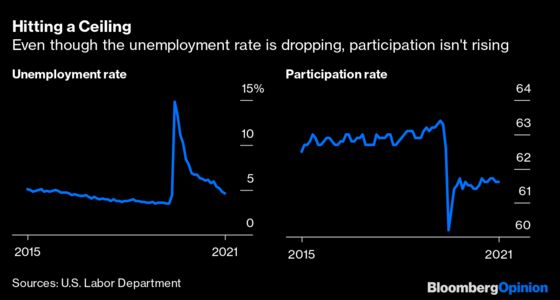

(Bloomberg Opinion) -- Economists are generally a “glass half empty” bunch. So while they cheered the U.S. Labor Department’s monthly jobs report on Friday, which showed the unemployment rate dipping to a pandemic-era low of 4.6%, they also bemoaned a labor force participation rate that has become stuck at around 61.6% since the summer of 2020. Before the pandemic, it was more like 63.5%. That may not seem like much of a difference, but it accounts for the 5 million or so jobs that have yet to return.

The thinking is that the economy won’t be able to meet its full potential until those workers who are still on the sidelines decide to seek employment. The economists at Wells Fargo & Co. went so far as to write in a report that the lack of improvement in the labor force participation rate may give the Federal Reserve “pause as it considers the strength of the overall labor market recovery.”

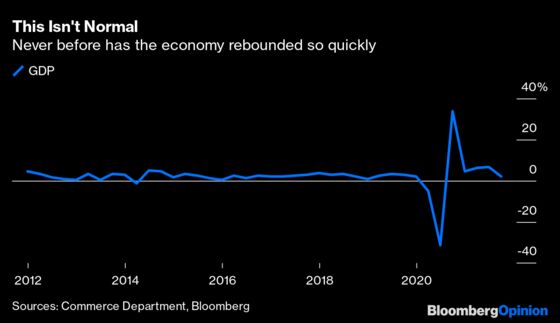

Maybe, but the pandemic has rendered data that was once seen as insightful almost irrelevant because of the unprecedented fiscal and monetary support provided by the government and the central bank. Using the participation rate, and even the number of jobs overall, to help divine what may lie ahead for the economy feels a lot like a football coach still working with a playbook from the time before the forward pass was introduced. Nothing in the economic textbooks envisioned an economy that stops on a dime, jettisons some 17 million from the workforce over two weeks and contracts 31% only to rebound just as quickly on the back of free-money government programs.

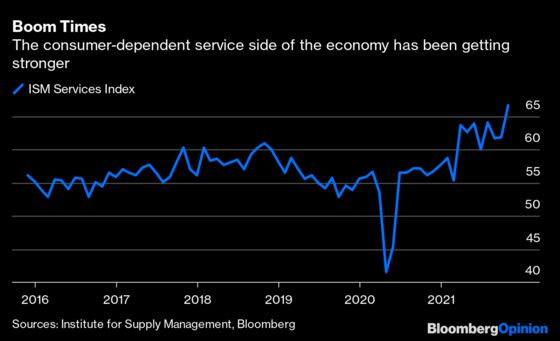

It’s looking more and more as if economists need to rethink whether “full employment” even matters. Rather than looking at how many people are working, perhaps it’s better to look at their activity. That is why this week’s Institute for Supply Management services index was so important. Even with a depressed labor force participation rate, the gauge managed to soar to a record for October. It advanced to a reading of 66.7, up from 61.9 in September and exceeding all projections. All 18 services industries tracked by the Institute reported growth last month, led by retail trade, transportation and warehousing, and real estate.

Clearly, consumers are in a good spot heading into the all-important holiday shopping season. But the question is how good? We already know that household net worth as measured by the Fed reached another record in the second quarter, jumping $5.8 trillion to $141.7 trillion, led by a $3.5 trillion gain in the value of equities and a $1.2 trillion rise in real estate. That brought the increase over the four quarters ended June 30 to $23.2 trillion. The all-time high for any one calendar year was $11.6 trillion in 2019. On top of that, Tom Porcelli, the chief U.S. economist for RBC Capital Markets, calculated in a report this week that wages for the year are already about $400 billion higher than they would have been had the pandemic never happened, using a pre-pandemic baseline estimate. Here’s how he put it:

In the immediate years prior to the pandemic, wages and salaries would grow that much over the course of a year. Viewed from that lens, by the time we get to the end of this year, the consumer could be sitting on nearly an extra year of income gains.

And don’t forget that Americans have also built up $2.7 trillion of excess savings since the start of the pandemic, according to Bloomberg Economics, about triple what it is normally. It’s also almost four times the average annual increase in gross domestic product during the last expansion and equivalent to the annual GDP of the U.K. It’s little wonder that the National Retail Federation predicts that U.S. holiday sales will surge 8.5% to 10.5% this year compared with those in 2020.

It’s important to understand why there are still five million fewer jobs now than just before the pandemic despite widespread reports of employers struggling to find workers. For one, the economists at the Federal Reserve Bank of St. Louis calculate that more than three million Americans retired early because of the Covid-19 crisis. They point out that the big gains in household wealth have made it possible for young baby boomers to stop working.

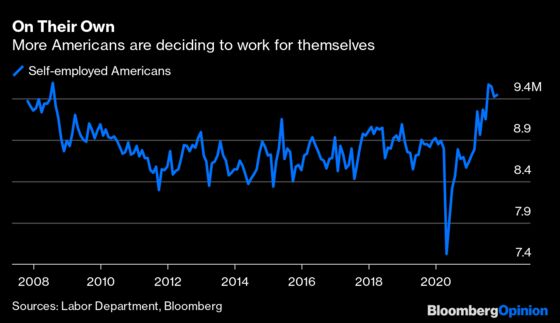

Then there are those who lost their jobs during the early days of the pandemic and decided to strike out on their own rather than return to work for someone else. The Labor Department’s monthly jobs report is notorious for undercounting the self-employed and so-called gig workers, but the data it does provide in this area reveals a trend. The report for October showed that about 9.5 million Americans are self-employed, the most since mid-2008.

There’s no doubt that it’s better for society — and the economy — if as many eligible workers as possible are actually working. However, for the foreseeable future, meaning well into 2022, it’s probably better to watch what consumers are doing through reports such the Institute for Supply Management’s services index rather than how many people are working to determine where the economy and markets may be headed.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is the executive editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2021 Bloomberg L.P.