(Bloomberg Opinion) -- The European Central Bank’s meeting on April 30 might be its most important as it tries to manage the devastating economic impact of the Covid-19 virus. While its reaction so far has worked, it will need much greater firepower in the future. It will also have to be much more flexible in how it applies its rules on asset purchases.

The biggest immediate question, as revealed by my Bloomberg News colleagues, was whether the central bank should relax its eligibility criteria to accept sub-investment grade debt as collateral in its funding facilities. That was answered on Wednesday night, when the ECB said it would accept junk bonds as long as they were rated at least BBB- as of April 7.

It said it may decide on further measures, if needed. The ECB might well follow the U.S. Federal Reserve’s example and start buying high-yield bonds in its pandemic Quantitative Easing programs too. As I’ve argued before, it makes sense to show a little love to some of the higher-quality junk-rated companies. They employ plenty of people too.

This is the time for the ECB to get out of its own way and not allow the coming wave of credit-rating downgrades for European government and corporate debt to blunt its stimulus response. Should Christine Lagarde’s institution really be barred from buying the bonds of companies and nations that have only fallen slightly below investment grade because of the pandemic?

This might also be the right moment to increase the pandemic QE package. Analysts at ABN Amro Bank NV reckon it could be raised without much difficulty by 500 billion euros ($544 billion) to 1.25 trillion euros.

While the European Union’s political leaders haggle over their fiscal package at a meeting on Thursday, the real heavy lifting will have to be done by the ECB, as usual. The central bank signaled on April 7 that a loosening on junk-rated debt might be coming when it said it would “assess further measures to temporarily mitigate the effect on counterparties’ collateral availability from rating downgrades.” Wednesday’s decision allows for a comprehensive plan to be unveiled at the ECB’s Governing Council meeting next week.

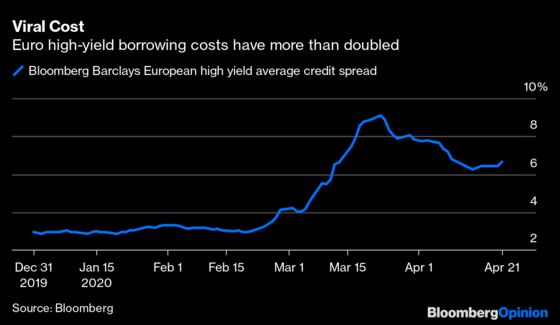

The situation is urgent. S&P Global Ratings is set to review Italy’s BBB (negative outlook) rating on Friday. The expected one-notch downgrade would still leave Rome on just the right side of the investment grade boundary, but it would push the debt of many other Italian issuers — effectively tied to their country’s rating — into junk. That would create liquidity constraints in the Italian banking system if a raft of bank and corporate debt became ineligible for use as collateral with the ECB.

This is far from being an Italian-only problem. Bloomberg Intelligence points out there is more than 200 billion euros of European corporate debt that’s close to entering the “fallen angel” category. There’s little the ECB can do to prevent the downgrades but it can soften the impact.

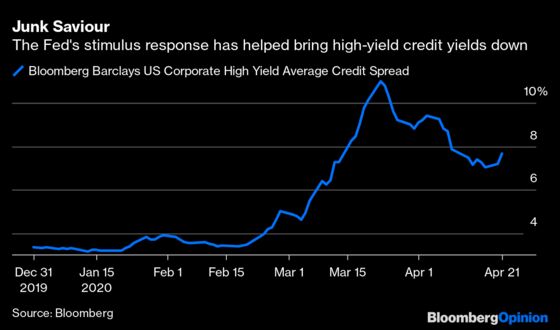

As the ECB already accepts as collateral Greek government debt, which is several notches below investment grade, the Rubicon had already been crossed. The central bank is also buying Greek sovereign bonds so why not match the Fed’s response by acquiring corporate bonds recently downgraded to junk? The Fed’s move tightened U.S. spreads on BB-rated debt by more than 300 basis points. A similar ECB approach would help lower corporate borrowing costs across Europe too. That’s a noble aim.

As with the Fed, it’s a worrying thing for the ECB to be holding ever more risky credit. But these are truly dangerous times for the economy. We’ll just have to fall back on the hope that these are temporary measures until the world recovers.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2020 Bloomberg L.P.