One Big Chinese Lesson for America’s Infrastructure Plan

(Bloomberg Opinion) -- If President Joe Biden is planning to transform America’s infrastructure with the $2.25 trillion plan unveiled last week, he could do worse than learn from China.

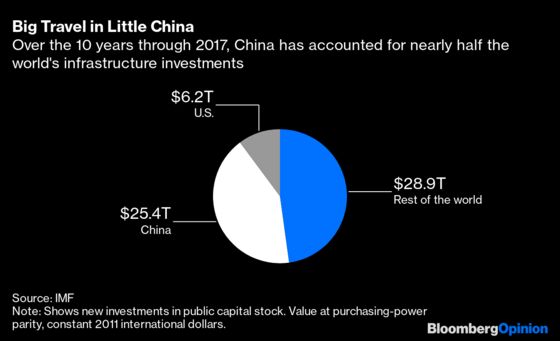

Its spending on roads, rails, bridges, metro systems and telecommunications and new cities since the 2008 financial crisis has transformed the country. A nation that opened its first true high-speed rail line between Beijing and Tianjin in 2008 now has more fast lines than the rest of the world put together. About 42 cents out of every dollar invested in public capital globally between 2008 and 2017 was spent in China.

There’s a vital lesson in the way China has managed to roll out so much investment in such a short time. Effective infrastructure depends not so much on top-down directives and funding, as on giving local governments and private businesses the right incentives to develop the facilities they need. In America, municipal and state governments still struggle to capture the economic benefits brought about by their infrastructure investments. It’s little wonder they’re not building enough.

Capturing the land value of improved infrastructure is fundamental to the modern Chinese economy. The model is brutally effective. First, governments secure land on the fringes of cities, where the property rights of individual landowners are often weak. Next, build the transport and communications needed to transform rural real estate into far more valuable development land. Finally, sell shovel-ready residential and commercial plots to real estate developers at vastly inflated mark-ups.

This system has been so effective over the past decade that about 29% of China’s consolidated government revenue in 2017 came from real estate sales, according to Caijing.

For obvious reasons, this model can’t be adapted wholesale to America. Without the dispossession of individual landowners and a troubling concentration of power in the hands of local officials, it wouldn’t work at all. At the same time, there’s a range of ways for the public sector to capture the increasing value of development land that go well beyond current practices in the U.S., while falling short of the plunder practiced by many Chinese municipalities.

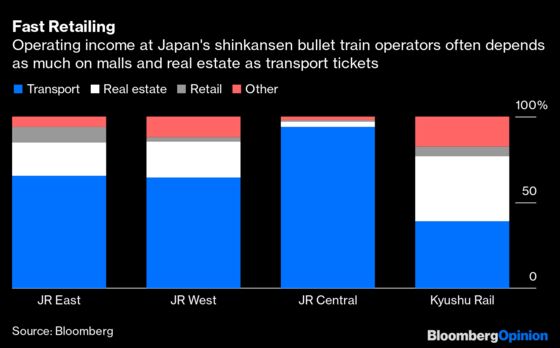

Take Japan’s privatized transport sector. Much of the industry, including some of the famed shinkansen bullet-train operators, are as much real estate developers as they are train companies. Kyushu Railway Co., which has the southern-most leg of the high-speed network, makes more money building and and running malls and other properties than it does from selling train tickets, as we’ve written. By investing in and developing land in the vicinity of their transport corridors, they’re able to cross-subsidize rail operations that run at cost or even at an outright economic loss, while still delivering benefits to the public.

New York’s Grand Central Station was built with a similar rationale, financed in part by the real estate developed on top of the covered rail yards that extend 16 city blocks north of the main concourse. London’s Crossrail project is earning 500 million pounds ($691.55 million) from similar developments, and Sydney’s new metro line has involved the demolition of multiple office towers to make way for new, more valuable high-rises in their place.

In all these cases, it’s attractive for the government to build infrastructure because it’s able to capture some of the increased land value that results. That’s rarely the case in the U.S.

Measures to levy fees on the local property owners, such as the special assessment zones used to finance projects like Seattle’s South Lake Union Streetcar, could in theory have a similar effect. The problem is that the unity of purpose needed to develop larger-scale infrastructure is lacking in the modern U.S., according to David Levinson, a professor of transport engineering at the University of Sydney and former transportation planner in Maryland.

“Transportation decisions are much more fractured” in the U.S., Levinson says. “Property taxes are a local government thing whereas transport infrastructure funding tends to be a state thing. Governments aren’t willing to upend the privileges of municipalities to get infrastructure built.”

That fragmentation also means that spending is too reactive — for instance, repeatedly widening roads to eliminate congestion rather than developing integrated visions for how cities as a whole could function better. “The traffic engineers have more power than the planners,” Levinson says, “and the decision makers drive a car, so they have the view from their windshield.”

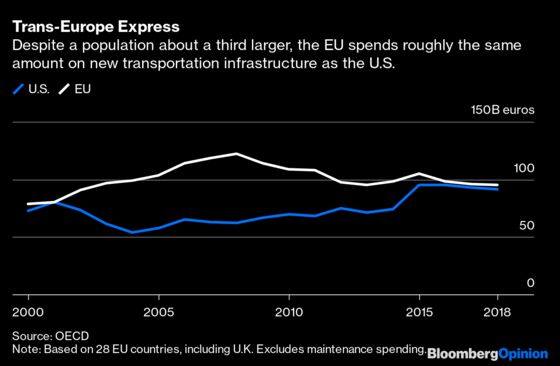

The risk of a major infrastructure program that doesn’t tackle some of these coordination problems is that the money will end up wasted, or just substituting for funds that states and municipalities should be spending anyway. The fundamental problem for infrastructure in the U.S. isn’t so much that it’s underfunded — transport spending is equivalent to that of the European Union, which has roughly a third more people — but that all that spending is failing to deliver the amenity that U.S. citizens deserve.

For all its governance failings, using public spending to improve people’s quality of life is one area where China has excelled over the past decade. An America that wants to repeat the trick shouldn’t be too proud to learn from that experience.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2021 Bloomberg L.P.