(Bloomberg Opinion) -- Make it quick and keep it simple. That seems to have been the thinking behind Emmanuel Macron’s and Angela Merkel’s surprise master plan for a 500 billion-euro ($543 billion) Covid-19 recovery fund, to be paid for collectively by the European Union and doled out as grants to the bloc’s worst-affected nations.

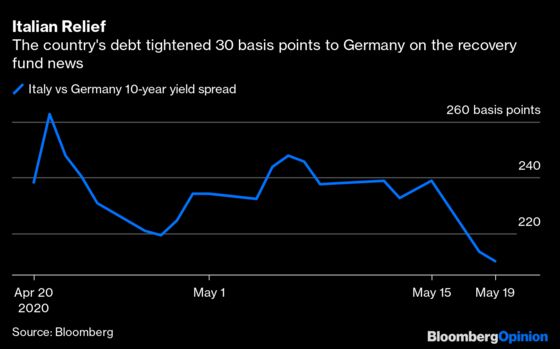

The details are yet to be thrashed out, and there’s still plenty of scope for opposition from fellow euro area members, but this does look like a genuine attempt to share the financial pain from the pandemic between Europe’s weaker and stronger nations. The spread between Italian and German 10-year bond yields fell by 30 basis points in response.

One can debate the merits of whether northern European states should be making fiscal transfers to their southern neighbors by contributing to this fund — and you can be sure that the Austrians and other hawkish nations will be doing just that — but investors would have no qualms about snapping up the new debt.

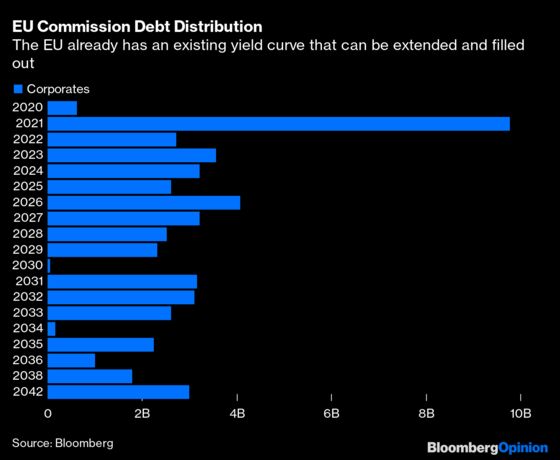

The new securities will be issued on behalf of the EU member states (their relative GDP would decide their share) by the European Commission, which is an established borrower with 52 billion euros ($57 billion) of bonds in 44 different issues and an average weighted maturity of nearly eight years. That’s a small amount when compared with the borrowings of governments, and investors will be eager that the Commission keeps its AAA credit rating from Moody's Investors Service and its AA from S&P Global Ratings even if it starts issuing a lot more debt. The Franco-German plan will only work if these securities are regarded as being of the highest quality.

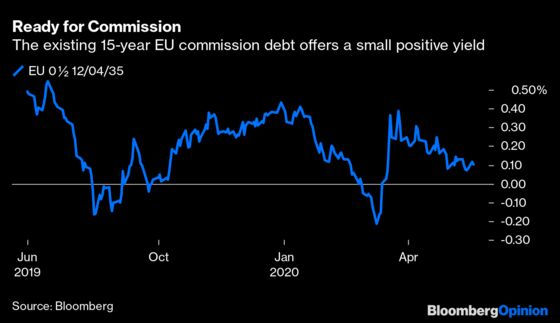

If the proposal is agreed, the new debt issued will be the closest thing yet to a true “euro bond,” with the implicit backing of all EU countries. One would expect sales of between 150 billion euros and 200 billion euros of these securities over each of the next three years. Existing Commission debt at 10- to 15-year maturities yields 40 to 50 basis points more than German bunds, meaning there might be a slight positive return for investors — a rare thing for the safest European debt.

Importantly, this new debt could also be used as gold-standard collateral, effectively as good as German Bunds, for any of the ECB's funding facilities, so it would be attractive for banks to hold.

For once, the euro area’s two dominant countries aren’t just letting the European Central Bank do the dirty work (although the ECB could help buy these bonds if needed). Instead, they appear to be trying to find a truly European solution to a crisis rather than watching as weaker nations sink under a new debt mountain. Italy might, for example, receive as much as 30% of the grants but it would be liable for only 15% of the funding. Raising the debt isn’t going to be the problem here, the politics might yet be.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2020 Bloomberg L.P.