(Bloomberg Opinion) -- Fund managers are grappling with how to incorporate environmental, social and governance considerations into their portfolios. A movement that started in equities has spread across asset classes. For credit investors, the trick to investing with a conscience without hurting returns may lie with which corporate bonds they load up on as much as with those they choose to shun.

Chris Bowie, who helps oversee 15 billion pounds ($18.5 billion) as a partner at TwentyFour Asset Management in London, has used his Absolute Return Credit strategy as the basis for testing what incorporating ESG into his bond selections would have done to returns. The fund aims to deliver 2.5 percentage points more than cash and is restricted to holding no more than 100 investment-grade bonds.

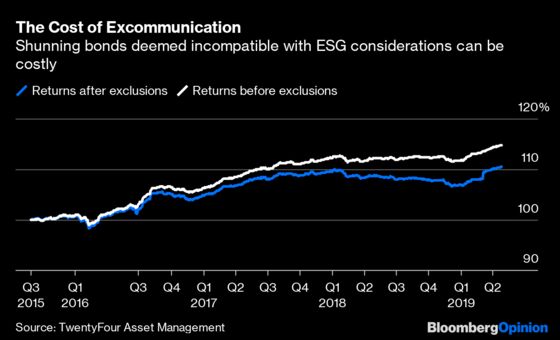

Bowie started by excluding debt issued by companies involved in industries such as tobacco, gambling, alcohol, oil and gas, a process called negative screening by the fund management industry. That eliminated nine securities the fund had owned at some point during the four-year period he studied.

The effect on returns was tangible – and detrimental, to the tune of a full percentage point per year.

As well as eroding how much money the fund made, the exclusions also increased its volatility. At TwentyFour, part of Swiss firm Vontobel Holding AG’s stable of fund management boutiques, that outcome threatened to make sustainable investment in credit “a non-starter,” Bowie says.

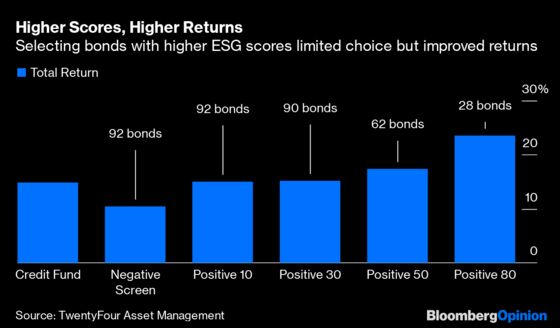

So he extended the portfolio selection process to include so-called positive screening. All of the bonds the fund could potentially buy were scored and screened, ranging from a minimum of 10 for the least favorable from an ESG perspective to 80 for those deemed most acceptable. Constructing different portfolios by raising the ESG score threshold reduced the number of eligible bonds at each level – but also generated higher returns.

At the highest score, though, the only bonds available were either asset-backed securities or debt issued by financial companies, flattering the returns and producing a portfolio that’s too concentrated.

The solution, Bowie reckons, is to set the threshold low enough to capture enough bonds to provide diversification. That, combined with the negative screening, can produce a portfolio that’s more socially responsible but with similar return and risk characteristics as a non-ESG fund.

Myriad studies are available purporting to prove both that socially responsible investing hurts returns, and that it can boost performance. Bowie, who says he’s still considering marketing a sustainable credit fund, reckons there could be a “seesaw” between the two opposing strategies:

“There will possibly be long periods where sustainable mandates outperform as capital flows into those companies, lowering their cost of capital and generating capital gains for existing holders. But consequently, the relative cost of capital for non-sustainable companies will likely rise to a point where the yields on offer give an advantage to strategies that can allocate to them.”

Cliff Asness, the billionaire co-founder of AQR Capital Management, argued a few years ago that the point of ESG-driven investment is to raise the cost of capital for what he called sinful companies, which in turn would mean higher returns for less virtuous investors.

That strikes me as plausible. But with issues such as the climate crisis and the gender pay gap finally getting the attention they deserve, more of us should be willing to make monetary sacrifices in the cause of making the world a better and safer place.

To contact the editor responsible for this story: Melissa Pozsgay at mpozsgay@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.