(Bloomberg Opinion) -- Billionaire Li Ka-shing built his fortune and legendary reputation by displaying an uncanny ability to time asset markets. Investors in Shanghai real estate need to ask whether his son has the same touch.

Victor Li’s CK Asset Holdings Ltd. is considering selling its 60% stake in a commercial building that’s valued at almost $3 billion, Bloomberg News reported this week, citing people familiar with the matter. The 54-year-old elder son of Hong Kong’s richest man took over as chairman of CK Asset and group flagship CK Hutchison Holdings Ltd. upon his father’s retirement last year.

The mixed-use development is CK’s single-biggest Shanghai project, so a decision to sell could be seen as a significant call on the city’s office market. It arrives as overseas investors such as Blackstone Group LP and Brookfield Asset Management Inc. have been piling into Shanghai. Foreigners accounted for about half the 53 billion yuan ($7.8 billion) in commercial property deals in the first quarter, a more than fourfold jump from what they spent a year earlier, according to figures from real estate broker CBRE Group Inc.

To get an idea of the CK group’s market-timing prowess, consider The Center. CK Asset sold the Hong Kong skyscraper for HK$40.2 billion ($5.2 billion) in November 2017, when the elder Li was still at the helm. The price was a global record for an office building, according to a Dealogic analysis cited in the Financial Times.

A year and a half later, it looks like CK may have picked the top of the market. Hong Kong’s office capital values fell 0.3% in the six months through March, according to Denis Ma, head of research at Jones Lang LaSalle Inc. Ma estimates they could drop between 5% and 10% this year as Hong Kong borrowing costs rise and economic headwinds build. Grade A rental yields are 2.7%, versus around 4% in 2010, according to JLL.

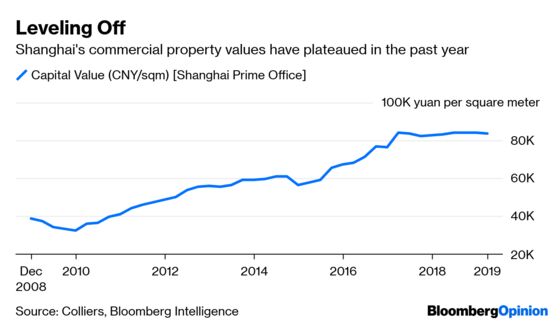

Shanghai office values have a similarly toppy look, having plateaued since the first quarter of 2017. China’s economic growth has slowed and a trade war with the U.S. is picking up steam, both factors that are likely to damp demand from companies to lease space in the city’s office buildings.

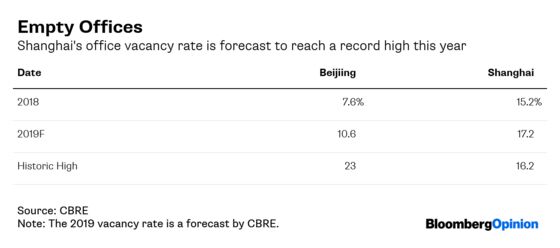

Added to this, domestic real estate investors have been struggling to get access to funding while there’s already evidence of serious oversupply in the commercial market. Shanghai’s office vacancy rate will climb to a record 17.2 percent this year, from 15.2 percent in 2018, CBRE forecasts.

Granted, CK’s development may not be a bellwether for Shanghai in the same way that The Center was for Hong Kong. The project, Upper West Shanghai, is outside the city’s downtown area in the northwestern district of Putuo. Moreover, a sale – should one happen – may not signify any view on the market. The Li family has been reducing its exposure to China for years.

At the same time, it would be rash to dismiss the signal that such an exit would send. Investors have been waiting for clues that Victor Li has inherited the investing savvy of his 90-year-old father, whose well-timed bets and $30 billion fortune have earned him the nickname Superman in local media.

A near-term dip in Shanghai property prices might suggest some of the master’s flair has rubbed off on his scion.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2019 Bloomberg L.P.