Google 'Minsky Moment' Before Buying These Bonds

Ever more obscure Chinese cities are selling debt as investors clamor for their generous yields. Tread carefully.

(Bloomberg Opinion) -- In just a few months, a shunned corner of China’s $13 trillion bond market has become an investor favorite. Thank the trade war.

Local government financing vehicles have long been seen as the potential trigger for a Minsky moment, a sudden crisis that follows a buildup of debt. As recently as October, there was little appetite for their bonds in the offshore dollar market. These days, millions are being raised by first-time issuers from cities so obscure that most people would need Google to find out where they are.

This remarkable turnaround in sentiment reflects investor bets that Beijing won’t let LGFVs default, at least for a while. As trade tensions with the U.S. intensify, China can’t afford to alienate the bond market. With the government back in stimulus mode, it needs such sales to finance infrastructure projects that will help to keep the economy growing.

China is notorious for pushing the dirty work of stimulus on to local governments that lack sufficient sources of income. They use debt to plug the gap. A spending spree in 2012 resulted in almost 30 trillion yuan ($4.3 trillion) of LGFV obligations. In the past three years, China amassed another 8.1 trillion yuan of special-purpose municipal bonds, Beijing’s new favorite tool for project financing.

Despite a spate of default scares involving state-owned enterprises and investment conglomerates, no municipality or LGFV has reneged on its bond obligations. Yields are also alluring: Provincial LGFV debt can pay 5% or more.

In their enthusiasm, investors haven’t necessarily lost the ability to discriminate. Provinces with high ratios of LGFV bonds to GDP are paying more to borrow, a Bloomberg News analysis showed Tuesday.

This makes sense, as far as it goes. What’s missing, however, is how much we know about these structurally opaque vehicles, which are essentially shell companies set up by municipalities to finance off-budget projects, and how much corporate-governance risk they entail.

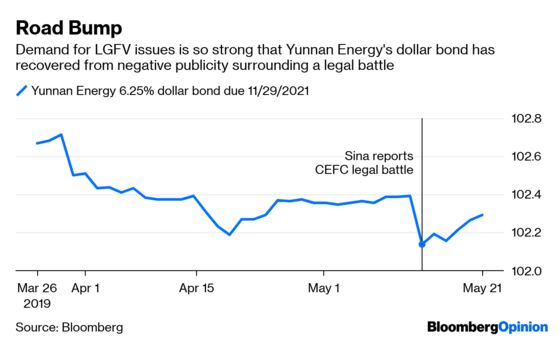

Earlier this month, bonds of Yunnan Energy Investment Overseas Finance Co. fell after Sina.com reported that the company was embroiled in a legal battle with CEFC China Energy Co., an energy trader that defaulted on a series of bond payments last year. The dispute centers on financing of a venture between the two companies, according to the Chinese media outlet.

Nasty discoveries can be made when things go sour with government-linked entities. Qinghai Provincial Investment Group Co. was long considered an LGFV by bond investors. When the aluminum maker missed a coupon payment in February, doubt surfaced as to its exact nature.

The company was 69%-owned by the Qinghai State-owned Assets Supervision & Administration Commission, the government body that supervises state-owned enterprises, according to HSBC Holdings Plc. As a result, “we consider the group a local SOE,” the bank wrote in a report.

That changed the calculation entirely: China allowed SOEs to go bust as early as 2015. This saga, at least, had a happy ending: Qinghai Provincial paid its dollar bond coupon by the end of February and its bonds recovered from their plunge.

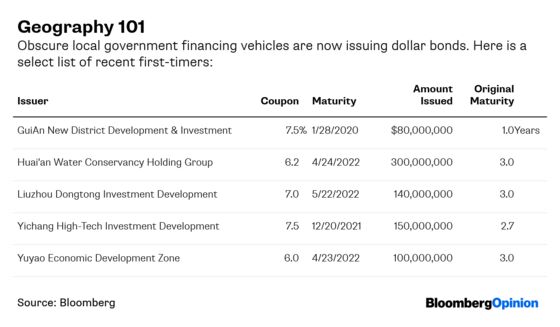

Investors have long looked at provincial governments’ finances, but a stream of new issuers will soon force them to investigate at a more granular level. Do you know where Huzhou, Yichang, Yangzhou or Zhuzhou are, or what their governments’ books look like? Yichang Gaoxin Investment Development Co., from the second-largest city in central Hubei province, issued a $150 million dollar bond in April, as yield-thirsty foreigners clamored for its 7.5% coupon. Some, such as BlackRock Inc., settled for 4.5%.

To beat benchmarks, bond-fund managers may have no choice but to buy high-yielding Chinese local government debt. They need to recognize they’re in uncharted waters, though. A good geography lesson is in order.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.