Keep an Eye on Americans’ $3 Trillion Credit-Card Buffer

(Bloomberg Opinion) -- Since the Federal Reserve Bank of New York started its Quarterly Report on Household Debt and Credit in the wake of the 2008 financial crisis, it has largely showed the continued strength of the U.S. consumer. On the margin, there were some concerns about individuals falling seriously behind on paying back student loans, and debt overall surpassed its peak from a decade ago, but for the most part households have maintained a resilient financial position.

The New York Fed’s update for the first quarter, released Tuesday, will most likely be the last to follow that trend. The snapshot highlights why the Coronavirus Aid, Relief, and Economic Security Act was a crucial stopgap measure, but it also reveals cracks that will only grow bigger the longer America’s economy remains in lockdown.

The top-line news is largely positive. Even though household debt rose by $155 billion to a record $14.3 trillion, there was no noticeable increase in delinquencies in the first three months of 2020. Moreover, credit standards tightened slightly in the first three months of the year for new auto and mortgage borrowers, a signal that individuals with weak credit scores weren’t overextending themselves just before the pandemic hit.

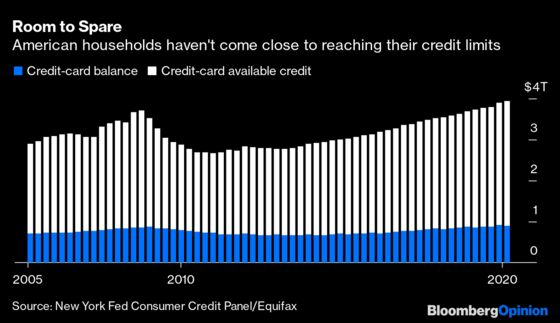

When an unprecedented amount of Americans are suddenly without jobs, trends in credit cards suddenly take on a more important role. Just as companies rushed to draw down revolving credit lines in March, individuals in theory could use more of their allowance, too. Interestingly, credit-card balances declined about $34 billion from the previous quarter to $893 billion, the sharpest drop since 2011, even though credit limits rose to a record $3.93 trillion. That has created a $3.04 trillion emergency buffer for individuals to get through the lockdown.

In the wake of the 2008 crisis, those limits proceeded to fall for nine consecutive quarters. For now, though, “open revolving credit lines may provide critical borrowing opportunities to consumers to smooth gaps in income,” New York Fed researchers wrote in a blog post analyzing the data. They note that in lower-income ZIP codes, the median available credit is about $1,900, with 25% of borrowers having at most $150 to draw upon. By contrast, in areas with the highest incomes, the median card holder can tap almost $14,000 of funds.

As I wrote last month, large Wall Street banks are angling to be the good guys in the coronavirus crisis. Bank of America Corp., for one, made sure to emphasize that individuals and families can request to defer payments on credit cards, auto loans and mortgages without any negative credit-bureau reporting for those who were previously up to date. While credit-card delinquencies have been ticking higher in recent years, they’re still well below levels seen from 2003 to 2007. And even though mortgages make up the vast majority of household debt, delinquencies remain near all-time lows. By and large, it appears individuals have been on-time with these payments, which in turn should earn goodwill with their financial institutions.

Of course, it’s not just the banks offering a lifeline through the lockdown. The CARES Act included forbearances for both mortgage and student-loan payments. The latter, while a smaller component of household balance sheets, is arguably just as crucial because a greater share of student loans were already delinquent by 90 days or more than any other type of debt. Student loans also fall disproportionately on younger Americans who might have been more likely to lose their jobs during the first wave of layoffs.

New York Fed researchers note that a majority of Americans (55%) younger than 65 don’t have either mortgage debt or student loans. “Thus, while these policies certainly provide substantial benefits to mortgage and student loan borrowers, they do not benefit all consumers,” they wrote. Still, “a substantial proportion of indebted households and individuals will potentially be able to benefit from a payment moratorium provided by the CARES Act.”

As those two statements show, it’s impossible to draw firm conclusions from a 30,000-foot snapshot of Americans’ balance sheets. Without question, those households in a more tenuous financial position as of March 31 will start to feel financial strains sooner, if they haven’t already.

In that sense, the report reinforces the high stakes of shutting down the world’s largest economy and the importance of critically evaluating the trade-offs between remaining closed to curb the burden on health-care systems and moving toward reopening. As the credit-card data suggest, there’s a cushion for many individuals to get through weeks — and possibly even months — without bringing in their previous income. The $1,200 stimulus checks and enhanced federal unemployment benefits might also help bridge such shortfalls. Beyond a few months, though, the finances of many Americans will inevitably become dicey.

The last look at the pre-coronavirus state of U.S. households revealed at least some reasons to be optimistic. The next update will reflect the consequences of every step taken, either in the right or wrong direction, by local, state and national leaders to address this crisis.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.