(Bloomberg Opinion) -- The federal government is moving at a breakneck pace to respond to the coronavirus recession. In the states, however, the preliminary data suggests staggering job losses, exceeding economists’ expectations of just a week ago. If the pattern holds, it will mark the sharpest downturn in the labor market on record.

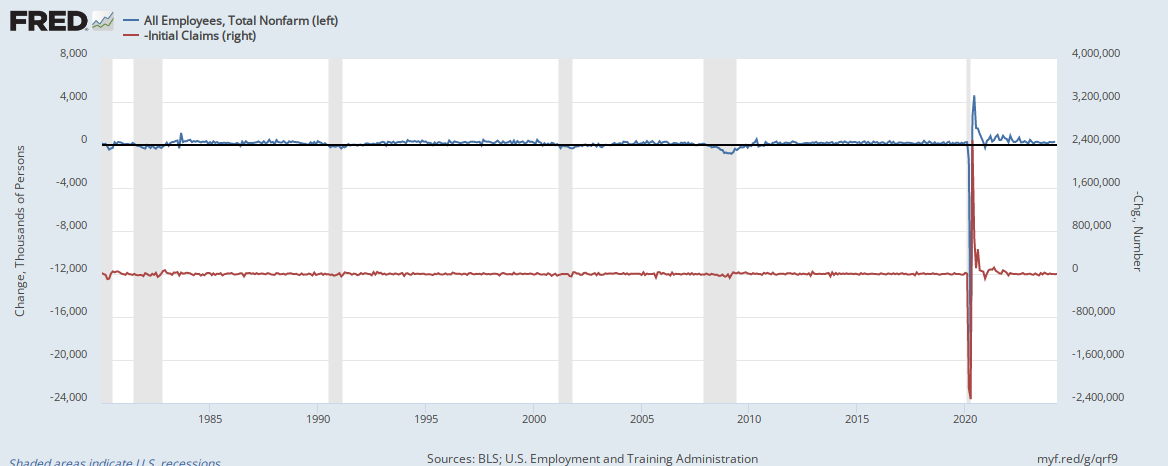

A spike in initial claims for unemployment insurance is among the earliest signs that a recession is underway. The most recent official number is from the first week of March, and it shows 221,000 claims, roughly on par with the average of the last several months.

State unemployment offices, however, are reporting huge increases in the volume of more recent claims. Hawaii reported 1,500 claims on Monday, five times the previous Monday. From Friday to Tuesday, Connecticut saw 30,000 claims, about 10 times the average for a whole week. Pennsylvania received a staggering 50,000 claims on Monday alone, compared to 12,000 claims for the first week of March.

All of this implies that, for the U.S. as whole, total initial claims for unemployment insurance for this week could spike to over 2 million. During the worst week of the Great Recession, the last week of March 2009, claims reached 665,000.

Some perspective: Even when the economy is booming, hundreds of thousands of workers file for unemployment benefits each week, and an even greater number find new jobs. In December 2007, by way of comparison, the U.S. economy added 108,000 jobs. In March 2009, it lost 800,000.

The correlation between unemployment insurance claims and the monthly payroll report is not exact. But simple extrapolation suggests that next month’s payroll report could show a total decline of roughly 4 million jobs. The human suffering behind that number is overwhelming. It all but requires Congress to pass without delay an increase the amount workers receive in unemployment insurance.

{kind=link}

The macroeconomic consequences are if anything more dire. A typical recession gains steam because all workers reduce their spending: Some because they’ve lost their jobs, others because they expect to, others who are worried they might. This effect ripples through the economy.

The first month of major job losses during the Great Recession was February 2008, when the economy shed 906,000 jobs. The effect rippled throughout 2009, and during the entirety of the Great Recession about 8.5 million jobs were lost. A similar multiplier would place total job losses from the current recession at … 37 million.

Again, using back-of-the-envelope math, that implies a rise in the unemployment rate to about 27% — even higher than the 20% Treasury Secretary Steven Mnuchin has warned as possible. It would exceed the highest unemployment on record, 24.9%, set during the Great Depression. To repeat: These are rough estimates based on early data.

Moreover, the coronavirus recession is, structurally speaking, unlike any that have come before it. Many of the measures the public is being asked to take are voluntary, so it is possible that economy could bounce back rapidly once they are lifted. On the other hand, because social distancing will have to continue for months, it could be that the initial shock is compounded several times over.

In either case, the government and the public should be prepared for a dramatic and uncertain economy.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Karl W. Smith, a former assistant professor of economics at the University of North Carolina and founder of the blog Modeled Behavior, is vice president for federal policy at the Tax Foundation.

©2020 Bloomberg L.P.