Do You Really Want To Bet Against Howard Marks?

Stock investors turn pessimistic again, with good reason. Plus, dividend dilemmas, Carnival credit and more.

(Bloomberg Opinion) -- The optimism that permeated equity markets last week when U.S. stocks posted their biggest gains since the 1930s has once again given way to a feeling of despair, with the S&P 500 Index falling 6% over the course of two days. Yes, moves by fiscal and monetary authorities have shored up the all-important “plumbing” of the financial markets, but that is looking more and more like an act of triage than a catalyst to recovery. No one at this point in the pandemic crisis can confidently say how deep and long-lasting the coming recession will be, and that’s keeping markets stuck in their own form of purgatory.

The conundrum facing investors was underscored by a pair of developments out of JPMorgan Chase & Co. this week. At the same time the biggest U.S. bank’s research department was pronouncing that most risk assets — a universe that typically includes stocks — have seen their lows, its asset management division was cautioning investors against rushing to buy. In all fairness to JPMorgan, it’s not uncommon for different parts of the same financial firms to having opposing views. And contrasting views are what makes markets happen. But to cut through the noise, it’s often best to seek out the best and brightest, and in that regard, few on Wall Street compare with the legendary Howard Marks, whose Oaktree Capital Group LLC oversees about $125 billion. In a career that extends all the way back to the 1960s, Marks has seen it all — from the Vietnam War to the oil embargo of the 1970s, rampant inflation, double-digit interest rates, 1987’s Black Monday crash, catastrophic terrorist attacks on the U.S., a financial crisis and seven recessions. If that’s not impressive enough, consider that Warren Buffett once said that "when I see memos from Howard Marks in my mail, they're the first thing I open and read.” So, what did his latest memo released late Tuesday say? In essence, stay cautious.

“Assets were priced fairly on Friday for the optimistic case but didn’t give enough scope for the possibility of worsening news,” Marks wrote in the note. He added that during the 2008 financial crisis, he was concerned about the implications for the economy from bankruptcies among financial institutions, but there was “no obvious threat to life and limb.” With the escalating Covid-19 pandemic, the range of negative outcomes seems much wider, he wrote. In other words, the path of least resistance for stocks is probably lower.

THIS ISN’T HOW IT’S SUPPOSED TO WORK

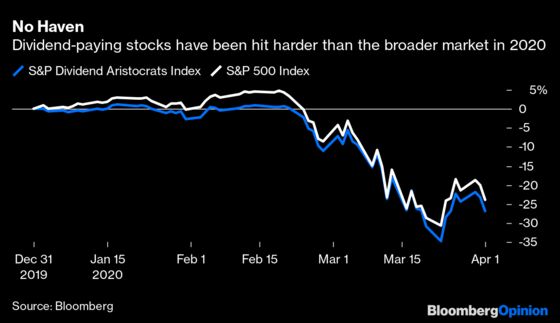

One of the basic tenets of market theory is that dividend-paying stocks are inherently “safer” than those that don’t make payouts. The thinking is that dividend payers have stable and predictable cash flows. But like so much in markets these days, this theory is proving false. The S&P 500 Dividend Aristocrats Index, which tracks those companies in the benchmark gauge that have consistently increased payouts every year for at least 25 years, is down 26.4% this year, compared with a drop of 23.5% for the S&P 500. The strategists at BNY Mellon looked into the outlook for dividends and concluded that the market is pricing in a 41% drop in dividends for members of the S&P 500 through 2021, declining to $38 per share from a recent high of $63 per share. The good news is that markets expect dividends to begin to recover in 2022. The bad news is they won’t recover to their pre-coronavirus levels until 2030. What does that mean for stock prices? Perhaps a 20% decline from current levels, the strategists conclude.

WHAT ARE THEY THINKING?

