Crispin Odey Makes a Killing on Britain's Retail Apocalypse

(Bloomberg Opinion) -- As the e-commerce boom lays waste to bricks and mortar retailers, it was only a matter of time before Britain’s high street landlords were hobbled too. U.K. shopping center owner Intu Properties Plc is at the epicenter of this particular storm and is ill-equipped to cope because it has too much debt.

A trading update this week confirmed that it’s in a very tight spot and raising equity is now considered “likely.” The stock dropped 24% over two trading sessions, swelling total losses over the past year to 84%. Hedge Fund Odey Asset Management and other short-sellers have made a killing here. Shareholders’ best hope of salvaging more value is that someone makes a takeover bid.

Intu’s misfortunes stem from renting space to troubled retailers such as Arcadia and Monsoon, which entered so-called company voluntary arrangements (a mechanism to close stores and cut rent). The mall owner expects net rental income to drop about 9% this year and continue falling next year.

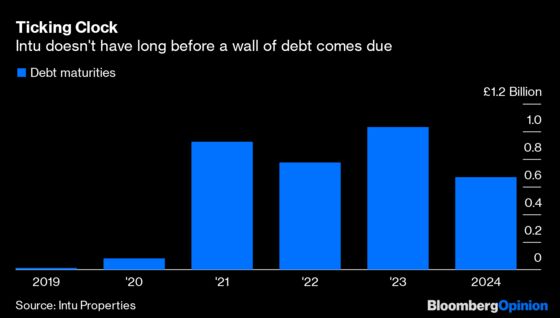

That might not sound too dramatic, but it’s a huge problem for a company with 4.7 billion pounds ($6.1 billion) of net debt and hefty near-term refinancing needs. More than 900 million pounds of those borrowings fall due in 2021.

Intu’s debts are equivalent to a whopping 58% of the dwindling market value of its properties, putting it uncomfortably close to breaking some of its debt covenants. The dividend has already been suspended — a drastic move for a real estate investment trust — but management hasn’t made much progress generating cash and reducing leverage.

The company is talks to sell three Spanish sites, which should free up a few hundred million pounds of cash. U.K. asset sales are also under consideration. The trouble is that the market for British retail property transactions has ground to a halt and Intu will be viewed as a forced seller. So it’s hard to be optimistic about the proceeds. Brexit uncertainty and a pre-Christmas election won’t help Intu’s current or prospective tenants.

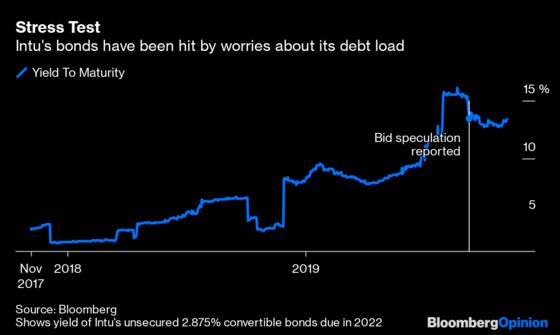

The group’s 375 million pounds of 2.875% coupon convertible bonds due in 2022 now yield 13%. This is the credit world equivalent of the “sad face” emoji and a sign the company would have difficulty raising more unsecured borrowing.

While raising equity looks unavoidable, Intu has waited too long. With a market capitalization of just 417 million pounds, a rights issue would probably be highly dilutive to existing shareholders and they’ll get a vote on whether it goes ahead.

Anyone considering a takeover bid at a premium to the current share price would be taking a huge risk in view of Intu’s huge financial liabilities and waning capacity to meet them. Still, Intu attracted two failed offers last year when the share price was much higher. Now it trades at a massive 85% discount to what the company calculates its net assets are worth.

Those asset values probably have further to fall but Intu’s malls have some high quality tenants, decent footfall and occupancy rates. Bid speculation gives faint hope to stockholders and might yet crimp Odey’s profit.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2019 Bloomberg L.P.