Markets Are in Crisis, Not the Financial System

(Bloomberg Opinion) -- Financial-market volatility is painful. From mom-and-pop investors suddenly seeing red in their 401(k) plans to large institutions scrambling to hedge their gigantic portfolios, this past week has been record-setting in any number of ways. The one example that’s bound to be repeated often: The S&P 500 Index plunged the most since 2008.

Minds tend to wander in the same direction when hearing that particular year. So let me just say this right now: There’s virtually no evidence that the world is veering toward another financial crisis. The rapid decline in Treasury yields and the fastest correction ever in stocks is, at least as of now, purely a market-driven phenomenon. That’s bound to strain some mutual funds, no question. Maybe some hedge funds, too. But it’s hardly apocalyptic.

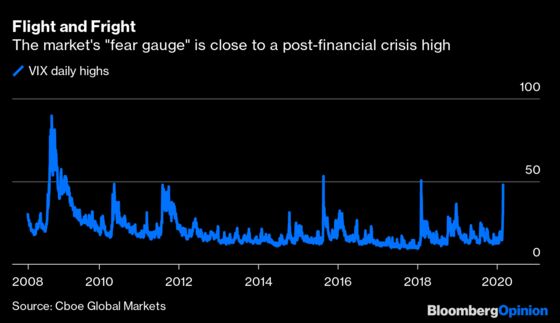

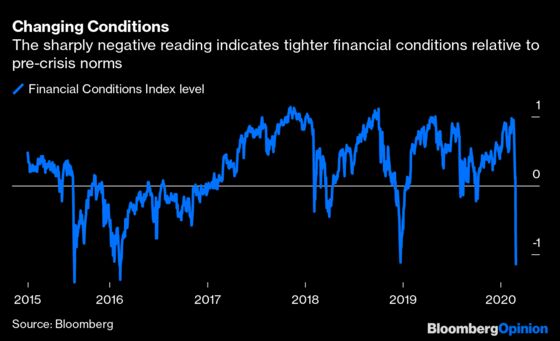

Here are just a couple of examples of scary charts that truly don’t reflect anything about the health of the financial system; rather, they are just another way of measuring the quick sell-off in equity markets.

First there’s the often-cited market “fear gauge,” the CBOE Volatility Index (VIX). It jumped to as high as 49.48 on Friday, the highest level since the so-called Volmageddon episode in early 2018.

Then there’s the fact that the Bloomberg U.S. Financial Conditions Index has been absolutely crushed in recent days and reached its lowest level since early 2016. But the inputs to this index are largely market-based, like the levels of the S&P 500 and the VIX, as well as yield spreads between Treasuries and corporate bonds rated triple-B and below investment grade, which have both widened significantly.

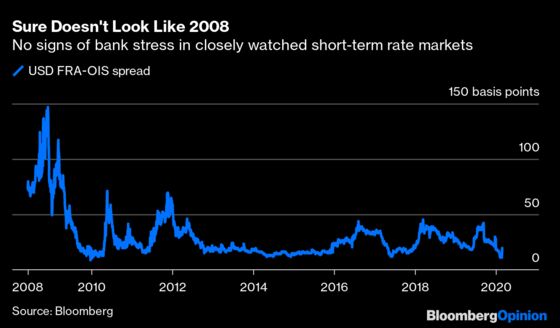

So what sorts of metrics are worth watching to determine whether a banking crisis is unfolding beneath the market chaos? Some traders look to the London interbank offered rate and other money-market benchmarks.

There, the three-month Libor plunged 11.8 basis points on Friday to 1.46275%, the steepest one-day drop since December 2008. This isn’t what you would expect to see if financial institutions were facing any sort of turmoil, given that it’s the rate at which large global banks lend to one another. The drop merely reflects expectations of significant central-bank easing in the near future. A spread known as FRA/OIS, which measures market expectations for the gap between Libor and the Overnight Index Swap Rate, are rising a bit but still remain comfortably below levels seen in each of the past two years and certainly nowhere near the levels of the crisis.

