How the End of Growth Could Save China Internet Stocks

(Bloomberg Opinion) -- It’s time for Chinese internet executives to embrace the slowdown.

Heady days of 50% sales growth are over, which means they needn’t keep burning marketing money to chase revenue that isn’t there. Part of this slowdown is due to both Chinese and global economic weakness, yet much of it was the inevitable conclusion to a long and lucrative boom in the world’s hottest industry. The sooner management accepts this new reality, the sooner they can start delivering stable earnings growth.

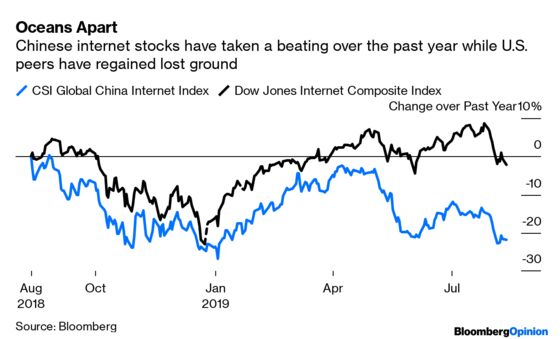

Investors have already shown impatience. The CSI Global China Internet index – a collection of 30 companies that includes Alibaba Group Holding Ltd. and Tencent Holdings Ltd. as well as lesser-known Mango Excellent Media Co. – has dropped 22% over the past year. By contrast, the Dow Jones Internet Composite Index, which tracks the likes of Amazon.com Inc. and Snap Inc., is off just 2%.

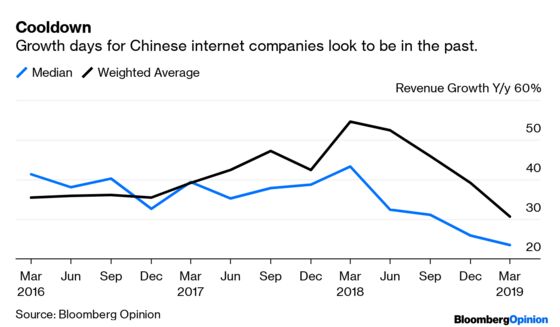

A quick look at revenue for these Chinese companies tells the tale. As recently as a year ago, top-line growth surpassed 50% across the industry, spurred by massive rises at Alibaba and Xiaomi Corp. On a more balanced basis, the median growth rate was 10 to 15 basis points slower, which is still significant.

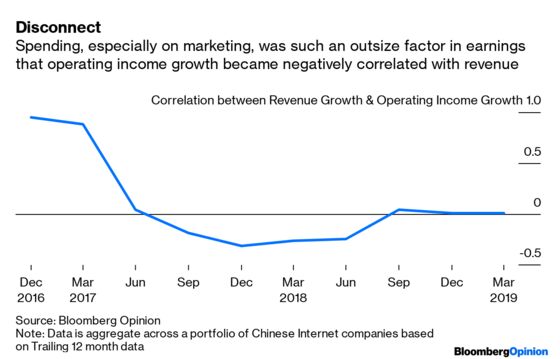

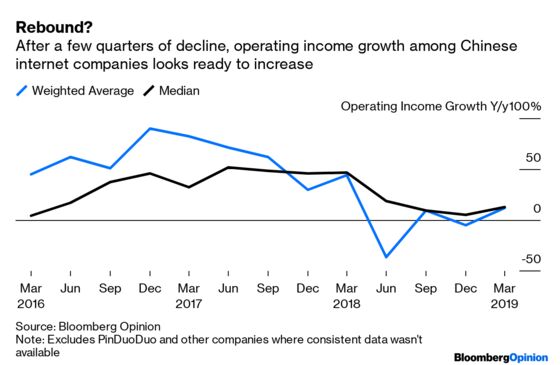

And yet operating income fell far behind, dropping into a decline on a weighted basis with median growth rates in the single digits. I’ve warned about this disconnect between revenue growth and profits. The problem has been that management, and investors, became so obsessed with the top line that they lost sight of the bottom. Which is why companies spent big on marketing to ensure revenue numbers kept hitting those heady heights.

The result was a negative correlation between revenue growth and operating income expansion. That’s not the way it should be. Companies should reap the rewards for selling more of their wares, not suffer for it.

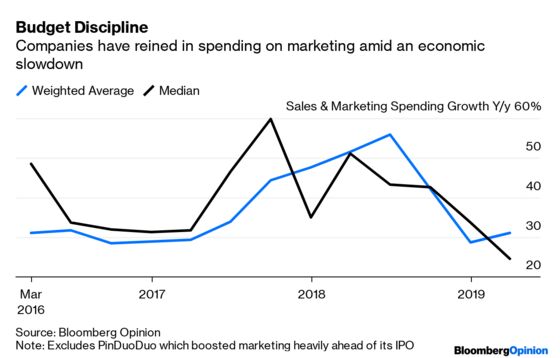

Now there are signs that this obsession with growth may be coming to an end. After more than a year of using marketing dollars to juice revenue, some of the more savvy management teams have reined in spending. They’re pragmatic enough to recognize that in this new, more sedate era there’s a limit to how much they can gain from chasing users.

We’re in the early phases of the June-quarter earnings season, but there are already encouraging signs. NetEase Inc., the online games and content company, cut its sales and marketing budget by 22% after reducing it by 32% the prior quarter. The result is that while revenue climbed only 15%, operating profit expanded 49%. The stock was rewarded with a 13% rise over the following two days.

China Literature Ltd., a provider of e-books and online publishing, by contrast reaped little reward from an 85% increase in marketing expenses for the first half, posting revenue growth of just 30% and a 15% drop in operating income. The company showed weakness in its paid-reading business while its free model has yet to be fully monetized, analyst Wei Ming of China International Capital Corp. wrote Tuesday, noting that the company faces continuing regulatory headwinds. Investors saw the folly in spending big on marketing when there are limits to driving revenue, sending the stock down as much as 19% in Hong Kong.

Both Alibaba and Tencent will report earnings in coming days. Investors have come to understand that revenue growth isn’t what it used to be. If management embraces this new normal, then shares may enjoy the rewards of fiscal discipline.

To contact the editor responsible for this story: Patrick McDowell at pmcdowell10@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Culpan is a Bloomberg Opinion columnist covering technology. He previously covered technology for Bloomberg News.

©2019 Bloomberg L.P.