(Bloomberg Opinion) -- President Donald Trump inherited the world's best economy in 2017 and helped make it one of the worst. The coronavirus pandemic would have made Americans miserable under any president, but it was Trump’s defiance of science, muddled messaging and incessant vitriol that has plunged the country into a swamp of joblessness, receding labor participation and slumping business confidence unseen in other developed nations. Trump's four years in office already measure up as the biggest economic disaster for any U.S. president in modern times, according to data compiled by Bloomberg.

It didn't have to be this grim. Dozens of nations dealing with the same challenges are showing superior infection, death and unemployment rates and quicker business rebounds after shutdowns earlier this year. But Trump's disdain for antibody tests, contact tracing, social distancing and masks, among other prerequisites for containing the coronavirus, enabled the U.S. to lead the world in confirmed cases and deaths (though not in deaths per capita). Instead of peaking in late April with more than 30,000 daily new U.S. Covid-19 infections, the virus is resurgent in July — a stark contrast to such densely populated regions as Hong Kong, where Covid-19 retreated to insignificance within a month of its March high.

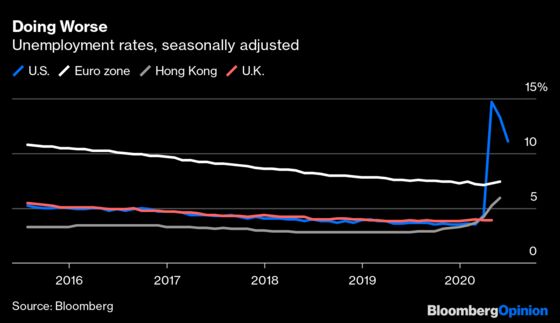

The dreadful consequence is that America doesn't work anymore. The 14.7% April unemployment rate was the highest since 1948, when Harry Truman was president, according to data compiled by Bloomberg. Trump cheered when the Labor Department reported a decline to 11.1% for June. He didn't mention that U.S. joblessness had continued to dwarf the 3.9% rate in the U.K., which lowered its daily infections in two months after experiencing the most Covid-19 deaths in Europe. France, Italy and Spain were similarly victimized by Covid-19, yet their unemployment is about half the percentage of Americans out of work, according to data compiled by Bloomberg.

Unlike France and Germany, which dealt with the coronivirus systematically to pave the way for a robust rebound, the U.S. is less likely to achieve a dramatic recovery after losing more than 20 million jobs in April while the labor participation rate plummeted 2.5% — a downturn unprecedented since record-keeping began during Truman's first term, according to data compiled by Bloomberg. The trauma of such dislocations hasn’t showed up in opinion polls showing that voters retain modest confidence in Trump’s economic stewardship. But it is starkly reflected in the Bloomberg Consumer Comfort Index, which tumbled 16.8 percentage points in April, the most since data was compiled in 1985 when President Ronald Reagan was in his second term.

In the stock market, where the S&P 500 has recovered its March decline, investor confidence still is precarious as measured by VIX Index. The closely-watched gauge of investor uncertainty surged to a record 82.7 in March, surpassing the November 2008 level of 80.9 during the financial crisis, according to data compiled by Bloomberg.

Trump had a chance to slow Covid-19 by following Hong Kong's example and insisting that all Americans wear masks. “The only thing you can do is universal masking, that's what stopped it,” said Professor Yuen Kwok-Yung, a leading coronavirus expert advising the Hong Kong government, in an essay in the Wall Street Journal. Before Texas reported a record 194,932 of Covid-19 cases this month, the mayors of Austin and San Antonio said the same thing: If Trump wore a mask, lives would be saved and the economic outlook would be brighter.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Matthew Winkler, Editor-in-Chief Emeritus of Bloomberg News, writes about markets.

©2020 Bloomberg L.P.