(Bloomberg Opinion) -- The latest round of U.S. Treasury auctions must have left Lloyd Blankfein at a loss for words.

The former head of Goldman Sachs Group Inc. posted a perplexing tweet last week, contending that “in finance, most surprising to me is that despite the trillions the US is adding to our budget deficit and national debt, investors (many foreign) will lend the US a virtually limitless supply” of dollars at low yields. Never mind the fact that the federal government doesn’t need anyone to lend it its own currency. The dollar is not at risk of losing its reserve status, so adding to the deficit at a time of an unprecedented nationwide shutdown makes good sense. It’s not mind-boggling.

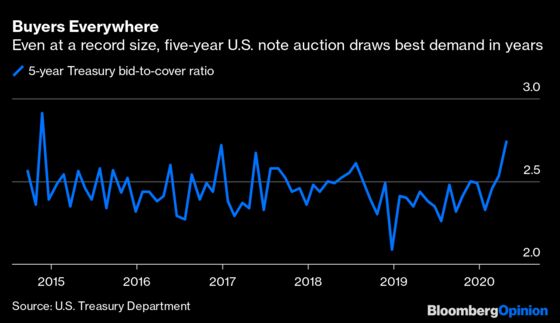

As if to hammer home the point, the Treasury’s $85 billion in combined auctions of two-year and five-year notes on Monday were nothing short of spectacular.

The $42 billion two-year offering, the largest such sale since 2010, drew a yield of 0.229%, better than the market’s indicated yield before the auction at 11:30 a.m. in New York. For bond traders, that was just the appetizer: The $43 billion sale of five-year notes, the largest ever for the maturity, yielded just 0.394%. That was easily the lowest ever, beating out last month’s 0.535%. Primary dealers, which are obligated to bid at these auctions, were left with just a 19.4% share, the lowest since August 2017, indicating strong demand from investors.

Now, I’ve cautioned before against reading too much into a single Treasury auction. A number of quirks can distort the data; for example, whether the world’s biggest bond market had been rallying or selling off in the weeks between sales, and whether that sentiment shifted right around the time of the offering.

Those caveats don’t hold up quite as well lately, however. Two-year Treasury yields have traded in a tight range of 0.185% to 0.298% over the past month, while five-year notes have traded between 0.305% and 0.514%. In other words, the yield levels at Monday’s auctions were about what bond traders have come to expect since the Federal Reserve began open-ended purchases of Treasuries to quell market volatility. These were hardly bargain prices for deals compressed into one day because of the Fed decision coming on Wednesday.

Strategists don’t seem to know quite what to make of the strong investor interest. Jim Vogel at FHN Financial called the auctions “defensive in front of major announcements on Wednesday and in light of additional gains in global risk assets.” Thomas Simons at Jefferies LLC noted that direct bidders “have come out of hibernation after largely shunning the February and March auctions,” though cautioned that “there is no guarantee we will see quite as large a bid in the other auctions going forward.”

One thing that’s clear is few investors expect shorter-dated Treasury yields to increase meaningfully anytime soon. When Fed Chair Jerome Powell cut the central bank’s benchmark interest rate to near-zero last month, he added that “we will maintain the rate at this level until we’re confident that the economy has weathered recent events and is on track to achieve our maximum employment and price stability goals.” He also noted that when it comes to the coronavirus pandemic, “we’re going to be watching, and willing to be patient, certainly.”

That sentiment likely resonates with much of America. Even as states begin to lay out their plans for a gradual reopening of their economies, there’s little sense that everything will return to the way it was anytime soon. It could well take years — and if that’s the case, why not buy five-year Treasuries at a yield 14 basis points above the upper bound of the fed funds target range?

Central bankers have proved time and again to move slowly, deliberately and transparently when tightening monetary policy. Considering how long it took the Fed to raise interest rates after the 2008 crisis, even penciling in a hike in 2025 looks ambitious at this point. Meanwhile, the specter of yield-curve control looms large.

Add it all up, and it’s little wonder why bond traders will buy Treasury notes at just about any price and in any size. They won’t provide any sort of eye-catching returns. But with the Fed’s heavy hand in the market, at least they can’t lose.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.