(Bloomberg Opinion) -- The U.K. Debt Management Office (DMO) has put out a signal of intent: More government bond supply is about to come thick and fast. The amount of gilts to be sold in April will be raised from 20 billion pounds ($22 billion) to 45 billion pounds.

Boris Johnson’s government needs swift access to more funding to support the economy during the coronavirus shutdown. The good news is the bond market can handle it with ease, even in a market environment like this one. It helps enormously that the U.K. Treasury and the Bank of England are working in lockstep to deal with the financial side of the Covid-19 crisis.

It makes sense to front-load the surge in Gilt issuance, as the BOE is already ramping up its Quantitative Easing bond-buying program by 200 billion pounds in an accelerated schedule. The net effect on investor demand should therefore be fairly muted, as the central bank will be in the market, hoovering up debt.

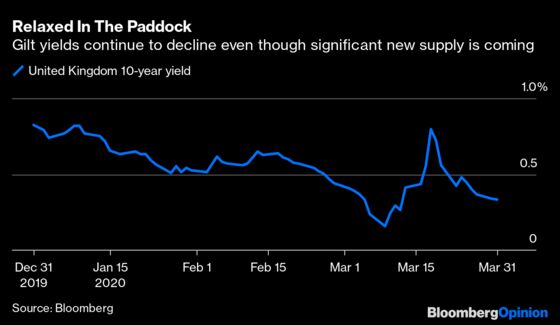

Thankfully the DMO, which operates as the Treasury’s agent in the debt market, has vast experience in this area from the financial crisis a decade ago. Even after more than doubling the size of April’s gilts sale, the yield on the benchmark 10-year note was little changed at 31 basis points, not far from its record low yield of seven basis points seen on March 9.

Britain’s coordinated response to the economic mayhem has been genuinely impressive, and groundbreaking. The DMO and the central bank are working together to smooth out what — according to analysts from Royal Bank of Canada — could be a doubling of overall debt sales across the whole of the upcoming financial year (April to April) to about 300 billion pounds. There will be 17 gilt auctions in April alone. This is a full-blown emergency response.

It’s especially important to tread carefully with this almost unprecedented surge in supply with the most sensitive and illiquid longer maturity gilts. The DMO is limiting issuance of the longest-dated stuff to 12 billion pounds in April, which will be outweighed by planned BOE purchases of 21 billion pounds. The central bank has raised its total purchases of assets to nearly 5 billion pounds on three days per week and will probably buy more than 60 billions pound in April alone, easily exceeding new supply.

The two entities are having to be careful not to get in each other’s (or investors’) way by making sure the BOE doesn’t snap up too many of the most in-demand bonds, and equally not to overload any sector.

The BOE only buys from investment bank primary dealers in the secondary market rather than directly from the Treasury but the rules might be relaxed with so many auctions taking place, to avoid straining the primary dealers’ balance sheets. This could necessitate direct monetary financing , as former BOE deputy governor Charlie Bean said this week, meaning the BOE actually buys straight from the Treasury. With so many traders working from home, the risk of an operational glitch causing a failed auction is disproportionately high. The authorities need an insurance policy.

Both debt issuance and QE buybacks will probably tail off later in the year and both can be altered together if the economic situation improves — or worsens. This is a make it up as you go along moment, but as long as the communication to the market remains as clear as it has been, any amendments shouldn’t cause problems. It helps that the average maturity of U.K. debt is significantly longer than all other major bond markets at 15 years, meaning there’s less urgency in refinancing debt. But having such joined-up institutions in the country’s hour of need is very fortunate.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2020 Bloomberg L.P.