Europe’s Rescue Package Gives Bond Yields a Chance

(Bloomberg Opinion) -- European bond buyers are currently trapped between the devilishly unpredictable mood swings of higher-coupon government debt such as Italy and Greece, and the deep blue sea of top-rated but sub-zero yielding German bunds. But salvation is on the horizon — both for fixed-income fund managers and our pensions.

Investors starved of yield are in for a treat in the coming years, as the European Union’s pandemic response creates a sizeable increase in one flavor of top-quality securities offering more bang for a buck than is available from lending to Germany.

The European Commission is trying to get member states to agree on a rescue package that, as it currently stands, would disburse 500 billion euros ($560 billion) of grants to those countries most in need, along with 250 billion euros of loans. The wrangling has centered on how much should be lent and how much should be given, with the so-called frugal four — the Netherlands, Sweden, Austria and Denmark — pushing for a bigger slice of the aid to be repaid. However, there are signs that opposition is easing in some corners.

In true European fashion, the bloc will eventually fudge some sort of compromise. Whatever the final agreement, bond sales will fund the bulk of the package — with the Commission itself borrowing in the name of the EU and poised to become a much bigger supplier of bonds on the capital markets than it is currently.

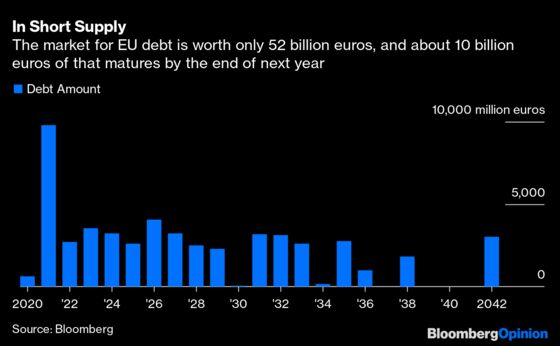

As my colleague Marcus Ashworth argued last month, EU debt is the closest thing the region offers to a euro bond backed by all of the bloc’s members. But with just 52 billion euros of debt outstanding, the Commission is dwarfed by the bloc’s other supranational borrowers. The European Investment Bank, for example, has 463 billion euros of bonds in existence. The European Financial Stability Facility has almost 200 billion euros and the European Stability Mechanism contributes about 93 billion euros of tradeable securities.

New bonds sold in the EU’s name were set to total just 800 million euros this year, according to analysts at Rabobank Group. They anticipate that the economic aid package means that between 2021 and 2024, the EU’s bond sales will increase by 125 billion euros per year, qualifying it as “a notable funding uptick.”

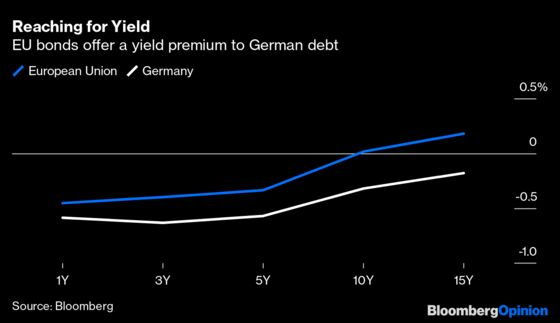

Moreover, Rabobank reckons those additional sales can be absorbed without undermining the EU’s credit ratings as a borrower, currently AAA at Moody’s Investors Service and AA at S&P Global Inc. That’s great news for investors looking for top quality bonds that offer more yield than German bunds, the region’s benchmark securities.

Fund managers have certainly got their bond-buying boots on. This week, Europe’s bond market surpassed sales of 1 trillion euros of new issues for the year, reaching that amount at the region’s fastest pace ever. For those of us worried about how our pensions will fund retirement, the prospect of more long-dated supply from a top-rated borrower offering even a smidgen of positive interest is a welcome relief.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2020 Bloomberg L.P.