Steven Mnuchin Is a Rock Star to Japanese Investors

(Bloomberg Opinion) -- U.S. Treasury Secretary Steven Mnuchin most likely won a lot of fans among Japanese bond buyers this week.

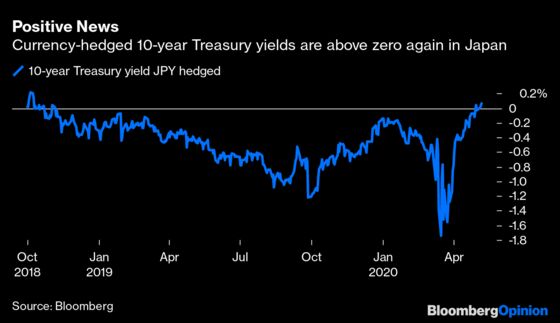

His department’s announcement on Wednesday that it would increase issuance of longer-term debt to cover America’s swelling budget deficits surprised stateside bond traders, leading them to sell 10-year and 30-year Treasuries. The repricing was enough to push the currency-hedged yield on 10-year U.S. notes to 0.07% for Japanese investors. While that doesn’t sound like much, it’s the most positive since October 2018, when the Federal Reserve was still raising interest rates, and beats domestic Japanese yields of zero.

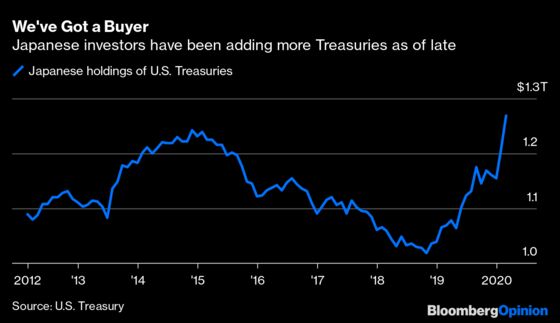

Already, Japanese investors were plowing into Treasuries, adding more than $110 billion in the first two months of 2020 to bring their holdings to a record $1.27 trillion. The now-positive hedged 10-year yield, however small, suggests a steady source of demand as the U.S. begins to auction off record amounts of debt. Large institutions with conservative mandates tend to hedge foreign-exchange risk if possible when they invest in overseas obligations because currency swings can overwhelm any moves in interest rates.

If October 2018 sounds familiar, that’s because it marked the peak in nominal 10-year Treasury yields during the Fed’s last tightening cycle, at 3.26%. Obviously, the yield is nowhere near that now, at 0.66%. The reason Japanese investors are getting the same return is because of the sharp drop in hedging costs, which in the classic cross-currency trade reflects moves in the U.S. London Interbank Offered Rate, which has declined for 15 consecutive days, and what’s known as the basis for yen-based investors.

To hedge currency risk, Japanese investors lend yen and borrow dollars, typically over a short period and then roll over the hedges. This means they pay three-month dollar Libor and the basis, while also effectively paying their local Libor because it’s slightly negative. In absolute value terms, those rates are now 0.43%, 0.15% and 0.02%, respectively. By contrast, when 10-year Treasury yields peaked on October 9, 2018, three-month dollar Libor was 2.42%, the basis was 0.5% and local Libor was 0.08%.

In practice, some money managers simply use forward currency contracts rather than run through the entire cross-currency trade. For years, when the Fed was raising short-term interest rates, one of the easiest money-making trades was for U.S.-based investors like Pacific Investment Management Co. to buy Japanese bills and hedge the currency risk, which turned the negative-yielding debt into a solid, if unspectacular, foundation for a portfolio.

The Fed is now back at the zero lower bound, and some traders on Thursday wagered that Chair Jerome Powell and his colleagues will follow the Bank of Japan into negative interest rates. The prices of early 2021 fed funds futures contracts rose above the 100 level, which implies negative yields attached to the policy rate. That move, perhaps inspired by DoubleLine Capital Chief Investment Officer Jeffrey Gundlach saying on Twitter that “the pressure to go negative on Fed Funds will build as short term borrowing explodes and dominates,” sent yields across the Treasury curve tumbling.

Still, as long as currency-adjusted Treasury yields are positive, Japanese investors should be a steady source of demand to offset increased auction supply. Of course, there are other fixed-income options. According to a May 1 report from Tetsuo Ishihara, a U.S. macro strategist at Mizuho Securities USA, several large Japanese life insurers have said they like U.S. investment-grade bonds, where spreads still remain wider to Treasuries than at any point from mid-2016 through 2019. At the same time, regulators in Japan have expressed financial-stability concerns about exposure to foreign credit products, making Treasuries an appealing alternative.

Regardless, Japanese investors suddenly have many positive-yielding options. It’s anyone’s guess how long that’ll last in Treasuries, as evidenced by Thursday’s trading. But for the moment at least, Mnuchin’s decision to go long was a winning play in Japan.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.