To Dispel the Property Crisis, China Has to Tame Two Types of Bad Borrowers

(Bloomberg Opinion) -- There are two types of scary borrowers in China. The first kind has good-looking assets but it isn’t quite clear how much debt they have hidden away. That’s at the heart of the China Evergrande Group crisis. The second has a lot of debt but no assets to shore up their ability to repay — but they have the political connections some hope will help bail out the first kind.

To avoid hurting the broader economy, China is considering easing rules to let its distressed real estate developers sell off assets to avoid defaults. The so-called “three red lines” on leverage ratios — formulated in August 2020 — were so tight that there were no buyers for developers’ property holdings even if the likes of Evergrande were willing to offload projects at fire sale prices.

Going forward, as the Wall Street Journal reported, regulators might allow white knight developers to take over assets without having the projects’ associated debt affect their own leverage ratios and risk crossing the three red lines.

That would be a relief. But will anyone take the bait? Even the richest real estate magnates might have second thoughts because of the many hazards beneath the surface.

In the fast-churn, high-leverage world of Chinese builders, every step is an opportunity to squeeze in hidden debt. To buy land, developers often borrow from trust companies. To secure the deals, the real estate firms ask their own senior management and employees to buy into these trust products.

Even after purchasing the land, developers are unlikely to get enough bank loans to cover construction costs. That’s because large commercial banks are already dangerously exposed to the regulatory cap of 40%. As a result, developers start to owe money to their suppliers, often in the form of commercial paper. They also do pre-sales, which require consumers to pay the full price of a home upfront, long before the property has been completed. In short, developers end up borrowing from everyone.

So, when a new corporate buyer goes shopping for a development project, many creditors already have claim on the property. The project may even have been offered as collateral to wealth management products elsewhere. Sometimes, the financing is so complex even the seller does not know how much money it owes. Who wants to be mired in this web!

One solution has been for corporate rescuers to jointly develop projects with distressed developers who then have to absorb all liabilities. Once the partners finish the projects, they can sell all the apartments, and the troubled builder will have enough money to repay its debt, or so the thinking goes.

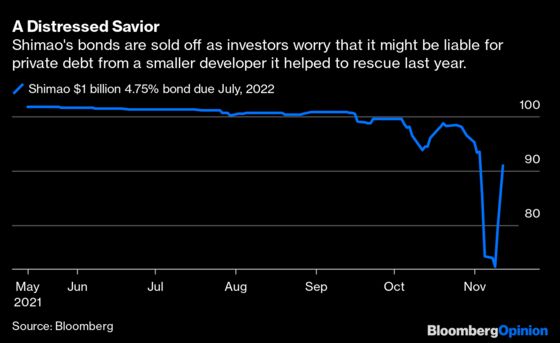

Unfortunately, this doesn’t work well in practice. When sellers fail, the white knights can’t quite disentangle themselves from extraneous effects. For instance, in January 2020, Shimao Group Holdings Ltd., the 10th largest builder by sales last year, came to the rescue of struggling Fujian Fusheng Group Co., promising a joint venture to develop Fusheng’s projects. That came at a steep cost. This month, as selloffs spread to the better-known names, traders dumped Shimao’s bonds, worrying that it’s on the hook for private debt issued by Fusheng. Last week, Shimao lost its investment-grade rating at S&P Global. In this environment, a white knight must be extra cautious. One bad move and the savior itself would need to be saved.

Traders love to dream about state-owned white knights riding in to the rescue. But are they really big enough to save their private peers? The top ten builders are, for the most part, private enterprises. And the government hasn’t exactly been willing to rescue its own firms. Beijing has let state-owned firms default as far back as 2015. Even state-owned enterprises must watch their wallets.

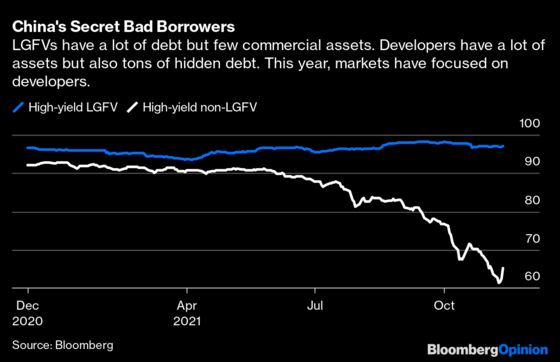

Financially and politically, there has been another option: bailouts from provinces and municipalities. These routinely set up shell companies to build roads and repurpose farmland to residential use to stimulate the local economy. They are the debtors of the second type. Few of these so-called local government financing vehicles are profitable or have assets that can make money, but investors don’t look at their cash flow. They focus instead on how much political support these vehicles can get to remain viable. So, unlike developers, LGFVs have no trouble tapping onto the onshore bond market. With 11 trillion yuan ($1.7 trillion) of bonds outstanding, they are the single largest group of debt issuers in China itself.

For example, the Guangzhou-based developer China Aoyuan Group Ltd. was offered 2 billion yuan in loans from a local LGFV: the collateral was the developer’s headquarters, guaranteed by the chairman, according to a report by Redd last week. In addition to owning toll rights of roads to nowhere, LGFVs can provide creditors empty apartment blocks, too. LGFVs are a crisis waiting to happen.

Desperate times demand desperate measures. Beijing has vowed not to bail out Evergrande, already the world’s most indebted developer. But market conditions have worsened since it made that promise in mid-October. Even investment-grade builders like Country Garden Holdings Co. have seen its bonds tumble, a sign that contagion risk is real. China has to find a workable solution to fix the developer debt crisis. Time is running out.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2021 Bloomberg L.P.