Expect Corporate Credit to Be a Port in the 2022 Storm

(Bloomberg Opinion) -- The European corporate credit market was feeling just a little sorry for itself in 2021. Activity was crowded out by massive sovereign issuance, with noticeable spread-widening in the fourth quarter. The corporate market certainly did not fire on all cylinders because of the persistence of Covid-19. And the pandemic looks to stretch deep into 2022.

All that, however, shouldn’t affect how investors look at credit spreads in the new year. Indeed, the differentials may increase the attractiveness of bonds from companies that are increasingly profitable as the virus loosens its grip. Healthy corporate credit will be more of a haven than burgeoning government debt.

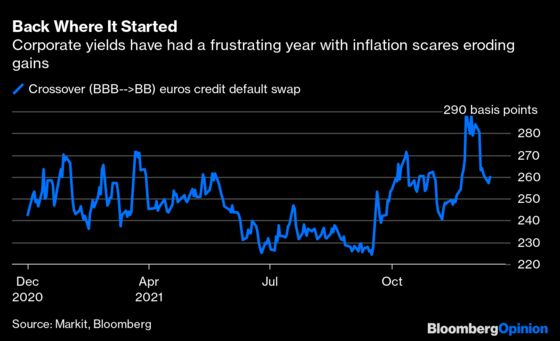

Spreads on European corporate bonds — the premium that companies have to offer over benchmark government bond yields — have had a rocky autumn and will likely end this year pretty much where they started. November was the worst month for sub-investment grade debt since the start of the pandemic as rampant inflation and logistical bottlenecks depressed market sentiment.

But this widening should make spreads look attractive again at the start of next year when investors review their asset allocations. Bob Michele, global head of fixed income at JPMorgan Asset Management, is pretty clear that corporate bonds look more appealing than government bonds. Case in point: the -0.35% of German 10-year bunds.

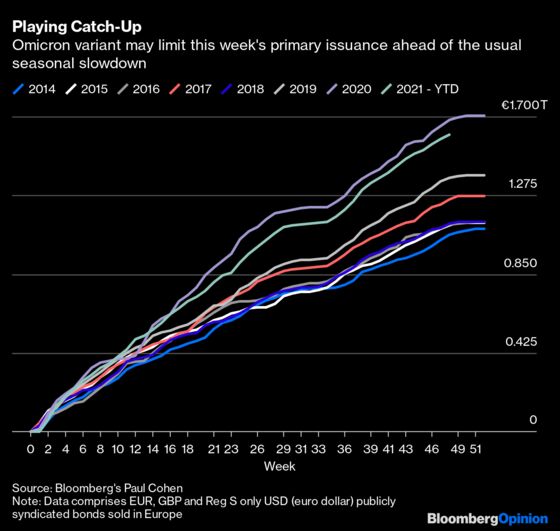

In 2021, new bond issuance in Europe of all currencies and sectors is likely to fall just short of 2020's record of 1.7 trillion euros. But within that, the corporate tally of 380 billion euros is 20% down this year. The omicron variant has all but shut the debt capital markets earlier than usual for the holiday season, with several deals postponed by corporate issuers at the riskier end of the spectrum.

Nonetheless, it has been a stellar year for European high yield bonds and leveraged loans, with supply nearing 300 billion euros ($340 billion). This is more than the amount maturing over the next two years, so it’s going to make it hard to repeat such large issuance totals with less pressure to raise debt.

Ethical debt took a record 44% share in Europe in November, with nearly a third overall for the year. The European Union itself is responsible for a large chunk of this: About one-third of the 800 billion-euro EU NextGeneration recovery fund will be raised in green debt through the middle of the decade. ING Groep NV analysts see a range of one to 10 basis points of “greenium” for ESG issues over comparable conventional debt. Corporations can see the carrot. And investors are tripping over themselves to “greenify” their portfolios. It’s a trend that's here to stay and Europe is leading the global charge. Sovereigns, supranationals and agencies — led by the EU — will continue to dominate new issuance league tables as government debt magically turns green, too.

The good news is that — with spreads over government bonds looking less skinny — markets will reopen in the new year with pent-up demand from investors who want to diversify into corporate debt. It is not all bad for corporate issuers: Government bond yields have corrected lower so overall issuance costs should be little changed. If the economic climate remains balmy, one bad quarter should be easily shrugged off. On balance, with several factors limiting issuance, corporate spreads and activity should hold reasonably well next year — worsening Covid variants aside.

Companies that needed to issue debt have already taken advantage of the amazingly benign conditions afforded by the huge monetary and fiscal pandemic recovery stimulus — with the abundance of cheap financing increasing the propensity to borrow at much longer durations. Unicredit SpA analysts note that the average maturity of eurozone medium- to long-term government bond issuance rose to an all-time high of almost 11 years in 2021, though they expect that to start reversing next year. Credit duration has naturally followed longer, too.

Banks also look in reasonable health as investment banking has propelled profit growth. There is plenty of access to loans with trillions of euros of European Central Bank largesse available in targeted long-term refinancing operations. That means lots of avenues for companies to stagger and structure their debt needs.

S&P Global Ratings expects the trailing 12-month default rate for speculative-grade companies to drop further from 3.3% to 2.5%; their bull market scenario could see that drop closer to 1.5%. Though there have been 13 defaults in Europe this year, that is a considerable improvement to the 42 credit events in 2020. Upgrades have outweighed downgrades. Stimulus has worked as a great big safety net. Take a bow, central banks and governments! Schumpeterians look away.

In the likely event interest rates tick up in the U.S. and U.K., European credit spreads would benefit. If economies continue to grow, corporate debt will look relatively better due to rising profits, compared to governments, with their ever-climbing debt burdens. Moreover, corporate issuance will naturally decline if yields rise and borrowing becomes more costly. The ECB is also committed to buying far less government debt next year for its asset purchase programs (this in turn reduces the somewhat overly-forced richness of government bonds).

Super-low interest rates have allowed companies to refinance their existing debt on the cheap — and many have jumped on the opportunity. But that window may be closing. It will take a substantial uplift in mergers and acquisition activity to see a fundamental uplift in corporate demand for new financing. On balance, 2022 should be more straightforward for credit investors after the whipsawing vagaries of the past two years.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2021 Bloomberg L.P.