors were falling over themselves to give it capital in the absence of domination (or profits), in marked contrast to their treatment of the cash-spewing titans of oil. Imagine the fallout if Exxon CEO Darren Woods took to Twitter (in fact, just pause on that idea for a second) and announced a fanciful take-private deal. I’m no prophet, but I’m pretty sure (a) the stock wouldn’t have almost tripled since and (b) he would no longer be CEO.

Daimler’s predicament is another reason to be fearful. Like the majors, it must convince investors that, despite past failings, it has what it takes to make the right choices (and bets) in an energy-transportation complex undergoing profound change after a century of incumbency. Like them, it must somehow make the necessary investment using capital that has become scarcer, and therefore pricier.

On Wednesday, BP’s new CEO (and Instagrammer) Bernard Looney is due to lay out his vision for navigating this new world. Without wishing to front-run his speech, it’s worth reading these comments made by Daimler boss Ola Kallenius on Tuesday:

We understand that we are in transformation. Yes, the auto industry in the next years, next decade is going to change fundamentally. This company is going to change fundamentally. We are prepared to take the actions and the measures that we need to take to make sure that we come out as a winner of this transformation

Swap in “energy” for “auto,” and Looney could repurpose those words effortlessly. Change is now a constant for this business, and it has the yields to show for it.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2020 Bloomberg L.P.