(Bloomberg Opinion) -- About two years ago, I wrote my first column on collateralized loan obligations. It followed a Barron’s article pointing individual investors to funds that buy the riskiest equity and junior debt of CLOs and offer double-digit yields. I posited that the peak must be close, based mostly on a hunch that markets only get truly frothy when mom and pop show up.

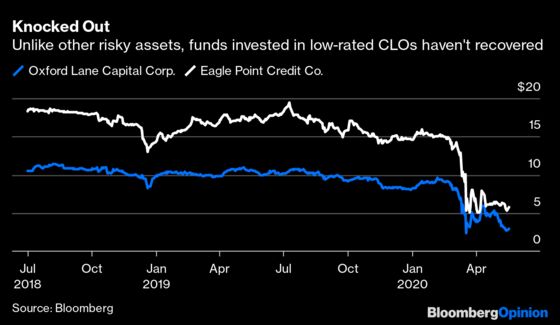

With the benefit of hindsight, that turned out to be about right. Oxford Lane Capital Corp., a fund flagged by Barron’s that traded at $10.53 in July 2018, would top out at $11.50 a month later. It’s now worth just $3, not far from its low in March. Eagle Point Credit Co., which traded at $18.65 at the time, would climb by less than a dollar over the following year and is now hovering around $5.75. While these investments are known for their high yields, that’s still a steep loss in total value. And unlike public equities and even high-yield bonds, the funds show little evidence of rebounding anytime soon.

What’s happening here? In the words of S&P Global Ratings: “The CLO structures are working as intended during periods of economic stress.”

It truly is as simple as that. The equity and mezzanine tranches of CLOs offer huge returns but carry the risk that at the first sign of trouble, they’ll get nothing. It’s all part of how the structure is designed to protect the highest-rated portions, which famously never defaulted during the financial crisis and are owned widely by conservative investors like Japanese banks.

And trouble has surfaced. Since early March, some 440 of the more than 1,500 obligors held in broadly syndicated U.S. CLOs rated by S&P have either been downgraded, placed on a negative CreditWatch, or both. Consequently, S&P has gradually put lower-rated CLO tranches themselves on negative CreditWatch, with the tally reaching 418 as of May 8. That usually either results in a downgrade or no change within 90 days. Meanwhile, Moody’s Investors Service has 859 CLO tranches worth $22 billion on downgrade watch.

That portends more pain ahead for those who have tried to ride out the worst of the market’s swoon. Oliver Wriedt, chief executive officer of DFG Investment Advisers, said last week in a Bloomberg TV interview that “weaker hands” in the CLO market could be forced to sell in the coming months. Some investors might “be unable to hold tranches that are downgraded or tranches that are no longer current-pay,” he said. Many CLOs are next scheduled to distribute cash in early July. According to Bloomberg News’s Adam Tempkin, it’s likely more of them will breach key compliance tests by then, meaning some payments will shut off.

“We’re excited about picking winners and avoiding losers in a market where that skill will be richly rewarded,” Wriedt said. Thus far, his company has been active in investment-grade tranches while treading cautiously among riskier parts of the debt stack.

While the complete story of this economic collapse has yet to be written, one of the core themes of the first few months has been the short-lived opportunities for those investors looking to scoop up bargains. Legendary market gurus like Berkshire Hathaway’s Warren Buffett and Oaktree Capital Group LLC’s Howard Marks have pointed out that the Federal Reserve’s interventions across asset classes have kept prices from falling to levels they deem attractive.

CLOs and leveraged loans are proving to be something of an exception. Triple-B and double-B CLO tranches have lost roughly 14% and 24%, respectively, so far this year. “We’re not expecting the support programs to meaningfully include the loan or CLO market,” Wriedt said. He’s buying with the expectation that “we’ll have to work this out by ourselves.”

For its part, the Fed is well aware of the potential pain ahead for CLOs. Its latest Financial Stability Report, released May 15, doesn’t mince words when it comes to the structures:

Defaults on leveraged loans ticked up in February and March and are likely to continue to increase, with the specific contour highly dependent on the path of overall economic activity. Such developments would weaken the balance sheets of lenders, including CLOs that hold leveraged loans, and amplify the economic effects of COVID-19.

…

Many lower-rated CLO tranches have been put on negative watch by rating agencies, indicating that material downgrades to those tranches are likely in the future. Some CLO investors such as hedge funds purchase lower-rated tranches using leverage. Downgrades of CLO tranches could result in margin calls on leveraged investors, forcing them to reduce their exposure by selling their holdings. Such sales have the potential of putting additional pressures on leveraged investors.

It’s hard to spin this as anything other than ominous. Which, naturally, seems to be precisely why opportunistic credit funds are starting to circle this market waiting for the right time to pounce.

Just last week, Bloomberg News’s Sally Bakewell reported that Tubkal Credit Partners, a fund set up with family office capital, is aiming to raise $100 million to invest in beaten-up European and U.S. lower-rated CLOs. That follows similar moves from Napier Park Global Capital and Neuberger Berman. These new funds signal that those looking for outsized profits need to act fast. Morgan Stanley strategists wrote last week that most speculative-grade European CLO tranches will ultimately return full par and deferred interest to investors, though not without the potential for wide price volatility in the interim.

Which brings it back to individual retail investors, who are often less willing to ride through painful times than institutional managers. It’s hard to say how many of them bought risky CLO exposure a couple of years ago. However, it’s clear institutions are beginning to nibble now.

Neuberger Berman added 400,000 shares of the Oxford Lane closed-end fund sometime in the first quarter, or about 0.5% of the shares outstanding, the biggest increase in limited data compiled by Bloomberg. Freestone Capital Management, an independent wealth adviser to high net worth families and institutions, piled the most into the Eagle Point fund in the three months through March. Private-equity firm Stone Point Capital holds almost 20% of the Eagle Point shares (though, as it happens, trimmed its position in mid-2018).

With all the high-profile investors flummoxed at how stocks and risky corporate bonds can rally through a pandemic, CLOs and leveraged loans will be worth monitoring as some of the few the assets left behind. So far, they’ve inflicted serious pain on those who were left holding the bag when the coronavirus struck.

But more risk takers will likely mobilize to buy low-rated CLOs on the brink of downgrades in the next few months. It could be little more than a desperate move, especially if global economy recovers more slowly than anticipated. But it’s about all that can be done to aim for high returns at a time when central banks are doing everything in their power to suppress volatility.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.