A Rising Tide Lifts All Boats, Even Ever Disappointing M&S

(Bloomberg Opinion) -- A rising tide lifts all boats — even the good ship M&S.

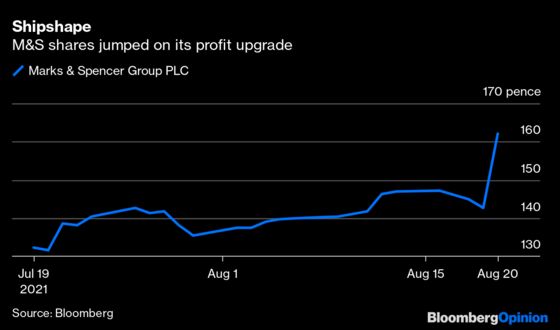

British retailer Marks & Spencer Group Plc has been a perennial disappointment to investors. But on Friday the household name said its underlying pre-tax profit would be above the upper end of its previous range of 300 million to 350 million pounds ($478 million) this year. The shares rose as much as 14%.

And yet, M&S has been in turnaround mode for much of the past 20 years. Investors need to see a sustained level of improvement to be convinced that this recent bit of good fortune is not another false start.

The company best known for its Percy Pig sweets, prepared meals and underwear said that changes implemented by chairman and retail veteran Archie Norman are starting to bear fruit. But Brits flush with lockdown savings and the demise of rivals are having an impact too.

Norman revitalized supermarket Asda Group Ltd. in the 1990s. His biggest move at M&S was buying 50% of Ocado Group Plc’s U.K. retail arm for 750 million pounds. Because online food sales are reported through Ocado Retail, they’re not reflected in M&S’s trading performance. Instead M&S receives a share of the joint venture’s post-tax profit.

Selling M&S food via Ocado does seem to have benefited the broader business. More people have been introduced to the brand thanks to the online supermarket. M&S has also increased its range of products and introduced cheaper items to complement its historic focus on food for special occasions.

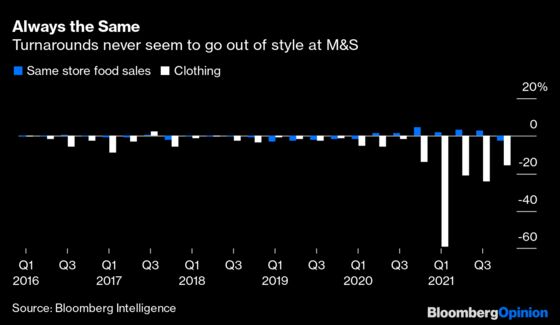

In clothing, M&S has cut its range but stocked more of its best sellers, for example dresses and jeans, which have been trending recently. It has also broken its tradition of selling only private-label clothing and now stocks third-party brands, such as environmentally friendly label Nobody’s Child, attracting new customers to the website. Some 14% of people who shop Nobody’s Child are new to M&S womenswear. And it introduced athleisure brand Goodmove just before the pandemic. Add in fewer markdowns, and full-price sales are up 9% on two years ago.

M&S has also been helped by factors outside of its control: Brits are flush with lockdown savings, and many are still not going abroad for their holidays or venturing out to restaurants. These trends are good for M&S’s food business, which is still well suited to preparing a fancy meal at home. Once you consider the fact that rivals, such as U.K. department store Debenhams and fashion chain Topshop, have disappeared from high streets, it would be more surprising if M&S were not firing on all cylinders.

But it’s worth remembering that Next Plc, a much more consistent performer than M&S, last month increased its full-year pre-tax profit forecast after sales were “materially ahead” of expectations. So M&S’s brighter outlook is merely a part of the pack, not ahead of it.

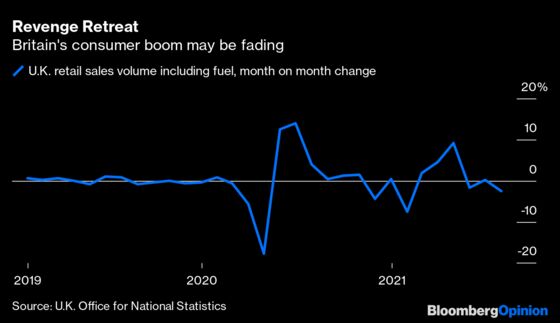

The real test for M&S will be what happens if consumer conditions cool. U.K. retail sales fell 2.5% in July compared with June. Economists had expected a 0.2% increase. Despite M&S’s efforts to make its food more affordable, if its customers’ incomes are crimped by a higher cost of living, they could trade down to cheaper supermarkets.

And while M&S has made operational improvements, there is more work to do in finding better store locations and sprucing them up. Despite several past chief executive officers investing billions of pounds in its stores, many still look dated. It’s telling that while online sales of clothing and home furnishings in the 19 weeks to Aug. 14 were up 62% from two years ago, store sales were still down almost 20%.

Right now there’s a significant amount of interest in taking over British retailers. A bidder might be tempted to finish what Norman started. But M&S would be a complicated purchase, in part because the retailer sells clothing as well as food — a split that could deliver value, but also makes the operations more complex.

Meanwhile, M&S owns less of its property than the supermarkets. Only 40% is freehold or subject to long leases, partly because some buildings are pledged to the pension fund. So there is less scope for a new owner to sell off M&S’s property or borrow against it.

Norman has little choice but to prove that M&S won’t sail into choppy waters once the post-pandemic consumer boost fades.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2021 Bloomberg L.P.