(Bloomberg Opinion) -- The oil market is taking reports of the death of crude surprisingly well.

Crude jumped to its highest level in more than a year Friday, on signs that inventories are declining amid a hoped-for recovery from Covid-19. Brent moved as high as $59.12 a barrel, within a whisker of the $60 level where swathes of the industry find it easy to balance their books.

There’s a lesson in all this from the second-most consumed commodity, iron ore, and how it has handled the ups and downs of the past decade. Many oil producers still see the end of 150 years of almost uninterrupted demand growth with trepidation. If the iron ore industry is any guide, though, small may still prove to be beautiful.

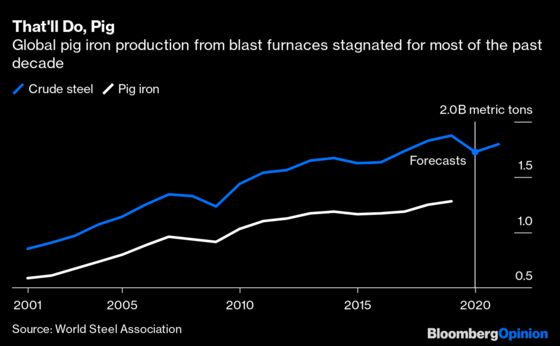

While steel production has continued to grow in recent years, the bit of it that matters to iron ore producers has mostly stagnated. Global output of pig iron — the hot metal that comes out of blast furnaces — grew at an average 6.2% a year in the decade through 2012. In the subsequent five years, that pace slowed to 1.1%.

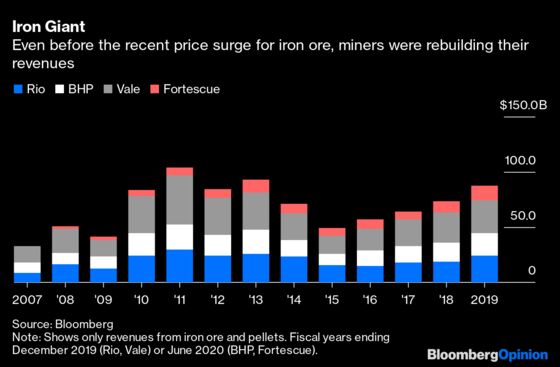

That ought to have been bad news for the people digging rust out of the ground — and, indeed, in 2015 they had a brush with death due to signs that Chinese steel demand was drying up altogether. Once that storm settled and demand regained a measure of equilibrium, though, BHP Group, Rio Tinto Group, Vale SA and Fortescue Metals Group Ltd. found business rather profitable:

What happened? The best argument is that the bull case for iron ore went from a demand-led to a supply-led story. A short spike of extreme demand — like the one we saw last year, driving ore prices to a multi-year high of $176 a metric ton — provides a nice sugar boost. When demand growth is both strong and sustained, though, margins suffer, as miners spend all their cashflow on an orgy of capital expansions to provide the extra raw materials that consumers are crying out for.

Put that way, the end of demand growth isn’t all bad. The machinery built and deposits developed at the peak of the market should be able to keep chugging along, without adding too much more, reducing capex budgets. So long as producers are able to restrain supply, prices should hover around profitable levels. Once you’ve dealt with the debt hangover from boom times, business starts looking a lot more sane and sensible than it was in the glory days.

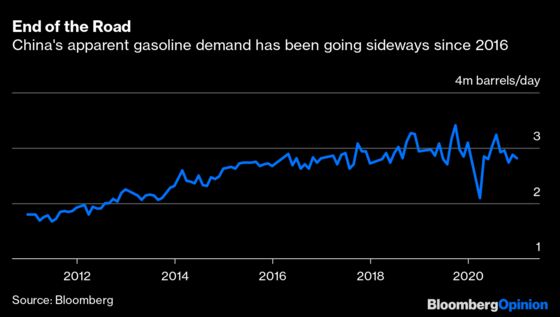

That’s the best case for what could be happening in the oil market right now. For all the apparent strength of crude demand growth out of China, there’s still very little sign that transport consumption is going to resume its upward trend, as my colleague Julian Lee has written.

China’s apparent gasoline demand has gone sideways for five years, with most of the growth in refinery output soaked up by exports. Covid-19 shows little sign of reversing that. Indeed, looking down the list of China’s major refinery products, it’s hard to see any that have seen a sustained improvement in consumption over the past year, with the exception of a minor bump in kerosene that matched the brief recovery in the country’s aviation industry.

That suggests growth is being driven by less-noticed fractions used as feedstock for China’s fleet of new petrochemicals plants — ultimately representing a shift in the location of the global chemicals and refining industry, rather than an increase in ultimate end-user demand.

As we’ve argued, the prospect of a plateau or decline in crude demand may not initially be as bad for oil producers as feared. Saudi Arabia, for instance, may see healthier oil revenues from throttling back output than opening the spigots. That’s one possible explanation for its current willingness to shoulder the burden of supply restraint within OPEC+ on its own. Even Exxon Mobil Corp., the industry’s most perennial demand bull, seems to be capitulating to peak-ism, judging by its own spending plans.

Maintaining that happy equilibrium depends on accepting that the world has changed. Iron miners have shown impressive conformity in refusing to ramp up capital spending to previous levels in spite of their healthier profits in recent years — helping in the process to keep supply tight and prices elevated.

Oil producers are a much larger and more disorderly bunch, one reason the likes of OPEC+ exist in the first place. The biggest players will have to work harder than ever to enforce the sort of supply restraint that the miners have exhibited. If Big Oil wants to make the most money out of petroleum’s twilight years, the first step is accepting that the oil era is really coming to an end.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2021 Bloomberg L.P.