When Will China Blink and Stop the Evergrande Meltdown?

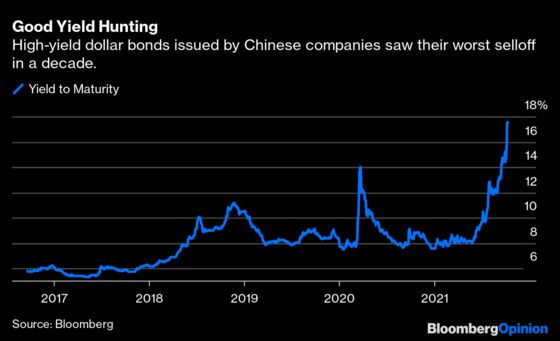

(Bloomberg Opinion) -- Beijing has been sitting firmly on the sidelines as real estate developers falter on their debt repayments, tumbling like dominoes. The central government is reluctant to bail out the likes of China Evergrande Group, asking local officials to brace for their demise instead. But corporate bond traders are unleashing the worst sell-off in a decade. At what point will China blink? Or won’t it?

Don’t fret. China’s debt is at 224% of gross domestic product, one of the highest percentages in the world. If it is at all serious about cutting that down, it will have to relent and do something dramatic. Maybe even bail out Evergrande.

But no country can deleverage in a deflationary environment. That’s Fixed Income 101. In the case of developers, their ability to service debt naturally improves if they can charge higher prices. That means home prices must rise over time. But this year, various levels of the government actually rolled out as many as 400 measures to cool prices in the red-hot housing market.

In the first-half of 2021, the more than 50 publicly-listed companies in the sector had $2.5 trillion in liabilities, almost doubling that of 2017. That’s about 17% of China’s GDP, data compiled by Bloomberg Opinion shows.

Even without the government’s intervention, developers were struggling with poor profitability. Modern Land China Co., which asked for a three-month extension for a $250 million note due Oct. 25, was generating negative operating cash flow in three of the last four years. So was Guangzhou R&F Properties Co, whose co-founders recently scrambled to shore up the company’s balance sheet, and our good old Evergrande. By some macro measures, the broader industry has accrued $5 trillion debt. Sometimes, you have to wonder why they are in business at all.

The cooling measures, ranging from rationing to price control, make the picture even uglier. During October’s Golden Week holiday, residential home sales slumped year-on-year in the country’s medium-sized cities — those in tier 2 like Wuhan (-55%) and Suzhou (-45%) — and smaller ones — in tier-3 like the Guangdong province manufacturing hub of Dongguan (-53%).

Deflation can be stubborn. Once Chinese households expect a broad-based slowdown, they won’t head into the market to buy property. They will wait instead. That, in turn, forces developers to cut prices — and the entire market spirals down. How then can Beijing expect its indebted developers to deleverage at all?

In recent weeks, the market was anxious about the prevention of a banking crisis. To that end, Beijing was seen doing a good job ring fencing developers from their lenders. With a Lehman moment fading, bond holders were afraid they’d be be left to wither.

But systemic risk is only one reason for a bailout. China also cares about its eventual goal: corporate deleveraging. A real estate bear market will make paying down debt that much harder. You can expect Beijing to step back from harsh tightening measures when an ugly set of home prices shows up in public. Or if Evergande starts a deflationary fire sale of its projects in some of China’s medium and small cities.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2021 Bloomberg L.P.