(Bloomberg Opinion) -- At one point last week, traders who bought high-yield energy bonds during the darkest days of the market’s sell-off had to be nothing short of giddy at their good fortune. In just three weeks, from March 24 to April 14, an index of junk debt from companies in oil field services, midstream and refining had surged more than 30% — a staggering rally that if stretched out over a year would translate to a 10,500% windfall.

Markets rarely move in a straight line, of course, and indeed the gains flatlined toward the end of the week. Still, those investors who snapped up speculative-grade energy bonds at 24% yields were sitting on a tidy profit in the short term and amassed a seemingly large buffer for losses in the longer run. As of Friday, the average yield on the Bloomberg Barclays High Yield Energy Total Return Index tumbled almost 900 basis points from that peak to about 15%.

Those yield hunters might want to book their gains and run, judging by the latest swings in the oil markets.

West Texas Intermediate crude oil fell more than 40% on Monday to less than $11 a barrel, the biggest one-day drop since the contract began trading in 1983 and the lowest level since 1986. The WTI contract for May expires Tuesday and is more than $10 a barrel cheaper than the one for June, wider than the record $8.49 difference set in December 2008. A a fast-growing glut of oil is causing traders to shift their positions rapidly to June so they don’t have to take deliveries of cargoes given the lack of space to store them. As Bloomberg News’s Alex Longley put it, there are signs of weakness everywhere:

Buyers in Texas are offering as little as $2 a barrel for some oil streams, raising the possibility that producers may soon have to pay to have crude taken off their hands. China reported its first economic contraction in decades on Friday, an indication of what’s to come in other major economies that have yet to emerge from coronavirus-driven lockdowns.

“There is no limit to the downside to prices when inventories and pipelines are full,” commodities hedge fund manager Pierre Andurand said on Twitter. “Negative prices are possible.”

Already, those who tried to call the oil-price bottom through energy exchange-traded funds are getting burned. As Bloomberg’s Katherine Greifeld noted, the United States Oil Fund LP (ticker: USO) plunged more than 10% on Monday, burning investors who added a whopping $1.6 billion into the $4.3 billion fund last week — the biggest weekly inflow ever.

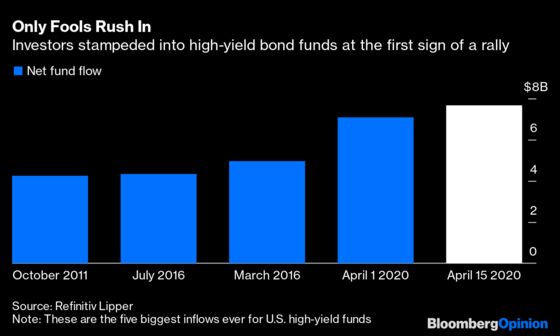

Guess what other asset class just experienced record demand? That would be U.S. junk-bond funds, which reported an unprecedented $7.66 billion inflow for the week ended April 15, according to Refinitiv Lipper data. It broke the previous high-water mark of $7.09 billion set in the period through April 1.

Now, the sudden revival in high-yield debt goes beyond just the energy sector. Most prominently, the Federal Reserve announced on April 9 that its corporate-bond facilities would extend purchases to “fallen angels” that recently lost their investment grades, alleviating some fears that the speculative-grade ranks would be inundated with supply. That helped thaw the primary market for junk-rated companies to raise cash and avert an imminent reckoning.

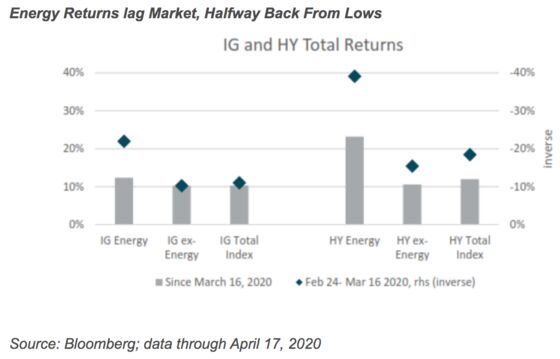

Still, there’s evidence that junk energy bonds, which faced the steepest sell-off and therefore offered the highest yields, benefited disproportionately from the overall bounce-back in risky debt. Here’s a chart from John Velis, an FX and macro strategist at BNY Mellon:

The blue diamonds show the depth of losses from Feb. 24 through March 16 and the gray bars show the total return since that date. Clearly, high-yield energy bonds were pummeled more than the rest of the market and remain the worst-performing segment, but they’ve bounced back significantly from their lows, too. “We wonder if the HY energy sector is too sanguine about stability and subsequent recovery prospects in high-yield energy bonds,” Velis wrote in a note Monday.

He’s hardly alone. Morgan Stanley strategists Brian Gibbons and Mackenzie Schneider wrote Monday that they “continue to see low asset values and recovery rates across the sector at the current commodity strip.” The most optimistic point was that “companies with strong liquidity and longer maturity runways have a greater chance of making it through the downturn to a higher price environment, although pricing that optionality is challenging.” To their point, double-B rated energy bonds gained the most last week, while those rated triple-C dipped even lower to roughly 20 cents on the dollar.

Bank of America Corp. strategists went even further, arguing that high-yield bond spreads as a whole don’t fully reflect default risk. They expect a 21% cumulative junk-debt default rate over the full cycle, from 11% for double-Bs to 50% in triple-Cs, and a 9% rate over the next 12 months. By their calculation, that suggests yields should be 950 basis points more than Treasuries to compensate for the risk, rather than the current 705-basis-point spread.

Similarly, the latest lurch lower in oil prices suggests the peak yield of 24% for high-yield energy bonds might have been closer to the appropriate level after all. The cost to insure against defaults from Diamond Offshore Drilling, Transocean and Chesapeake Energy over the next five years surged on Monday by more than just about all other companies in Markit’s high-yield credit-default swap index. That’ll soon make its way into bond pricing.

It’s worth remembering that sometimes bonds look cheap for a reason. As my Bloomberg Opinion colleague Liam Denning put it in his assessment about the future of the energy industry, “Covid-19 is like a fever dream of all the pressures that were bearing down on oil already.”

Fortunately for traders who went bottom-fishing for speculative-grade energy bonds in the eye of a market storm, they still have time to wake up to reality before their blockbuster returns are swiftly washed away.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.