China’s Chemicals Mega-Merger May Have Come Too Late

(Bloomberg Opinion) -- Better late than never?

Three years of efforts to combine China’s giant state-owned chemicals companies Sinochem Group Co. and China National Chemical Corp., or ChemChina, may finally be paying off. A merger between the two unlisted companies is at last “in progress,” Frank Ning, the chairman of both companies, said last week.

Such a deal would create a behemoth with about 1.04 trillion yuan ($152.2 billion) of revenue. If it was ever listed, that might result in a market capitalization of 777 billion yuan on the 0.75 times price-sales multiple typical of large chemical businesses — roughly the size of BASF SE, Dow Inc., and Nutrien Ltd. put together.

Size isn’t everything, though, and any completed SinoChemChina deal is likely to look less like a triumph than a limp to the finish line.

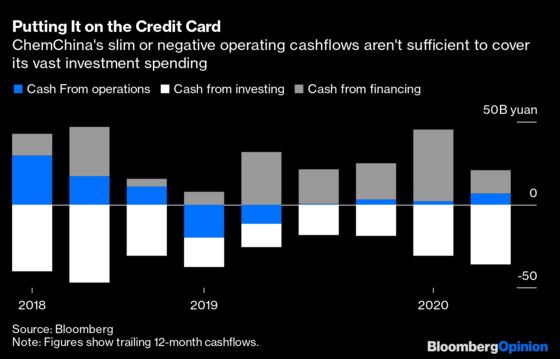

The reason is ChemChina’s vast and growing debt mountain. Since its $43 billion takeover of Swiss crop-science giant Syngenta AG at the height of China’s outbound acquisitions spree in 2017, the company’s borrowings have only grown, thanks to ongoing capital spending far in excess of operating cashflow. The $20 billion that funded the Syngenta deal looks modest next to net debt which stood at 434.23 billion yuan, or $63.6 billion, at the end of June.

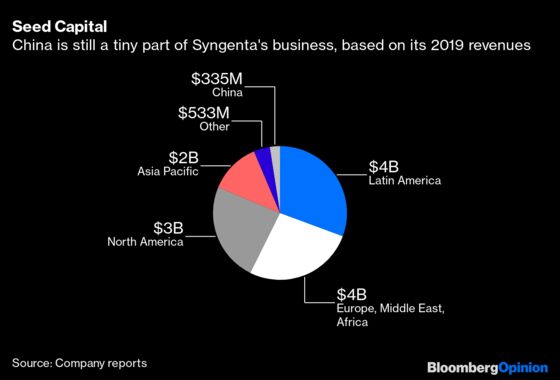

Operating income barely covers the interest bill and the company hasn’t made a profit since the takeover was completed. Despite hopes that owning one of the world’s crop giants would allow China to drastically increase the productivity of its domestic farming industry and food security, Syngenta’s mainland sales have barely risen, with the biggest jump in revenue coming from Latin America. No wonder’s China’s ambassador to Switzerland labeled the takeover a mistake.

A spinoff will go some way toward winding back the debt clock. Ning has already been working to combine ChemChina and Sinochem's agricultural assets into a vehicle that would be suitable for listing on mainland exchanges. Pre-IPO financing from state-backed investors could provide $10 billion in return for 20% to 30% of the company, Reuters reported last year citing people familiar with the situation. If a similar amount could be raised from smaller shareholders, SinoChemChina could end up with $20 billion while still holding onto a majority stake in its listed agritech business.

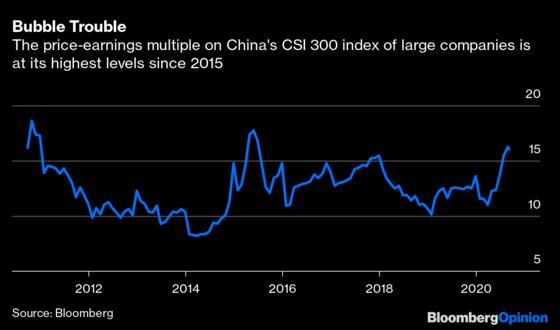

There’s no time like the present to get that long-awaited initial public offering done. China’s equity markets are in a frothy state these days, as my colleague Shuli Ren has described — perfect conditions for raising cheap money. The multiple on the CSI 300 index of large companies recently broke through 16 times for the first time since the 2015 market bubble.

There’s been another bit of news that may throw a wrench in the works, though. The U.S. Department of Defense last month added both Sinochem and ChemChina to its list of entities it considers “Communist Chinese military companies.” That gives the White House broad powers to impose crippling sanctions on any company doing business with them. Just consider the $1.19 billion fine the Trump administration levied on ZTE Corp. in 2017.

That's some risk factor to add to your IPO documents. On one hand, SinoChemChina’s bankers will have to hope that the febrile conditions in China’s equity markets hold out long enough for them to do the remaining work on the share sale. On the other, they’ll be looking nervously over their shoulders for signs of a late-night Trump tweet that could sink the whole show. More than 97% of Syngenta’s business is outside China. If sanctions were imposed, nothing less than full separation from SinoChemChina would be sufficient to preserve it from ruin.

Sanctions hold a sword of Damocles over what would remain of the business, too. The billions that ChemChina has been dedicating to capital investment is just a small part of the constellation of new chemical plants under construction in China in recent years, with vast complexes being planned or built by Hengli Petrochemical Co., Rongsheng Petro Chemical Co. and even BASF. Despite rapid increases in domestic demand, these plants need robust export markets to soak up their product — but that route would be closed off to SinoChemChina if Washington was to unleash its thunderbolt.

A better prospect would be to junk plans for a domestic IPO and sell Syngenta back to the market in its entirety, along with ChemChina’s 45% stake in tire maker Pirelli & C. SpA and Sinochem’s oil-trading unit. That would give up on SinoChemChina’s grand strategic ambitions, but would at least salvage the maximum amount of cash from the wreckage.

Ning, who earned his MBA at the University of Pittsburgh, could then turn his entrepreneurial skills to a task even more important than doing mega-deals: Getting China’s newborn chemicals giant to live within its means. Once upon a time, Sinochem itself was a candidate for a stock market listing. If it’s to get in the sort of shape necessary to attract investors, a thorough clear-out is in order.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2020 Bloomberg L.P.