CEOs Beware, Shareholders Want You to Go Green Fast

(Bloomberg Opinion) -- Most listed companies are duty bound to hold a general meeting for all shareholders at least once a year. They’re typically dull gatherings at which the annual report gets signed off and the board gets reinstated. In recent years, disputes about executive pay have triggered some fireworks. This year’s round of U.K. conferences could be spicier than usual, as asset managers press the companies they invest in to reveal more about the risks posed to their businesses by the climate crisis.

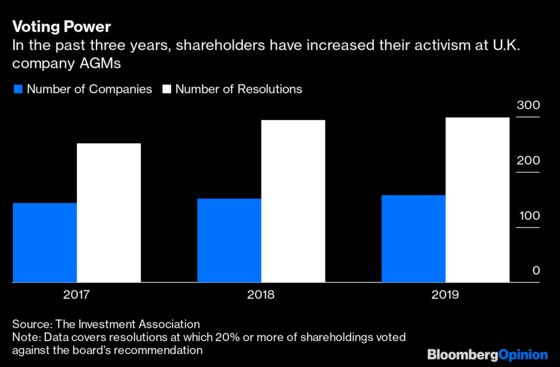

U.K. fund managers have been flexing their muscles more frequently in recent years. The Investment Association, which represents 250 U.K. asset managers overseeing 7.7 trillion pounds ($10 trillion), keeps a scorecard of how many company resolutions meet objections from at least 20% of shareholdings, or which the board withdraws before a vote, adding them to what it calls its public register.

In the three years it’s been compiling the data, the number of companies facing what’s deemed “significant shareholder dissent” has increased by almost 10%, while the number of individual resolutions facing opposition has grown by about 20%. Last year, about a quarter of the 620 or so companies on the FTSE All-Share index made it onto the Investment Association’s register.

Traditionally, the main battleground has been executive pay, with more than a third of last year’s list comprised of companies falling foul of investors on remuneration. But this year, the Investment Association will start pressing U.K. companies to align with the Task Force for Climate-Related Financial Disclosures, an initiative set up by the Financial Stability Board and chaired by Michael Bloomberg, the founder and majority owner of Bloomberg LP, the parent company of Bloomberg News.

The association is asking British companies to detail how they assess climate-related risks, what steps they’re taking to mitigate those impacts and what metrics they use to measure progress. Given that its members own about a third of the U.K. stock market, its views carry a lot of clout.

At least one major U.K. company already faces a hard-hitting resolution aimed at making it more green. Amundi SA, Europe’s biggest fund manager with more than 1.6 trillion euros, and Jupiter Fund Management Plc are among investors in Barclays Plc planning to back a resolution in May asking the U.K. bank to halt loans to energy companies that aren’t aligned with the Paris Agreement on climate goals. The move is being coordinated by the non-profit group ShareAction.

The increased focus on the desire for money to do well socially as well as financially is a global phenomenon. Earlier this week, three of the world’s biggest pension funds — California State Teachers’ Retirement System, Japan’s Government Pension Fund and the U.K.’s university steward USS Investment Management Ltd. — issued a joint statement applauding efforts to incorporate environmental, social and governance issues in portfolio construction. “Skeptics that continue to question the growing role of sustainability within the global investment community should realize that they are quickly becoming the minority,” the trio said.

Adding to the drumbeat, Norway’s sovereign wealth fund, the world’s biggest with about $1.1 trillion in assets, said earlier this week it wants the companies it invests in “to go from words to numbers in their sustainability reporting.” For companies it deems to be falling short, it will consider backing what it called “a well-founded shareholder proposal calling for reasonable disclosure.”

This shift in attitudes isn’t because investors have signed up to the Extinction Rebellion movement and started worshiping teen climate icon Greta Thunberg. It’s because the fund management community has come round to the view that what’s happening to the environment poses a clear and present danger to the long-term viability of many of the companies it invests in. It’s a capitalist response to a financial threat.

And voting on resolutions can make a difference. In September, non-profit group Majority Action published an examination of the U.S. voting records of 25 of the world’s biggest asset managers. The study said BlackRock Inc. and Vanguard Group Inc. voted against at least 16 climate-related resolutions that would have passed with their backing. Given BlackRock’s January statement that it plans to “place sustainability at the center of our investment approach,” the world’s biggest money manager is much more likely to support any similar proposals in the coming year.

It’s still early days in the drive to hold companies accountable for non-financial disclosures, so there are a couple of common, sensible threads to this newfound insistence on improving corporate reporting of business-related climate threats. For one thing, there’s a recognition that it will take time for company boards to gather and report the necessary data. The Investment Association says it won’t sanction companies that fail to heed its call to enunciate their climate exposures at this year’s AGMs, though it reserves the right to become more vocal in targeting laggards in the future. Norway’s wealth fund says it won’t support shareholder proposals that prescribe “detailed methods, unrealistic time frames or targets for implementation” of ESG reporting.

Getting climate-related resolutions on the agenda, and garnering the votes needed to implement them, are essential steps for investors to deliver on the challenge of safeguarding the capital entrusted to them by holding companies accountable for protecting the earth for future generations. Reporting standards will only improve with practice: It would be wrong to allow perfection to become the enemy of the good. One of the oft-repeated complaints fund managers make about assessing the environmental record of the companies they invest in is the lack of coherent data. The sooner companies make the effort to come up with quantifiable ESG targets and goals, the faster the system can be refined and recalibrated into a more useful and universal form.

To contact the editor responsible for this story: Melissa Pozsgay at mpozsgay@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2020 Bloomberg L.P.