(Bloomberg Opinion) -- You’d expect the world’s second-largest economy to have a bigger presence on the world stage. But in mergers and acquisitions, China’s presence has been shrinking for years, and 2020 is unlikely to be any better.

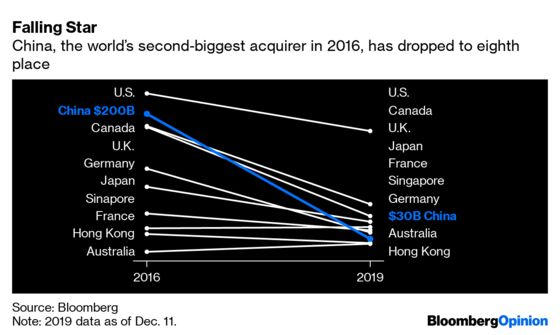

In 2016, the country was the world’s largest acquirer of overseas assets after the U.S. It tumbled to eighth place this year, trailing Japan and even Singapore, according to data compiled by Bloomberg. While the phase-one trade deal between Washington and Beijing may ease some tensions, frosty relations between China and many developed countries appear set to persist. Add tightened credit to this protectionist mix, and China’s acquisitions have little chance of regaining the heights of 2016, when state-owned China National Chemical Corp. agreed to pay a record $43 billion to buy Swiss agrochemical maker Syngenta AG.

Such actions have been seen as a clear shot at the Made in China 2025 plan, which set targets for the country to become a leader in critical technologies. Chinese venture capital investment in the U.S. fell 27% to $1.1 billion in the first half of 2019, from $1.5 billion in the July-December period last year, according to Rhodium Group LLC, an independent research firm.

Europe, previously more receptive to Chinese investment, has turned a lot less welcoming on the sale of technology and infrastructure. Regulators took their time approving what could have been China’s largest overseas deal of 2019 — the 9.1 billion euro ($10.2 billion) takeover of Portuguese utility EDP-Energias de Portugal SA, prompting state-owned buyer China Three Gorges Corp. to pull out in April. Germany, meanwhile, is looking at putting tighter restrictions on Chinese buying following high-profile investments in companies such as Deutsche Bank AG and industrial robot maker Kuka AG in recent years. A push by lawmakers to ban Huawei from its 5G network threatens to further chill relations.

Even President Xi Jinping’s signature Belt and Road Initiative, which prompted a wave of Chinese acquisitions in countries that have signed on to the trade-infrastructure campaign, has faced a backlash.

Beijing’s drive to control debt has played a part in tamping down deals. After the ill-fated spending sprees of conglomerates such as HNA Group Co. and Anbang Insurance Group Co., now being unwound, companies have become more cautious. Chinese banks are less aggressive when it comes to lending for overseas purchases, according to Bee Chun Boo, M&A partner at Baker McKenzie’s Beijing office.

The average size of China’s foreign acquisitions has shrunk by two-thirds since 2016 to $74 million, from $230 million (a figure that already strips out the Syngenta deal). Chinese buyers have stopped seeking controlling stakes to avoid raising protectionist hackles, and are searching out non-Chinese buying partners.

Anta Sports Products Ltd.’s $5.2 billion purchase of Finland’s Amer Sports Oyj is an example of what the typical Chinese acquisition may look like in coming years. Anta led an investor group that included Lululemon Athletica Inc. founder Chip Wilson, and the target — a tennis racket maker — was in a non-sensitive sector.

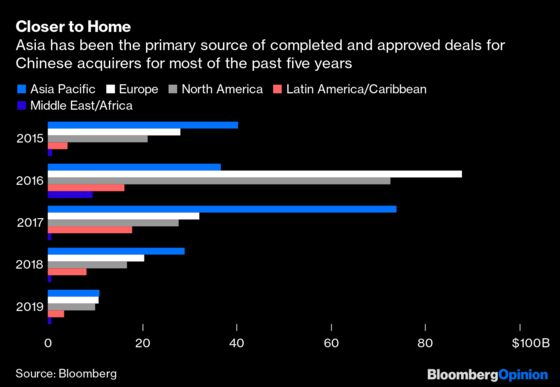

With the environment souring in the U.S. and Europe, Chinese acquirers will look more within Asia. In September, China Telecommunications Corp.’s entered a $5.4 billion agreement to set up a third major Philippine telecom operator with two local partners.

The home market may provide more promising action for China-focused bankers in the year ahead. Beijing is opening its financial sector, inviting more foreign banks, insurance providers and other companies to set up shop. In November, Chubb Ltd. paid $1.5 billion to boost its stake in Huatai Insurance Group, and Allianz SE forked out about $1 billion for part of Goldman Sachs Group Inc.’s stake in Taikang Life Insurance Co. Deal activity may accelerate in 2020, when foreign securities firms, futures businesses and life insurance companies will be allowed to fully own their Chinese units.

As financial companies enter, others are leaving. Chinese buyers are picking up the pieces as Carrefour SA and Metro AG sell the bulk of their local operations, joining Tesco Plc and Distribuidora Internacional de Alimentacion SA in giving up on a tough retail market. Nestle SA is another international company considering options for its Chinese units.

Advising on exits is a shrinking business by nature, though, and unlikely to compensate for the fall-off in China’s outbound deals. No China M&A banker is going to be partying like it’s 2016.

--With assistance from Yuan Liu and Elaine He.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2019 Bloomberg L.P.