(Bloomberg Opinion) -- You think you know what a green bond is? The boundaries are starting to fall away and the definitions are changing. It's a blurry line between greenwashing and an instrument that might actually do some good. But the momentum is towards more the merrier. So everything is greener nowadays. Even the riskiest of bonds, designed solely to prop up capital in banks and insurers, are fashionably charteuse.

At first glance, it does look surprising that the coveted “sustainable” label applies to the 300 million pound ($415 million) perpetual restricted tier 1 bond sold last week by Just Group PLC, a U.K. financial services group that specializes in retirement products. It’s the first of its kind for any insurer in Europe, which is now obsessed with environmental, social and governance issues.

This type of contingent convertible capital debt, known as CoCos, is designed specifically to be bailed-in or clawed back by the regulator in the event of failure — or if it falls below solvency capital requirements — and is comparable to additional tier 1 debt widely issued by banks. That means it is equity-like capital that supports the entire balance sheet of a company or enterprise in the event of some financial catastrophe. It is not just ring-fenced to fund ESG-related assets.

Any security that gets to be ESG-labelled ought to win that designation for two things: what the issuer is currently doing and what it will be doing. That is, it must have serious ambitions to move its balance sheet in an environmentally responsible direction. Just Group looks to be at least aspiring to those heights, and has a decent track record of doing so. Which is nice. Or to quote Oscar Wilde, “We are all in the gutter, but some of us are at looking at the stars.”

Just Group’s CoCo qualifies as a sustainable bond which has a wider perimeter than a green security, which is limited to clean transportation, green building and renewable energy. It has a wider perimeter: In addition to the green trio, it can also invest in social housing and local authority debt. These ESG labels may essentially be marketing — and not legally enforceable — but at least Just Group is putting its reputation at stake and blazing a trail.

Investors certainly seem comfortable: The coupon on offer was reduced from initial pricing talk of 5.625% to 5%, and demand was 10 times the bonds available. But then with yields generally so low across the investment grade sphere (this bond just sneaks in at BBB-) there is always a feeding frenzy for any form of return — and 5% is rare. So you can argue whether the sustainable factor conferred a “greenium” on the offer.

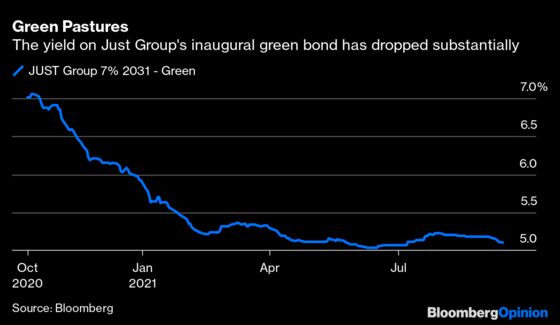

Just Group is probably happy to widen their investor base. It certainly has seen broader interest from funds in ESG-related deals. And the CoCo continues to herald the ESG-ing of its business model, following on the successful launch of its first green bond last October, a subordinated 10-year tier 2 (also bail-in eligible capital).

The greenery isn’t very permanent with other issuers. Take the inaugural “green” bank AT1 from Banco Bilbao Vizcaya Argentaria SA from July last year. That 6% bond will likely be called at the first opportunity in January 2026 and refinanced before BBVA’s balance sheet can get anywhere near being meaningfully green. That’s just green tourism, or maybe a drive-by.

It would be far more meaningful if such bonds had proper green strings attached. However, if the big sovereign and supranational issuers aren’t setting the example then it is hard to expect companies to do so, though some have taken it upon themselves. Global regulators should lay out clear criteria rather than letting it all evolve piecemeal. Perhaps progress might come from the task force on climate-related financial disclosures around the United Nations November COP26 summit. We live in hope for regulatory clarity.

In Just Group’s case, its regulator, the U.K. Prudential Regulation Authority, doesn’t even consider the sustainable label legally binding. In the PRA view, it is always good if an institution under its watch can minimize refinancing risks. If it does so by issuing green-tinged bonds that attract a wider audience, that’s great.

Just Group was put under serious stress in July 2018. Regulatory changes required that it put up significantly more capital against its main business. That forced it to boost its capital base by issuing a very expensive 9.375% callable perpetual RT1 in March 2019, which it has now tendered to buyback. The yield was below 3% at tender illustrating how significantly its financial situation has improved. It has also sold a 500 million pound portfolio of these niche mortgage products, steadily working to reduce its exposure.

It was logical of the insurer to cut the most expensive borrowings. It helps set a marker for lowering costs for Just Group’s 405 million pounds of senior debt that comes due by 2026. But Just Group is making itself increasingly the right color by getting close to the three-year objectives of the Tier 2 green bond issued last year — that is, by buying green assets.

Other issuers following in its footsteps may not be as virtuous. It would be a more perfect world if all this wasn’t all based on trust. Some entities will inevitably fall short of their promises. It ought to be a bit simpler to monitor what's bright green and not sludge. The dam has now been broken on allowing all debt along the capital structure to be tinted. Surely it deserves color-correction for the planet’s sake.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2021 Bloomberg L.P.