Citigroup’s Equities Blowout Signals Stress for European Peers

(Bloomberg Opinion) -- Wall Street is on fire.

While ordinary people and other businesses might be worrying about inflation or jobs or snarled-up supply chains ruining the holiday season, traders and dealmakers are still on a roll.

Citigroup Inc. delivered the biggest surprise of all the big U.S. investment banks that have reported third-quarter earnings this week. All the banks mostly beat analyst forecasts for advisory fees and revenue from trading, but Citigroup’s equities trading was on another level.

All this success might be getting too much for some. After Morgan Stanley also reported earnings Thursday, Chief Executive Officer James Gorman sounded almost complacent on Bloomberg TV when he said the Federal Reserve ought to “prick this bubble.”

But mainly the numbers from U.S. banks seem like a bad sign for the market shares of their European rivals, which report later this month.

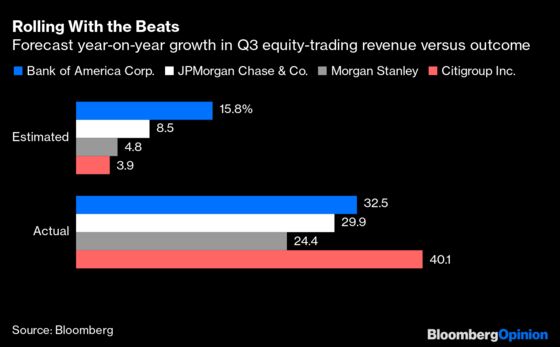

Citi is known much more for trading fixed income, currencies and commodities than equities. Analysts expected it to take advantage of busy stock markets this quarter, but less so than rivals. The consensus forecast was for Citi equities trading revenue of $909 million, up 4% compared with results in the period a year earlier.

In fact, it generated $1.23 billion of revenue, which was up 40% from last year and 35% ahead of the forecast. Its peers also beat their own more generous forecasts in equities: Morgan Stanley was 19% ahead, Bank of America Corp. 14.5%, and on Wednesday JPMorgan Chase & Co. was 20% ahead of estimates. Goldman Sachs reports on Friday; if it doesn’t beat its predicted revenue growth of almost 7.5% for equities that might end up being the biggest shock of the week.

But this string of expectation-busting results already suggests the U.S. banks are eating someone else’s lunch. Equities trading is forecast to fall in dollar terms for Credit Suisse and UBS already, while Barclays is expected to tread water. Their investors are probably looking on nervously. Stock prices for all three dipped on Thursday after the U.S. banks started reporting.

There’s no doubt that Credit Suisse is likely to have lost more ground. The Swiss bank took a $5.5 billion hit this year on loans to Archegos Capital Management, the hedge-fund-like family office of Bill Hwang. It has since cut back on the risks it takes in many areas and severely curtailed its prime brokerage unit, the business that deals with hedge funds.

Nomura, the Japanese bank that was also a big loser on the collapse of Archegos, has likely given up market share in this area as well.

The shock waves this episode sent through markets will have affected both sides: Hedge funds might prefer to take more of their business to the bigger players that are less likely to get nervous and withdraw support when markets get bumpy.

JPMorgan and Citi both highlighted their prime-brokerage operations as growth areas, meaning they hold more assets on behalf of hedge funds and lend more to them.

Another area of strength for Citi was traditional share trading (or cash equities as banks call it), especially in Asia. The region experienced the best growth globally in the third quarter compared with results in the period a year earlier. Bloomberg data show average daily trading values up 30% for Asia Pacific, much better than the 11% across U.S. exchanges or the weak-looking 2% growth in Europe.

That might help UBS more than other European banks because it has a bigger business there, especially among wealthy clients.

The story of U.S. banks taking share from European rivals is well known: The huge revenue American banks get from dominating their home market makes it easier to absorb the high regulatory costs of doing business everywhere else, too. But there are signs the process might be accelerating this year.

The best hope for European rivals is that their American competitors become too complacent. In spite of calls to prick bubbles, that feels like a pretty farfetched wish.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Paul J. Davies is a Bloomberg Opinion columnist covering banking and finance. He previously worked for the Wall Street Journal and the Financial Times.

©2021 Bloomberg L.P.