(Bloomberg Opinion) -- At last the creaking wheels of the European Union are starting to turn in motion — its leaders scared, no doubt, by the violent market reaction to Thursday’s underwhelming performance by European Central Bank President Christine Lagarde.

The entire viability of the euro project was once again coming into question because of the single currency area’s fractured response to the coronavirus threat. The suspension on Friday of EU deficit limit rules allows the countries most in need to react appropriately. But Europe has been well behind the curve here. Italy has already been committing tens of billions of euros to offering much-needed relief to its economy and to people who are stuck at home, unable to work. At least there is an official recognition that this is a crisis; contingency plans are being ramped up accordingly.

Most important of all is that Germany is leading the charge, possibly signaling a fundamental change in the attitude of governments everywhere toward fiscal looseness. Berlin’s Schwarze Null (Black Zero) rule, which insists on a budget balanced between fiscal spending and tax receipts, has dominated not just German but all of Europe’s budgetary discussions for a decade. I wrote last month that it might now be gone forever. The rapid spread of the coronavirus reaffirms that conviction.

The most charitable interpretation of Lagarde’s failure on Thursday to signal that she’d do whatever it takes to protect the debt of euro member states, unlike her predecessor Mario Draghi, is that she wanted to maintain the pressure on Berlin to finally succumb to reality and shoulder the fiscal burden for managing this latest crisis. Only she can answer whether that was her intention, but it’s unmistakable that the ECB’s dismal inability to reassure the markets forced Europe’s — and Germany’s — foot-dragging leaders to take action.

On Friday, German Finance Minister Olaf Scholz firmed up considerably his previous February promise to loosen the black-zero rules, saying he was prepared to put all of Germany’s economic “weapons on the table.” This includes taking on increased debt and putting no limit on the credit support available for cash-strapped companies.

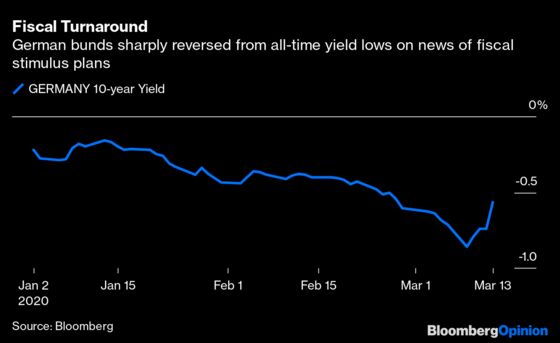

The bond markets are taking his latest comments seriously. The yield on 10-year German government bonds (known as Bunds) rose 17 basis points today to -0.57%. They’re nearly 30 basis points higher than their record low (which was only set on Monday, that’s how rapidly this markets crisis has spiraled).

Meanwhile, Italian government bonds have reversed half of their losses from Thursday, enabling a considerable narrowing of the spread between their yields and those of Germany. This is a key measure of the stability of the euro area, and the one that Lagarde blew a hole in on Thursday by saying it wasn’t the ECB’s job to worry about the yield spread. All European stock indices spiked on Friday.

Unless things go horribly wrong again in U.S. trading later, European markets will at least go into the weekend in a less fraught place. But the details of the EU fiscal response, and that of Berlin’s, need to be substantiated swiftly if the volatility is to subside properly.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2020 Bloomberg L.P.