Worst of Coronavirus Is Yet to Come for U.S. Factories

(Bloomberg Opinion) -- The worst of the coronavirus is yet to come for U.S. factories.

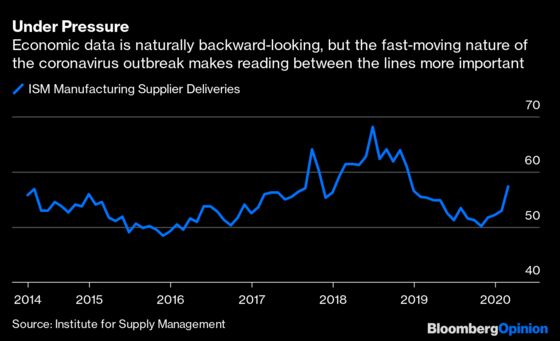

Data released Monday by the Institute for Supply Management showed manufacturing activity hovered just above the borderline between an expansion and contraction in February. No matter how you look at it, that’s a downshift from a January read that showed an uptick in production and new orders after a trade-war lull. But the on-the-ground dynamics for U.S. factories are more stressed than the headline number of 50.1 would seem to suggest. Notably, supplier delivery times stretched to the longest since 2018. While that’s typically a positive indicator showing parts makers are struggling to keep up with demand, in this case it shows the distortion already happening to supply chains as governments and companies pursue drastic measures to try to stem the spread of the Covid-19 respiratory illness that’s already killed more than 3,000 people.

Unlike retailers or airlines that feel the immediate hit of missed lattes and canceled flights, the supply-chain pain wrought by the coronavirus takes more time to manifest. Most companies operate with some kind of buffer in inventory and many likely pulled forward work to accommodate the Chinese Lunar New Year. There are positive signs that China is making progress bringing factories back on line as the spread of the coronavirus in that country slows. But the longer this public-health crisis drags on, and the more countries it ensnares, the harder it is to ensure parts can travel seamlessly through intricate, far-flung networks.

Notably, one ISM respondent was quoted as saying the coronavirus “is wreaking havoc on the electronics industry.” That is bad news for the likes of 3M Co. and DuPont de Nemours Inc., which supply materials and components to the sector. Neither company included an impact from the coronavirus in their initial 2020 outlooks, nor have they issued a formal update.

The growing – and more troubling – concern is that the supply-chain disruption is just the tip of the iceberg, and that the coronavirus could start to weigh heavily on underlying demand. Global manufacturing activity contracted in February by the most since 2009 amid a plunge in production and new export orders, according to the JPMorgan Global Manufacturing PMI. Aerospace is a particular watch item, with the International Air Transport Association forecasting the first decline in global passenger traffic since the financial crisis. Notably, that assumed that the worst of the airline capacity cuts was confined to China-linked markets; many carriers have since extended suspensions to Japan, South Korea and parts of Italy.

On Monday, Ryanair Holdings Plc cut its short-haul flight program to and from Italy by up to 25% for a three-week period amid weak demand. Fewer flights means that fewer planes need the lucrative spare part and maintenance work that’s been supporting aerospace supplier’s profits amid the grounding of Boeing Co.’s 737 Max. The prospect of monetary policy action and, in some cases, fiscal stimulus calmed markets on Monday and will soften the financial blow for companies grappling with disruption, but the Federal Reserve and European Central Bank can’t make people get on planes.

As with most things related to the coronavirus, this latest data point on manufacturing is a reminder of how much we still don’t know about the virus itself and the ultimate economic impact. But all signs point to more pain before the healing process begins.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2020 Bloomberg L.P.