(Bloomberg Opinion) -- Christine Lagarde made her third prime-time appearance as president of the European Central Bank on Thursday, against a backdrop of plunging stock markets around the world and surging bond yields for the euro zone’s weaker economies. If her aim was to soothe investor concern about the repercussions of the pandemic, she failed — spectacularly.

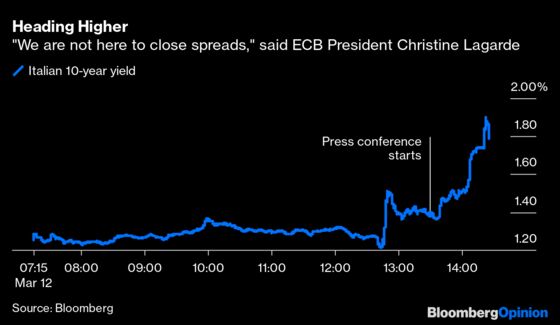

At the start of Thursday’s press conference, Italy’s 10-year borrowing cost was about 1.4 percent. By the time it wrapped up a bit less than an hour later, the interest rate had surpassed 1.8 percent, a climb of more than 60 basis points for the day.

The proximate cause of that surge was a phrase that may come to haunt Lagarde. “We are not here to close spreads,” she said, in response to a question about the negative market reaction to the measures her central bank had announced earlier. “There are other tools and other actors to deal with these issues.”

Except there aren’t other actors, at least not as far as the bond market vigilantes are concerned. The rise in Italian yields as the country went into lockdown mode, guaranteeing a recession as commerce grinds to a halt, was modest in recent days precisely because bondholders expected the ECB to stand ready to curtail any increase in borrowing costs. Its role as lender of last resort was seen as a given; Lagarde destroyed those hopes with a single sentence.

Other bond markets also suffered. Greek yields climbed by half a percentage point to their highest level since August, with Spanish and Portuguese 10-year borrowing costs also climbing. Even French bonds took a beating.

That three-part package comprises access to more cheap loans for banks, long-term financing targeted at maintaining access to credit for the region’s small- and medium-sized enterprises, and boosting the ECB’s existing bond-buying program by an additional 120 billion euros ($134 billion). Missing from the action plan was a cut in interest rates — something the Federal Reserve and the Bank of England both delivered earlier this month at emergency meetings in response to the coronavirus crisis.

Lagarde was keen to stress that the ECB hasn’t reached the lower boundary for interest rates (which would imply that the only future direction would therefore be for higher rates) and that her institution has plenty of wiggle room on borrowing costs. No one in the market is buying that message. The lack of a rate cut shouts loudest, and the fact that today’s decision was unanimously agreed on is not being perceived as a sign of strength. More likely is that the ECB’s more hawkish representatives, led by Germany, put their foot down, and Lagarde is not yet secure enough to challenge dissent.

So the ECB has drifted from the simplicity of Mario Draghi’s "whatever it takes" message to a complicated package of confusion. The markets needed something simple to latch on to. Lagarde has failed to deliver. The costs, both to the ECB’s credibility and to Italy’s ability to fund the cost of combating the effects of the virus, could prove expensive.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2020 Bloomberg L.P.