(Bloomberg Opinion) -- Two and a half years ago, Giuseppe Conte was an obscure lawyer and academic unknown to most Italians. Next week, this very unlikely prime minister will lead Italy’s most important round of European negotiations in nearly a decade.

The European Union’s political leaders will meet on April 23 to agree on a coordinated economic response to the Covid-19 pandemic, which has killed more than 65,000 people across the bloc. Italy’s economy is set to shrink by 9.1% this year, according to the International Monetary Fund. After a promising start, the government is struggling to put together a timely response because of administrative failures and concerns over the country’s very high debt levels.

Conte has demanded that the euro zone sets up joint and several liabilities (“euro bonds”) to show solidarity with its financially weaker members, but countries including Germany and the Netherlands are unlikely to give way on this. The single-currency area’s finance ministers reached an agreement last week for a coronavirus rescue package, but it only included the lightest reference to possible discussions over a limited form of euro bonds — or coronabonds, as they’re otherwise known.

The prime minister will hope to press the case of coronabonds afresh at the EU meeting. In reality, he may have to choose whether to climb down from this unrealistic negotiating strategy or walk away, which would mark an unprecedented rupture between Rome and the EU.

Italy is already the biggest beneficiary of the European Central Bank’s vast bond-buying program, which has helped keep a lid on its borrowing costs. The euro zone is also likely to agree to a number of schemes that would let all member nations borrow at preferential rates to fund their health-care systems and support their labor markets. Ideally, the bloc would add some form of commitment to mutualizing at least some of this extra debt between its members after the crisis.

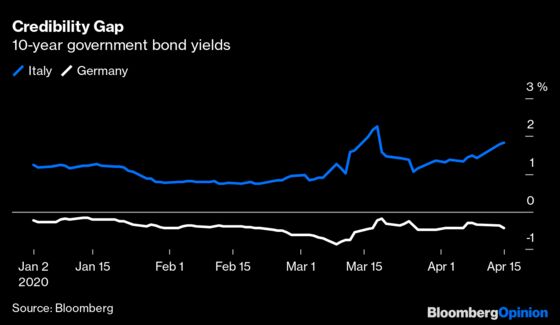

But the brutal truth is that Conte has no real leverage here. A conflict with the rest of the euro zone would spook investors, adding an Italian sovereign debt crisis to the epidemic.

Conte, who’s never been elected to parliament, is in a situation similar to the one faced by Mario Monti, another technocratic Italian prime minister, back in June 2012. At the height of the euro zone crisis, Monti tried to convince Germany to cap Italy’s borrowing rates, which were spiraling out of control. In a dramatic European Council meeting, he failed to obtain the hoped-for concessions, except for a vague commitment to use the European Stability Mechanism, the euro zone’s rescue fund, more flexibly. Luckily, Italy’s bond yields were saved a few weeks later by the then ECB president, Mario Draghi, who pledged to do “whatever it takes” to save the euro.

Conte faces a more tragic and costly crisis than Monti. But, in one way, he’s more fortunate. Over the past decade, Draghi has transformed the ECB into a more interventionist institution, fully committed to defending the single currency. Christine Lagarde, his replacement, appeared to put that role in doubt in March, when she said that the ECB was not there to close the spreads between the bond yields of weaker and stronger euro zone states. However, she has since corrected that mistake, stressing that there are “no limits” to her commitment to the euro. The central bank has bought more than 50 billion euros ($55 billion) in assets via its new pandemic-related program over its first three weeks — many of them Italian government bonds.

A Conte veto at the EU meeting would reopen old doubts over Italy’s euro membership and make it much harder for the ECB to support the country. Moreover, nothing good would come out of it politically. It’s impossible to have fully-fledged euro bonds without the Germans and the Dutch on board. While France and Spain have backed Italy’s calls for some form of joint debt issuance, they’re unlikely to join a Conte walkout. Italy risks being isolated.

Conte’s real troubles are mainly at home. Italy’s governing coalition is divided, as the left-of-center Democratic Party is in favor of a more conciliatory approach to the European negotiations, while the populist Five Star Movement is taking a hard line. Matteo Salvini’s right-wing League, meanwhile, is using its position outside power to capitalize on these divisions, expressing Salvini’s euroskeptic instincts and waging a campaign against any use of the ESM instead of fully fledged euro bonds. Coronabond supporters believe it’s fairer for the euro zone to share more of the cost of the coronavirus response because the Covid-19 outbreak isn’t the fault of any country.

Last week, Conte used an address to the nation on Italy’s lockdown to attack Salvini, a sign of just how nervous the prime minister has become.

Conte’s strategy at the EU meeting may decide his political future. In a period of emergency, his approval ratings are high, but there are creeping doubts about his ability to preside over a new phase of gradual reopening. Italy has set up a task force, led by Vittorio Colao, the former chief executive officer of Vodafone Group Plc, to advise the government on this so-called “Phase 2.” In the Machiavellian world of Rome politics, one wonders whether this is a sign that the political landscape is shifting.

For weeks, the euro zone’s dithering has given Conte a convenient political scapegoat to divert attention from a growing list of domestic failures. This has worked so far, as Italian voters have blamed Germany and the Netherlands. But the strategy seems to have run out of road. Conte has to make up his mind on where he stands; and be prepared to accept the consequences.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Ferdinando Giugliano writes columns on European economics for Bloomberg Opinion. He is also an economics columnist for La Repubblica and was a member of the editorial board of the Financial Times.

©2020 Bloomberg L.P.