(Bloomberg Opinion) -- ConocoPhillips knows how to please a crowd, even one as shrunken and beaten-down as energy investors. By Tuesday lunchtime, as Conoco’s analyst day was wrapping up in Houston, it was the only big U.S. oil and gas stock flashing green, what with oil prices slipping almost 3%.

This says a lot about why Conoco’s message resonates: It comes with a hefty dollop of FUD.

“Fear, uncertainty, doubt” is what bears thrive on, but Conoco has refined it into something useful. CEO Ryan Lance set the tone with an opening slide called “Two Charts We Can’t Ignore,” showing how oil had dropped from its pre-2015 triple-digit level to the “new normal of lower, more volatile prices” and how the sector’s weighting in the S&P 500 had slumped from 12% in 2012 to today’s 4%. The subtitle of that slide could have been “but Lord knows the industry has tried to ignore them anyway,” which is how it ended up at that 4% weighting.

Hence, Conoco continues to beat a different drum. The common thread running through Tuesday’s 152 slides is that oil and gas production is a mature business with a bad track record on capital management and a future clouded by climate change. There is no room for banking on higher commodity prices, and investors have given up paying for the oil option in E&P equities anyway.

So forget exuberance and focus on resilience. Conoco’s message can be boiled down to cutting its breakeven cost per barrel and returning a lot of cash to shareholders. It plans on generating $12 billion a year of cash from operations, on average, through the 2020s, of which 60% goes to capital expenditure and 40% to buybacks and dividends. The latter equate to about 80% of the current market cap and are split themselves 60/40 in favor of buybacks, reflecting the reality of the cycle.

Conoco bases its math on a $50 real oil price and expects production would grow by roughly a third over the next decade — or, factoring in the buybacks, significantly more than doubling on a per-share basis. Altogether, a projected average return made up of 8% free cash flow yield plus 3% growth is tailor-made for today’s energy investor, in contrast to the old, failed paradigm of a 10%-plus return owing everything to growth and nothing to payouts. Needless to say, Conoco was at pains to emphasize its cautious view on potential acquisitions, fear of which has weighed on the stock this year as fracker valuations have collapsed.

None of this makes Conoco immune to oil’s vicissitudes, of course. Free cash flow tilts toward the back end of the decade, and the company would effectively borrow to fund some of its buybacks through 2025, at $50 oil. That said, having cut net debt by two-thirds since the end of 2016, Conoco doesn’t envisage leverage rising to even one times Ebitda in 2025. Under a stress-test scenario, where oil prices average $40 a barrel between 2023-25, the company doesn’t see leverage breaching two times Ebitda.

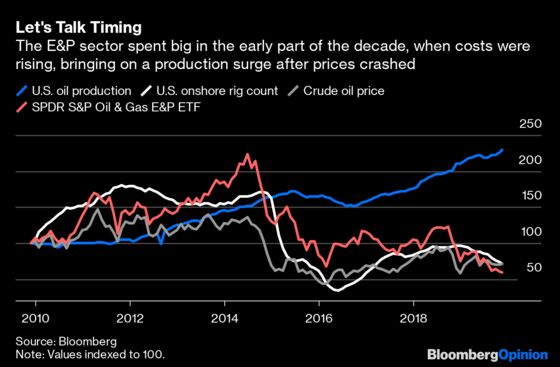

Let’s just step back here in 2019 and acknowledge that, looking back at everything that’s unfolded in oil over the past decade, any 10-year projection should be treated less like a Google map and more like asking someone on the street for directions. Indeed, for me, the most important slide in Conoco’s deck looked back rather than forward . Here, COO Matt Fox talked through lessons learned from prior investment programs, chief of which is to stop committing the industry’s original sin: pro-cyclicality. In other words, don’t base your spending on how much spending power you have at any given moment. Rather, by targeting low breakeven costs, which factor in wherever the industry happens to be in the cycle, you smooth out investment and minimize spending when cost inflation is high and bringing on new production just as commodity prices turn down.

This spend high/sell low approach pretty much sums up what the industry did over the past 10 years, vaporizing capital in the process. The chart below uses the U.S. onshore rig count as a proxy for industry capex, and you can see how it surged in the early years on the back of high oil prices, with much of the subsequent growth in production arriving after prices crashed. Even though frackers made real gains in efficiency in that time, the performance of the sector ETF tells you what this did to returns:

This is especially important in the context of the new mantra being preached by many E&P companies today: namely, that they will live within their means. Conoco’s message is that just ensuring you don’t spend more than you make in a given year isn’t the cure for the sector’s ills. Rather, it’s about smoothing spending, production — and thereby payouts — over time in order to escape the boom and bust cycle. It is the latter that has eroded confidence in the industry’s earnings and, hence, led to lower and lower multiples being put on those earnings.

Fear and doubt will always attach to oil prices, but companies can do something about uncertainty.

Slide 32 if you download the deck.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.