Is This Private Equity's Perfect Boris-Trump Play?

(Bloomberg Opinion) -- U.K. investors are down on the country’s defense sector, but the U.S. buyout industry takes a very different view. Thursday brought a 4 billion-pound ($5 billion) offer for British aerospace group Cobham Plc.

The bid from Advent International exploits both the weakness of the pound and a willingness among shareholders in downtrodden London-listed companies to take cash from private equity rather than hang on for a recovery – yet again.

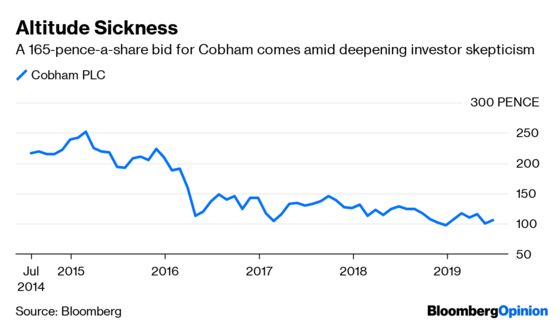

Cobham, whose technology is used in mid-air refueling and battlefield communication, has been hobbled by the debt it took on to fund some ill-judged acquisitions. Before today’s news, the shares had fallen more than 50% since the middle of 2015. CEO David Lockwood joined from Laird Plc just over two years ago. His predecessors had tried to repair the balance sheet with a stock offering. But Lockwood launched another, cut net debt to zero, and embarked on a turnaround. For all his efforts, the shares have languished.

The weakness of sterling – thanks to Brexit – has helped to make Cobham a much more affordable target. A little more than four years ago, its enterprise value was as much as $9 billion.

The 165 pence-a-share offer is 34% more the stock’s closing price on Wednesday and 50% above the three-month average. It values the group at 13 times expected Ebitda, a valuation not touched since 2017.

Rejecting a bid at this level would require the company to produce a standalone strategy with a reasonable chance of returning the stock to the same price that Advent is offering. In this industry, that would be tricky: It would rely on predicting armed conflict and U.S. defense spending.

What, though, could Advent do differently? Even if it took leverage back to its past highs, debt would still constitute less than half the purchase price. The firm will need to rely on more than financial engineering to make a return.

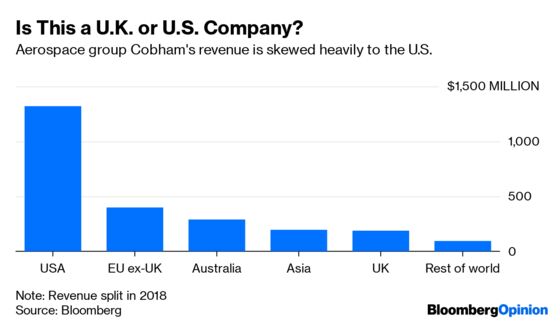

The obvious trick would be to turn Cobham into a U.S. company, allowing it to manage its operations there more closely and giving it some advantage in bidding for contracts in Washington. It would be difficult, though, to make this move as a public company: Many shareholders will be constrained by their mandates to own U.K. stocks. A takeover is a clean way of doing it while giving investors an immediate benefit.

The regulatory risks look manageable. The deal will require U.K. government approval. But it is likely that new Prime Minister Boris Johnson will want to show Britain is a market that is open to foreign investors. Hence Cobham shares are trading just above the offer price, a sign investors see a high chance of the deal succeeding.

It’s hard to see how Cobham’s board could have concluded that shareholders would be better off rejecting the bid. In Britain especially, private money is willing to pay higher prices than public market investors are willing to pay. The trend has further to run. For this buyer, though, it looks like a neat way to play both Boris Johnson and Donald Trump.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2019 Bloomberg L.P.