(Bloomberg Opinion) -- As the board of Credit Suisse Group AG meets this week to discuss a strategic review, the names of external forces can be attached to the bank’s troubles: Greensill and Archegos, two broken finance businesses that hurt its bottom line and its clients. But the ongoing crisis at the Zurich-based institution springs from within: Credit Suisse was desperate to hit profit targets and stopped looking at how it made them.

It needs to steady the ship and course-correct quickly. Prolonged uncertainty will only give rivals time to woo away more of its most productive bankers and highest-paying clients. There are questions whether Chief Executive Officer Thomas Gottstein is up to the task. He took the job in February 2020 after Tidjane Thiam resigned amid scandal and controversy. Over the weekend, António Horta-Osório — the bank’s chairman since April — tried to calm speculation by saying Gottstein had his full support during an interview with a Swiss magazine.

Some analysts are calling for radical changes — including the sale of Credit Suisse’s volatile investment banking division. That depends on where Horta-Osório — a clear-thinking, unsentimental executive simply referred to by his initials AHO in the industry — decides the problems are. Credit Suisse channeled $10 billion of client money to Greensill, a British finance company, which collapsed; and then it lost $5.5 billion on funding trades for Bill Hwang’s aggressive family office Archegos, which blew up spectacularly. Greensill emanated from Credit Suisse’s asset management division. Archegos from the investment banking side.

Blame for Credit Suisse’s Greensill mess comes at least partly down to inattention. The Swiss bank did not seem to have been alarmed that Greensill had previously caused problems at GAM, another fund manager. Typically, Credit Suisse would manage funds that bore its own name; but, in this case, it was Greensill that selected and managed the assets. Credit Suisse also did not always know exactly what Greensill was doing with the money. Out of $10 billion invested, $3 billion may never be recovered. Credit Suisse’s wealth and asset management arms had seen healthy net inflows each quarter since the start of 2019; these turned to net outflows of 6 billion Swiss francs ($6.5 billion) in the second quarter of this year.

The Archegos losses were the result of a much deeper rot, catalogued in a frank report by lawyers that was commissioned by the board and published this summer. Before it came to light, Credit Suisse had already lost $214 million when Malachite Capital Management, a hedge fund, defaulted on financing in early 2020. The bank, said its lawyers, “failed to effectively address a culture that encouraged aggressive risk-taking and injudicious cost cutting.” Malachite and Archegos traded different instruments but both were overseen by the same unit at Credit Suisse.

Of the two, Greensill looks like an idiosyncratic error; Archegos more systemic. While it has knocked client confidence, the first episode might arguably be a one-off, an act of carelessness. The Archegos scandal, however, reveals wider shortcomings in how Credit Suisse ran its trading division. Cost cuts in recent years reduced the number of staff responsible for oversight, each burdened by more and more hedge fund clients. Some senior employees were wearing so many hats they struggled to do their jobs.

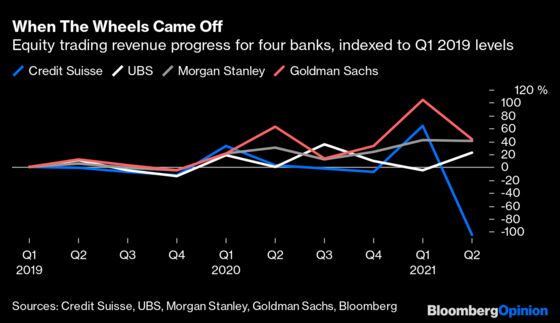

The bank had been stretching too far to try to perform. In the past three years, it made more revenue per dollar of capital in its investment banking business than any other European or U.S. rival, according to Alastair Ryan, an analyst at Bank of America Corp. That has turned out not to be a good thing. Revenues crumbled in the second quarter as it slashed risk in response to the Archegos losses.

Credit Suisse could redirect its strategy by selling the investment bank, if anyone were willing to buy it, or simply by spinning it off to shareholders as standalone business. That may be radical but it’s worth considering because the division’s biggest business lines are things like American mortgage bonds and loans for private equity deals that aren’t relevant to private banking, wealth and asset management — the areas that Credit Suisse wants to be its central focus. Still, there’s a good chance a separation — which would require restructuring charges, extra capital requirements and higher funding costs — could make the wealth businesses and the investment bank worse off at least for a few years.

Local rival UBS Group AG is one of the few banks that have successfully shut down a large chunk of risky, underperforming investment banking operations. That was extremely costly, but UBS closed its most capital-hungry, debt-related units at a time when its losses from the 2008 financial crisis were so big that the additional pain wasn’t too noticeable. The time it took to stabilize UBS allowed Credit Suisse to gain wealthy client assets at its rival’s expense for several years.

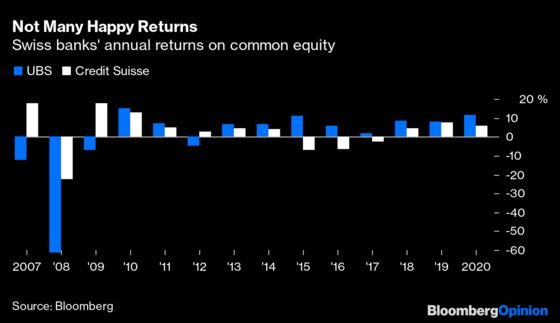

But the boot has long since been on the other foot. Credit Suisse hasn’t produced a return on equity of more than 10% since 2010 and it hasn’t beaten UBS’s return on equity since 2012, according to Bloomberg data.

The trouble is that Credit Suisse’s investment bank has produced just enough profits to convince executives that with a little more pressure, they can hit their targets. That attitude has been exposed by Archegos as dangerously wrong.

The bank’s errors have left it in a double bind. It needs to convince rich clients and shareholders that it can still be trusted with their money. But as it recoils from risk-taking, it will also have to spend more on technology and on employing the kind of staff who can say “No” to trades. That will drag profits down and make it less attractive.

The board and AHO need to decide what to do quickly. Take too long and Credit Suisse will lose people, clients and investors.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Paul J. Davies is a Bloomberg Opinion columnist covering banking and finance. He previously worked for the Wall Street Journal and the Financial Times.

©2021 Bloomberg L.P.