Then, of course, there’s the Federal Reserve. There’s a lot of frustration that policy makers haven’t yet indicated that interest-rate cuts are imminent. “I wouldn’t want to prejudge the March meeting,” St. Louis Fed President James Bullard said on Friday, mimicking comments earlier this week from other policy makers. “We are going to want to monitor events right up until the meeting.” This could be contributing to the market’s angst.

Fed Chair Jerome Powell attempted to quell that concern with a somewhat rare statement on Friday afternoon: “The fundamentals of the U.S. economy remain strong. However, the coronavirus poses evolving risks to economic activity. The Federal Reserve is closely monitoring developments and their implications for the economic outlook. We will use our tools and act as appropriate to support the economy.” Those 44 words didn’t have much immediate impact.

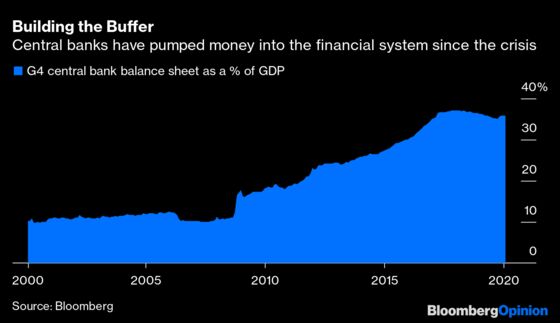

Still, few can dispute that the central bank has made significant strides to insulate the banking system from market stress. The Fed’s balance sheet expanded rapidly in the final months of 2019, which, somewhat ironically, had been cited by some investors as the reason behind the surge in equity prices. Stocks may be tumbling, but reserves at the Fed sure aren’t: They reached $4.18 trillion earlier this month, up from $3.76 trillion at the end of August.

Expanding out to include the European Central Bank, the Bank of Japan and the Bank of England, their balance sheets as a percentage of gross domestic product remains close to a record. It’s an open question whether that’s a good thing for the health of their respective economies, but it makes it easier for the banking sector to withstand a severe slowdown.

That’s not to say financial system is impenetrable. September’s repo meltdown served as a stark reminder of what can happen when critical market plumbing stops working. The Fed was able to step in, though, and it’s mostly functioning normally now.

There’s still room for improvement. That’s why it was such a big deal this week that JPMorgan Chase & Co. said it plans to borrow funds through the Fed’s emergency lending facility from time to time this year in an exercise designed to break the stigma attached to it. The discount window is intended to provide emergency liquidity to banks that otherwise have healthy balance sheets. Randal Quarles, the Fed’s vice chairman for banking supervision, has said better access to the window would reduce demand for excess reserves at the Fed which in turn would enhance liquidity in repo and other money markets.

I have written before about how the financial crisis caused a fundamental shift in who shoulders market risk now. Instead of Wall Street banks holding troves of corporate bonds and other risky assets, and stepping in when the markets are chaotic, they’ve tended to reduce their inventories over the past decade. That means asset managers, which are far less essential to the underpinnings of the global economy, will be increasingly on their own when losses start to mount. That’s a healthy development.

As Bloomberg News’s Sebastian Boyd put it, in 2008 “reasonable minds could wonder out loud whether we were watching the death throes of global capitalism.” You wouldn’t be rational saying that today. Investors are witnessing the outbreak of a virus that governments around the globe are struggling to contain, which in turn has caused pockets of the global economy to grind to a standstill. Germany is quarantining 1,000 people. Switzerland is banning large events, including the Geneva car show. Milan looked like a ghost town. In such an environment, is it any wonder that the share prices of global companies have repriced, or that sovereign debt markets are bracing for a severe hit to growth?

The coronavirus has infected markets, the economy and the habits of people worldwide. But if it’s any consolation, the financial system is proving so far to be immune.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.