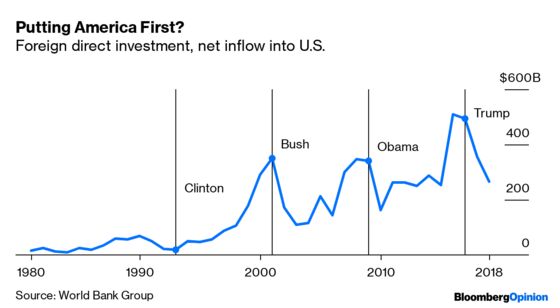

(Bloomberg Opinion) -- President Donald Trump promised to put America first when he campaigned for the White House. Today, after two and a half years of tax cutting, tariff boosting and assaults on globalization, foreign direct investment has fallen the most in almost two decades amid dwindling confidence by business leaders about continued U.S. prosperity.

The 45th president roiled so many symbiotic relationships between the U.S. and its major trading partners in Canada, China, Europe, Japan and Mexico that chief executive officers here and abroad have grown skittish about long-term commitments during the No. 1 economy's record-long expansion. Instead of using most of their cash to build new plants or invest in new equipment, CEOs are putting more of it into buying back company shares.

Trump inherited the only developed economy to rebound to a record gross domestic product and which produced the largest increase in jobs after the 2008 recession. But since he became president in 2017, net foreign direct investment in the U.S. tumbled 28% in his first year and another 25% in 2018, according to World Bank Group data compiled by Bloomberg. The last time the U.S. experienced such a double-digit loss in FDI over the first two years of a presidency was 2001 (-51%) and 2002 (-36%) when George W. Bush occupied the Oval Office.

When Trump signed the Tax Cuts and Jobs Act of 2017 — reducing the corporate rate to 21% from 35% and also adding more than $1 trillion to the budget deficit — he promised that the law would prompt U.S. and non-U.S. companies to put their repatriated overseas funds into new American facilities and jobs. At the same time, Trump abandoned the U.S. commitment to the 11-member Trans-Pacific Partnership, renegotiated the North American Free Trade Agreement (belittling steadfast allies Canada and Mexico) and imposed tariffs on Chinese products sold to Americans. All of which, he predicted, would create a wave of investment from abroad.

It's not happening. While foreign-owned companies have a history of investing more in research and development, wages and benefits than comparable U.S.-owned businesses, they're not rushing to the U.S., said Gary Hufbauer, senior fellow at the Peterson Institute for International Economics, in an interview with CNN last month. Instead of causing overseas firms to move operations to the U.S., Trump's tariffs tend to have the opposite effect because tariffs increase the cost of supplies foreign-owned companies would need to import to make their products, Hufbauer explained.

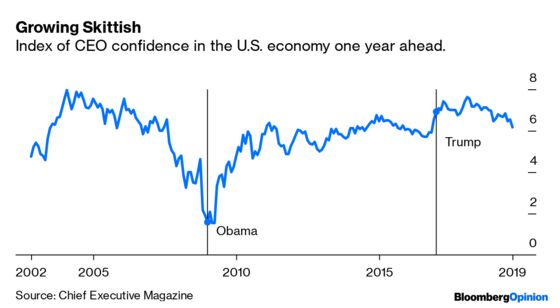

Business leaders initially embraced Trump’s tax cuts and rollback of President Barack Obama's environmental, health and consumer protections. When Chief Executive Magazine surveyed CEOs about their confidence after Trump was elected, he benefited from a surge of 1.7 points, the largest 15-month gain since 2014, according to data compiled by Bloomberg. But their outlook changed at the beginning of 2018 when the same measure began its descent of 1.7 points, the biggest 19-month drop since April 2009 during the recession. Launched in the context of a beggar-thy-neighbor trade policy, the tax cuts proved ineffectual.

Corporate America was more optimistic about its future under Obama, when the confidence measure rose 427 basis points during his first two years as president. That's also when billionaire investor Warren Buffett made the biggest bet on the nation's prospects when he acquired the Burlington Northern Santa Fe railroad for $44 billion. During Trump’s first two years, it fell 49 basis points. The lack of confidence in Trump is unprecedented; when Bloomberg began compiling CEO-confidence data in 2002, it showed a boost of 280 basis points for George W. Bush during his first 24 months in the White House.

Trump's tax cuts barely made a difference encouraging American companies to invest in themselves. While capital expenditures rose 9% in 2018 from the five-year average to $1 trillion for companies in the Russell 3000 Index, the money deployed for share buybacks and cash dividends increased 24% from the five-year average to $1.5 trillion, according to data compiled by Bloomberg.

Unlike Buffett's bullish-on-America railroad acquisition in 2009, Honeywell International Inc., the Charlotte, North Carolina-based multinational with sales in more than 30 countries, last year spent $4 billion buying back its shares, or 38% more than in 2017, according to data compiled by Bloomberg. At the same time, the diversified technology and manufacturing company spent $828 million on capital expenditures in 2018, or 20% less than it did in 2017.

Microsoft, the world's largest company with a market capitalization of more than $1 trillion, put $14 billion into capital expenditures last year, an increase of 20% over 2017. But it also spent almost $20 billion buying back its shares, or 82% more than it did a year earlier, according to data compiled by Bloomberg.

CEOs tend to blame uncertainty for their hesitation. Trump's tax cuts, trade wars and criticism of the Federal Reserve ushered in a period of market volatility that hasn't been experienced since he ran for president in 2016 and, before that, since the climax of the financial crisis and its aftermath between 2008 and 2012. The standard measure of investor anxiety, which is the average implied volatility of the S&P 500, increased three percentage points during Trump's first two years in office, according to data compiled by Bloomberg.

Under Obama during the similar period, the same VIX Index fell 10 percentage points. The last time the VIX surged for two years into a new presidency was at the beginning of the new century when Bush's tax cuts brought the U.S. budget back to deficits after several years in balance.

--With assistance from Shin Pei and Tom Lagerman.

To contact the editor responsible for this story: Jonathan Landman at jlandman4@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Matthew A. Winkler is a Bloomberg Opinion columnist. He is the editor-in-chief emeritus of Bloomberg News.

©2019 Bloomberg L.P.