Fed Is Getting Awfully Close to Backing Apple Stock

(Bloomberg Opinion) -- It doesn’t take much imagination to see the Federal Reserve supporting the stock price of Apple Inc.

The central bank’s Secondary Market Corporate Credit Facility recently released details about its “Broad Market Index,” which is a roadmap for which individual bonds it will buy for its portfolio after changing the rules to avoid forcing issuers to certify they’re in compliance with the Coronavirus Aid, Relief, and Economic Security Act. Just looking at the 13 companies with weightings of at least 1%, which collectively make up almost one-fifth of the index, a few things stand out. First, there are six automobile companies, with subsidiaries of Japan’s Toyota Motor Corp. and Germany’s Volkswagen AG and Daimler AG as the three largest issuers overall. In fourth is AT&T Inc., the largest nonfinancial borrower due in no small part to its $85.4 billion takeover of Time Warner Inc.

Then there’s Apple. As a reminder, it’s the largest U.S. company by market capitalization at $1.57 trillion, edging out Microsoft Corp. and Amazon.com Inc. Its shares have easily rebounded from the selloff caused by the coronavirus pandemic, rallying 24% so far in 2020. Yes, Apple has about $100 billion of debt outstanding, but it’s also known for having one of the largest cash piles in the world. It’s so big, in fact, that the company could repay all its obligations and still have roughly $83 billion left over.

With so much cash, that naturally raises the question: Why does Apple take on debt in the first place?

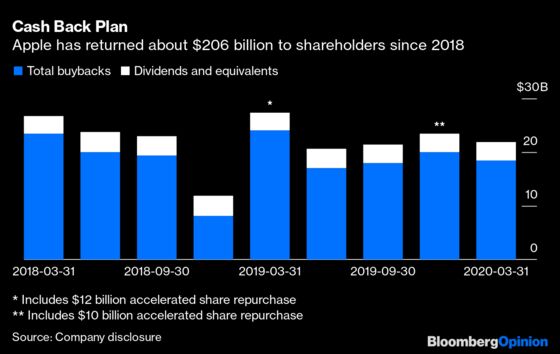

In each of Apple’s past three dollar-bond sales, in November 2017, September 2019 and May, the company said it would use proceeds at least in part to repurchase common stock and pay dividends under its program to return capital to shareholders. In total, the company has doled out more than $200 billion since the start of 2018. It’s easy to see why company leadership would see it as too cheap not to borrow. Apple has the second-highest investment-grade credit ratings from Moody’s Investors Service and S&P Global Ratings, allowing it to issue $2.5 billion of 30-year bonds in May that yielded just 2.72%. Its $2 billion of three-year debt, within the Fed’s maturity range, priced to yield less than 0.85%.

Luca Maestri, Apple’s chief financial officer, said during the last quarter’s earnings call that the company has more than $90 billion in stock buyback authorization left, adding that it plans to continue the same capital allocation policy going forward.

Still, Apple openly using debt sales to help finance share repurchases puts the Fed in a somewhat awkward position. Chair Jerome Powell has consistently framed questions about its secondary-market facility in the context of supporting the central bank’s full employment mandate. Workers are “the intended beneficiaries of all of our programs,” he said in a hearing last month. It’s possible Americans “are able to keep their jobs because companies can finance themselves.”

And yet, the Fed’s secondary-market facility comes with no strings attached. In fact, as I noted last month, its maneuver to create Broad Market Index Bonds circumvented the CARES Act requirement that any company must have “significant operations in and a majority of its employees based in the United States.” Rather than focus on the American worker, the stated goal is to “support market liquidity for corporate debt,” and, by extension, keep borrowing costs down for creditworthy firms. So there’s every reason to expect that Apple can and will issue bonds again in the near future, at an even cheaper rate, to fund stock buybacks and dividends. That, in turn, would most likely support share prices.

That shouldn’t sit well with many people. Even President Donald Trump, who has used the stock market as a barometer of his economic policies, has signaled a preference for capital projects over buybacks. On March 20, just before the S&P 500 Index fell to its lowest level of the Covid-19 selloff, he lamented that companies used the money saved from his 2017 tax cut to repurchase shares rather than build factories. He said at the time that he would support a prohibition on buybacks for companies that receive government aid.

“When we did a big tax cut and when they took the money and did buybacks, that’s not building a hangar, that’s not buying aircraft, that’s not doing the kind of things that I want them to do,” Trump said. “We didn’t think we would have had to restrict it because we thought they would have known better. But they didn’t know better, in some cases.”

The Fed’s strategy for buying corporate bonds is passive enough that few would equate it to receiving direct assistance from the federal government. The same can’t be said about the central bank’s Primary Market Corporate Credit Facility, which as of last week is open for business. Companies that want to place bonds directly with the Fed must certify that they have “not received specific support pursuant to the CARES Act or any subsequent federal legislation” and “satisfy the conflicts-of-interest requirements of section 4019 of the CARES Act.” As my Bloomberg Opinion colleague Matt Levine described in detail last week, there’s a huge amount of paperwork for issuers, and the Fed has the right to demand its money back if the forms are wrong and companies use funds for unapproved reasons.

In all likelihood, these constraints will turn almost every company away from the Fed’s primary-market facility. Instead, finance officers will reap the benefits of the central bank’s broad secondary-market interventions to issue new debt to private investors at rock-bottom rates and with no such rules, as they have for the past three months. And Wall Streeters will be happy with business-as-usual in the credit markets.

To put it plainly one more time: The Fed didn’t have to loosely interpret the law to create this index of corporate debt. It was already following through on its pledge to buy exchange-traded funds and had a system in place for companies to become eligible for individual purchases. It chose this third route, encouraging headlines like “Buying Corporate Bonds Is Almost Easy Money, Strategists Say.” What could go wrong?

Now that it’s scooping up individual bonds issued for share buybacks without any stipulations, policy makers should be asked again why this program is the right way to go about supporting the recovery. The truth is likely that corporate America needs low-cost debt to survive. Apple and its shareholders are more than happy to tag along for the ride.

The Fed's facility has not yet purchased debt from all the companies in the index, at least according to its disclosure, which only covers the$429 million in bonds it bought on June 16 and 17. Its largest purchases were Comcast Corp., AbbVie Inc. and AT&T Inc.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.