Stock Prices Make Lofty Promises That Earnings Can’t Keep

(Bloomberg Opinion) -- If investors disliked the level of the U.S. stock market last week, they must loathe it now. The market surged on Monday to its highest level since early March, shrugging off complaints by some prominent money managers that it was already too expensive.

David Tepper told CNBC last week that stocks are more overvalued than he’s ever seen except at the peak of the dot-com bubble in late 1999 and early 2000. Stanley Druckenmiller told the Economic Club of New York that “the risk-reward for equity is maybe as bad as I've seen it in my career.”

Some are letting their trades do the talking. Warren Buffett confessed at Berkshire Hathaway Inc.’s annual meeting earlier this month that he sold the company’s considerable stake in airlines. A regulatory filing last week also revealed that Buffett dumped some of Berkshire’s auto and banking stocks, including 84% of its stake in Goldman Sachs Group Inc.

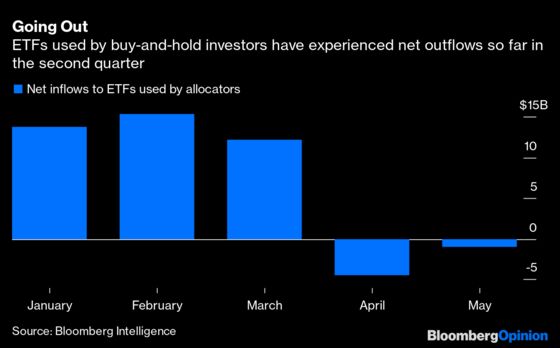

Even some less notable investors have turned bearish. A basket of exchange-traded funds favored by asset allocators (as opposed to traders) for exposure to stocks and high-yield bonds took in a net $12.2 billion in March, according to numbers compiled by Bloomberg Intelligence, despite the month’s deep sell-off across stock and bond markets. Since April, however, allocators have pulled roughly $5 billion from that same basket of ETFs.

So what accounts for all the skepticism? The answer lurks in just-wrapped earnings results for the first quarter. The price-to-earnings ratio is the most closely watched measure of the stock market’s valuation. But before the first-quarter results became available, no one had any inkling to what extent the shutdown would impair earnings. That was apparent in Wall Street analysts’ earnings estimates. As late as the end of March, the consensus still called for earnings growth from the S&P 500 this year, according to numbers compiled by Bloomberg.

First-quarter earnings crushed any such hope. One-quarter operating earnings per share for the S&P 500, which generally exclude income and expense that fall outside companies’ core businesses, tumbled 49% in the first quarter from the fourth quarter of 2019, according to S&P’s estimate with roughly 90% of companies reporting. That sobered up analysts. The most recent consensus calls for S&P 500 earnings per share of $126 for 2020, a decline of 17% from last year.

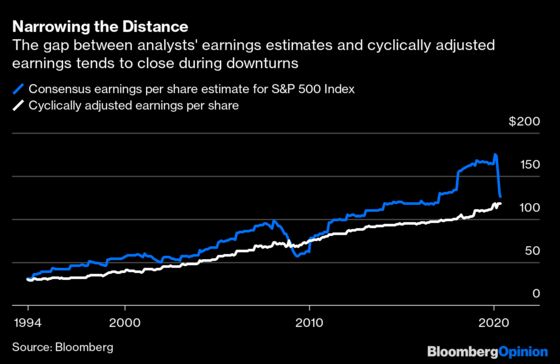

That may still sound too optimistic, but it’s probably not far off. A popular variation of the P/E ratio is the CAPE, or cyclically adjusted P/E. The cyclical adjustment refers to the use of 10-year trailing average earnings, adjusted for inflation, rather than analysts’ consensus estimate of future earnings. The consensus is almost always higher because the cyclical adjustment keeps a lid on earnings by incorporating previous years. During downturns, however, the difference between the two begins to narrow as analysts write down their estimates. And as the two earnings numbers approach each other, it’s often a sign that the consensus is nearing the mark.

At the peak of the dot-com era in early 2000, for example, analysts’ consensus estimate called for S&P 500 earnings of $58 a share, which was roughly 50% higher than cyclically adjusted earnings. By the end of 2001, the consensus had shrunk to $50 a share, or just 16% higher than cyclically adjusted earnings. Profits bottomed at $42 a share several months later. A similar pattern emerged during the 2008 financial crisis.

Where are we now? When 2020 began, analysts’ consensus estimate called for earnings of $175 a share for the S&P 500, which was roughly 50% higher than cyclically adjusted earnings. The most recent consensus of $126 is now only 7% higher than cyclically adjusted earnings. With a more realistic earnings estimate in hand, there should be less disagreement about the market’s valuation.

And that’s what troubles Tepper and his fellow notables. The S&P 500 currently trades at a P/E ratio of 23 based on analysts’ consensus earnings for 2020. That’s the highest P/E ratio using analysts’ estimates on record, except for the peak of the dot-com bubble, and well above the P/E ratio of 17 just before the financial crisis in late 2007. And given that cyclically adjusted earnings are in the ballpark, the CAPE ratio is only modestly higher at 24 times.

Of course, earnings could tumble further from here, which would make the market even more expensive. Investors appear to be betting on the opposite outcome, that earnings will hold up better than expected, thereby justifying the market’s lofty level, or even higher prices. The market seemed to validate that view on Monday.

None of this is news to Tepper, Druckenmiller or Buffett, who ordinarily delight in scooping up stocks during a crisis. If they find this market unappealing, perhaps investors would be wise to take a closer look at the numbers.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nir Kaissar is a Bloomberg Opinion columnist covering the markets. He is the founder of Unison Advisors, an asset management firm. He has worked as a lawyer at Sullivan & Cromwell and a consultant at Ernst & Young.

©2020 Bloomberg L.P.