The Fed Proves It Will Do Whatever It Takes in Repo

(Bloomberg Opinion) -- The phrase “whatever it takes” is something of a buzzword lately when discussing how to deal with the coronavirus outbreak and its impact on the global economy.

Echoing a phrase famously used in 2012 by Mario Draghi, the president of the European Central Bank at the time, German Chancellor Angela Merkel, Italian Prime Minister Giuseppe Conte and U.K. Chancellor of the Exchequer Rishi Sunak have repeated that pledge in recent days. Even U.S. President Donald Trump, confronted with stocks on the precipice of a bear market, took to Twitter to say he’s “fully prepared to use the full power of the Federal Government.”

Federal Reserve Chair Jerome Powell hasn’t gone quite that far — at least not yet. He said last week after the central bank’s emergency 50 basis point interest-rate cut that he and other policy makers “can and will do our part.”

Yet actions speak louder than words to financial markets. So give credit to the New York Fed for quickly and decisively taking action around its repurchase operations amid signs of a cash squeeze across Wall Street. It indicates that the central bank is very much willing to do whatever is necessary to avoid a full-blown crunch as financial markets whipsaw.

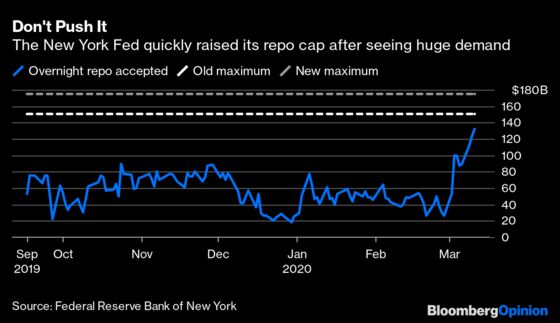

The New York Fed announced Wednesday that it would increase the maximum size of its daily overnight operations to $175 billion starting Thursday and lasting through April 13. That’s up from $150 billion, which was just announced on Monday. Before that, the amount of overnight cash available for the banking system was capped at $100 billion. It will also conduct three one-month operations of at least $50 billion beginning Thursday, providing a longer-term lending option that hasn’t been available since it set up term repo actions that covered year-end 2019.

It’s no secret why the Fed is stepping up its efforts. The New York branch took about $132 billion of securities in its overnight repo operation on Wednesday, the largest since the funding market meltdown in September. That’s a bit too close to comfort for the central bank, which was clearly trying to avoid another round of oversubscribed operations with its move just days ago.

Then the stock market plunged. Then Bloomberg News reported the following:

- Boeing Co. is planning to draw down the full amount of a $13.8 billion loan as early as Friday.

- Hilton Worldwide Holdings Inc. intends to draw down a portion of its $1.75 billion revolving credit line in response to market turmoil.

- Blackstone Group Inc. is directing its portfolio companies to draw down their bank credit lines to help prevent any liquidity shortfalls.

- Wynn Resorts Ltd. will draw down a portion of its $850 million revolving credit line.

Put together, it would seem as if Wall Street is in the midst of a full-blown cash crunch.

That’s probably an exaggeration. Revolving credit lines, after all, are meant to be tapped during tough times. Companies like Hilton and Wynn, facing tremendous uncertainty about their core businesses because of the coronavirus, are certainly well within their rights to first use their revolvers to bridge the tumult rather than make more drastic, permanent decisions.

If even more companies follow their example in the coming days, though, it could damage the banking system. As I’ve written before, the current crisis is hardly a financial one — but that’s assuming that the economy doesn’t deteriorate to the point that borrowers can’t repay what they owe. Bloomberg News’s Sridhar Natarajan and Heather Perlberg, who broke the news on Blackstone, summarized the situation nicely:

Banks offer revolving credit lines to strengthen relationships with companies and don’t typically intend for them to be drawn upon en masse. In normal times, revolvers serve as the corporate equivalent of credit cards, giving companies room to borrow as needed and repay when shortfalls ease — and under normal circumstances, the lines are seldom maxed out. Extensive use can be seen as a harbinger of distress.

The great news for Fed officials is this is an issue that they’re uniquely positioned to help mitigate. Its repo operations are specifically meant to ease pressure on funding markets and ensure ample cash reserves in the banking system. It should come as no surprise that the central bank’s balance sheet jumped in the week through March 4 by the most since October. And unlike, say, interest-rate cuts to fight a pandemic, the central bank has the capacity to directly provide cash to the financial institutions that need it.

A statement from the New York Fed hinted at that reasoning. The increased operations “should help support smooth functioning of funding markets as market participants implement business resiliency plans in response to the coronavirus,” the bank said. “The Desk will continue to adjust repo operations as needed.”

This is exactly the type of nimble action that the Fed should be focused on during this market tumult. Standing ready to provide liquidity to the banking system is arguably more valuable at this point than dropping short-term interest rates by an additional 50 or 75 basis points. Powell will almost certainly still go through with a rate cut — the markets have long since concluded that — but it’s vital that policy makers not fall asleep at the wheel again with regards to the market plumbing.

It might not be of much comfort to traders so soon after the Dow Jones Industrial Average fell into a bear market. But the Fed appears willing to do whatever it takes in repo. That could make all the difference in preventing the tumultuous market moves from descending into a full-blown crisis.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.