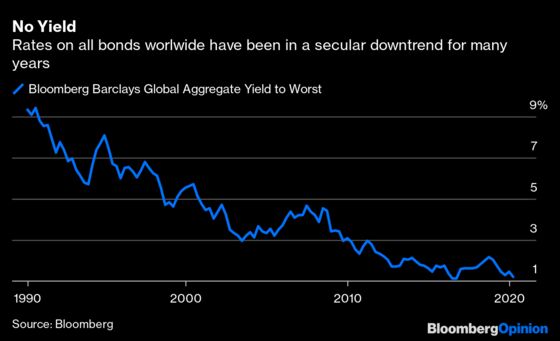

The world is finding out just how hungry yield-starved investors have been. For years, bond investors have complained that yields were too low to compensate for the risk. In a world with $17 trillion of debt with negative yields, and yields overall hovering around 2% on average for much of the past decade, they weren’t wrong. But it’s not unusual for those who are starving to experience hallucinations, which may explain the booming demand for a bond offering from cruise line operator Carnival Corp. My Bloomberg Opinion colleagues Brian Chappatta and Matt Levine have pointed out here and here the seeming folly of lending money to a business that is facing the real risk of collapsing. But that hasn’t stopped the company from boosting the size of the offering to $4 billion from $3 billion, while trimming the proposed yield to 12% from 12.5%. Of course, such yields are well above the 9.5% for the average junk bond, but not outrageously so. The point here is that Carnival can issue bonds, suggesting credit markets aren’t experiencing a buyers’ strike. That’s something markets can be thankful for amidst all that is happening.

WHO WILL RESCUE EMERGING MARKETS?

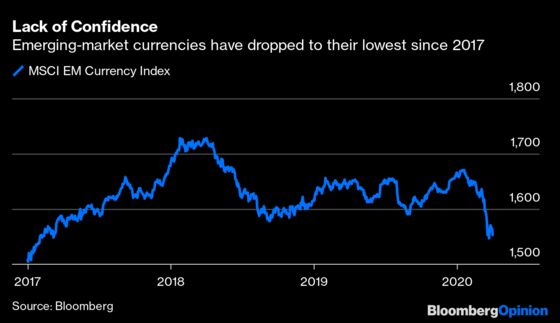

Emerging markets took another beating Wednesday, with the MSCI EM Index of equities dropping as much as 2.75% to bring its year-to-date decline to 26%. An MSCI gauge measuring EM currencies has fallen 6.68% in 2020. To put that move into context, its previous record decline for a full year was 8.68% in 2008. (The index was launched in 1997.) The Institute for International Finance estimates that a record $83.3 billion was pulled out of emerging-market portfolios in March. There’s good reason for investors to be jittery. Unlike in the Group of 10 countries, many developing economies don’t have powerful central banks or financial authorities than can take the steps taken by the likes of the Federal Reserve. If they run into trouble, their only hope is a bailout by the International Monetary Fund. Citigroup says 85 countries have already asked the IMF for emergency assistance. It’s not an issue of money; the IMF says it has $1 trillion of lending capacity, with about a fifth of that having already been loaned or committed, according to Citigroup. The real issue lies in the IMF’s “traditional insistence on belt-tightening,” which “seems inappropriate in the current circumstances,” Citigroup notes. “One way of easing belt-tightening requirements will be to ask private-sector creditors to bear some of the burden of easing countries’ payments problems,” it added. No wonder so much has flowed out of emerging markets.

TEA LEAVES

It’s time again for the world’s new most important economic number: weekly U.S. jobless claims. Last week’s numbers provided a glimpse of just how bad the coming employment situation will get. The government said a record 3.28 million people filed for unemployment insurance in the week ended March 21, surging from 282,000 the previous period and dwarfing median estimate of about 1.7 million. To be sure, those estimates were really just a stab in the dark, with forecasts ranging from 360,000 to 4.4 million. And Thursday’s number will be a crap shoot as well. The median estimate of economists surveyed by Bloomberg is for an increase to 3.6 million, but the forecasts range from 800,000 to 6.5 million. No one knows how to model an economy coming to a sudden stop, which is why estimates for most data points are all over the place. That’s likely to be the case through at least this month, helping to keep volatility elevated.

DON’T MISS

Markets Can’t Ignore 4 Crucial Uncertainties: Mohamed El-Erian

The Federal Reserve Shouldn’t Rescue Everyone: Bill Dudley

Jeffrey Gundlach Stress Is All About the Dollar: Marcus Ashworth

Critics of Stock Buybacks Will Outlast Coronavirus: Justin Fox

Maybe Coronavirus Didn't End the Bull Market: Barry Ritholtz

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2020 Bloomberg L.P.