The Financial Market’s Stress Is All About the Dollar

(Bloomberg Opinion) -- Good riddance to the worst first quarter in history. But that doesn’t guarantee Spring sunshine and flowers as winter ends. Eminent investors such as Oaktree Capital Group LLC co-founder Howard Marks and DoubleLine Capital’s Jeffrey Gundlach are warning that the worst may not be over. April really could be the cruelest month for equities as a brief bear market rally peters out and the lows are tested again. Until there’s evidence that the worst of the virus contamination is under control, the economy and financial markets are at its mercy.

Fixed-income assets have a tendency to show where equities are headed during crises and yet again U.S. Treasury bond yields are pushing lower, a clear warning of a renewed flight to quality.

While central banks have swiftly enacted the playbook learnt from the financial crisis more than a decade ago, and even parsimonious governments such as Germany’s are reaching for the fiscal checkbook, the emergency aid is only reaching higher-quality assets.

Sub-investment grade companies and non-agency mortgage debt are trapped in a downward spiral. Marks pointed to mounting job losses and business defaults and said the range of negative outcomes is wider now. Gundlach said the current economy resembles a depression and that he expects many defaults, although he advocates a hardline approach with “no government bailouts whatsoever.” That might not meet with popular approval.

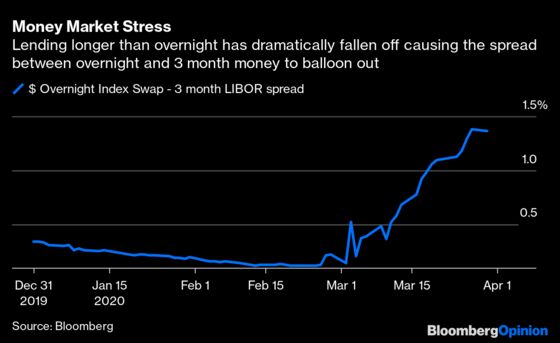

The critical faultline in the coronavirus-induced selloff has been the sudden strength in the dollar, as banks and investors globally liquidate assets and scramble for cash — above all, dollar cash. Until the Federal Reserve can satisfy onshore and offshore demand for the greenback, the economic effects of that will spread like wildfire. Everybody is desperate for liquidity, from the commercial property market to blue-chip Exxon Mobil Corp., which had to come to the bond market recently as it couldn’t get the size of funding it wanted in commercial paper.

With this lack of access to liquidity rising all over corporate America — especially in junk-rated companies — assets everywhere are being used as ATMs to raise urgent funds.

Some of the Fed’s liquidity measures won’t become fully operational until April 6, such as the crucial commercial paper funding facility, where the central bank will buy directly from eligible U.S. issuers. Until that backstop measure to ease borrowing in the corporate market kicks in, there will be little respite.

We have also just passed the end of the Japanese financial year, and there has been super-strong demand from the country’s banks for dollar liquidity. It’s been running at a rate of nearly 10 times that of European banks, which is bound to have an impact.

Until the volatility in the dollar money markets subsides there will no be peace for other asset classes and the intense pressure for liquidation will persist. The Fed is alive to the problem and has extended its dollar swaps lines to all foreign central banks (if they have an account with the New York Fed), allowing them to park U.S. Treasury bonds in return for cash.

The dollar is the world's reserve currency and the Fed is now acting as the central bank to all. Only by pumping out liquidity globally can it possibly prevent an even more almighty rush into dollars. Until it has put a lid on the money-market stress, the rest of the financial markets remain in peril.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2020 Bloomberg L.P.