Will the Fed’s Bond Buying Be as Powerful as the Idea?

(Bloomberg Opinion) -- Just about every investor has heard the adage “buy the rumor, sell the news.” Many have probably traded accordingly.

In the bond markets, it’s starting to look as if the strategy was to buy when the Federal Reserve revealed its plans to prop up companies’ debt, then pare back as the central bank prepares to take action.

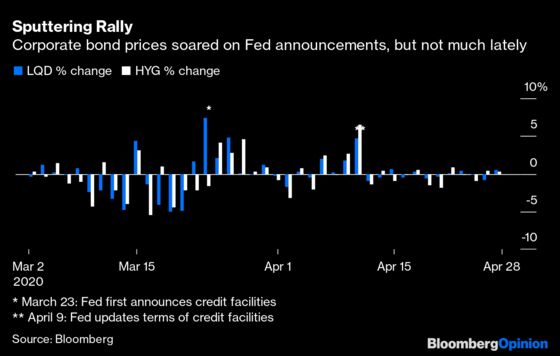

The corporate bond market reacted with nothing short of euphoria each time the Fed unveiled how it would go about backstopping debt from U.S. companies. The largest exchange-traded fund tracking the investment-grade market, known by its ticker LQD, surged 7.4% on March 23, the biggest gain in more than a decade. That was the day the Fed announced the terms in which it would wade into credit markets to an unprecedented degree. LQD popped an additional 4.7% on April 9, when the central bank expanded its program to include “fallen angels” and even junk-bond ETFs. The largest high-yield bond ETF (ticker: HYG) benefited the most, jumping by 6.6%, the most since January 2009.

Something strange has happened since then: Neither HYG nor LQD have climbed back to their April 9 levels.

Now, part of that can be explained by investors bidding up those ETFs to huge premiums relative to the underlying assets. But that can’t justify the moves of the past week, when prices were aligned with net asset values. While the S&P 500 Index has jumped 4.6% since April 21, LQD is down 0.1% and HYG is up just 0.6%. The same is true of the Bloomberg Barclays indexes tracking the investment-grade and high-yield debt markets.

The fading rally also can’t be blamed on a supply-demand imbalance. In the two weeks from April 9 to April 22, investment-grade funds experienced about $8 billion of inflows and high-yield funds added $9.9 billion, according to Refinitiv Lipper data. Even with more companies flocking to the now-open primary market with new offerings, investors have met them with a larger pile of cash. Average yield levels and spreads have barely budged for two weeks.

All of this suggests that the Fed simply announcing its corporate credit backstop was enough to swing open the market’s doors and get creditors and lenders back to the table. Or, to borrow words from a Bloomberg News headline this week, the central bank “is already bailing out levered companies.” But it raises questions about whether the facilities will meaningfully lift debt prices once they’re fully operational. In other words, it might be that the central bank’s thought counts just as much — if not more — than actually executing its plans.

Indeed, markets are just now discovering some of the more cumbersome and confusing aspects of the Fed’s programs. Bloomberg News’s Erik Schatzker and Craig Torres reported on Tuesday that the stimulus bill to combat the coronavirus pandemic included wording that was “deliberately vague” and “may leave out hundreds of companies with far-flung operations, including Coca-Cola Co., General Electric Co. and Mastercard Inc. No one knows for sure.”

Here’s a bit more:

The situation is creating headaches for Fed officials at a time when the central bank is playing a critical role preventing the Covid-19 outbreak from crushing the economy, people familiar with the matter said. In practical terms, restricting what it can and can’t do means the Fed might not be to supply all the liquidity needed to prop up prices if there’s another meltdown in credit markets.

...

Also hamstrung is BlackRock Inc., the investment firm retained to manage the corporate lending and bond-buying facilities. Fed officials and BlackRock executives are working out how to execute the program under the legislative constraints, the people said, declining to be identified because of the sensitivity of the issues.

Fed Chair Jerome Powell will have a chance to address some of these concerns at his press conference Wednesday after the central bank’s meeting. As of now, all that’s known is the credit facilities are supposed to “go live” in the next few weeks, per an April 17 speech from New York Fed Executive Vice President Daleep Singh.

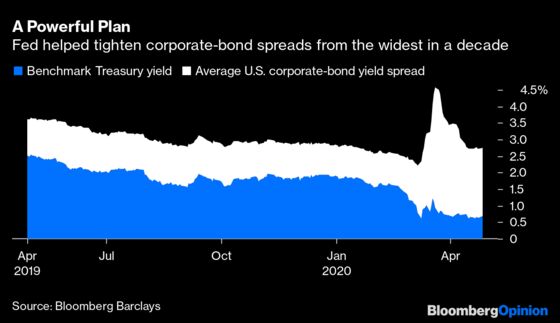

For now, here’s where markets stand: The average corporate bond yields 2.75%, or about 207 basis points more than benchmark Treasuries. On March 20, that yield was 4.58%, or 373 basis points more than Treasuries. Heading into this year, the average spread was less than half the current level, at 93 basis points. High-yield debt yields 774 basis points more than Treasuries, down from as high as 1,100 basis points last month but up from 315 basis points in January.

The question for bond investors is whether spreads will further compress as the Fed starts buying. In theory, of course, the answer is yes — a large, price-insensitive buyer is stepping in with up to $750 billion of firepower. But U.S. companies are staring down a crisis that’s unprecedented in any number of ways, and they are just beginning to look ahead to an economic reopening that could be equally as perilous. At best, it will be a slow grind tighter, not hundreds of basis points in less than three weeks.

Some money managers have already voiced their views. Jeffrey Gundlach, DoubleLine Capital’s Chief Investment Officer, this week called LQD “the most overvalued asset in the bond market.” The ETF reached as high as $132 on April 9, not far from its record level of $134.53 on March 6. It now stands at $129.20.

With so many questions about the path forward, it’s understandable why investors took comfort in knowing the Fed will support the debt markets as companies, governments and individuals muddle their way through in the coming months. But they should be wary of blindly following the central bank. The chance to do so may have already passed, before the Fed bought a single corporate bond.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.